Part of our General Ledger guide

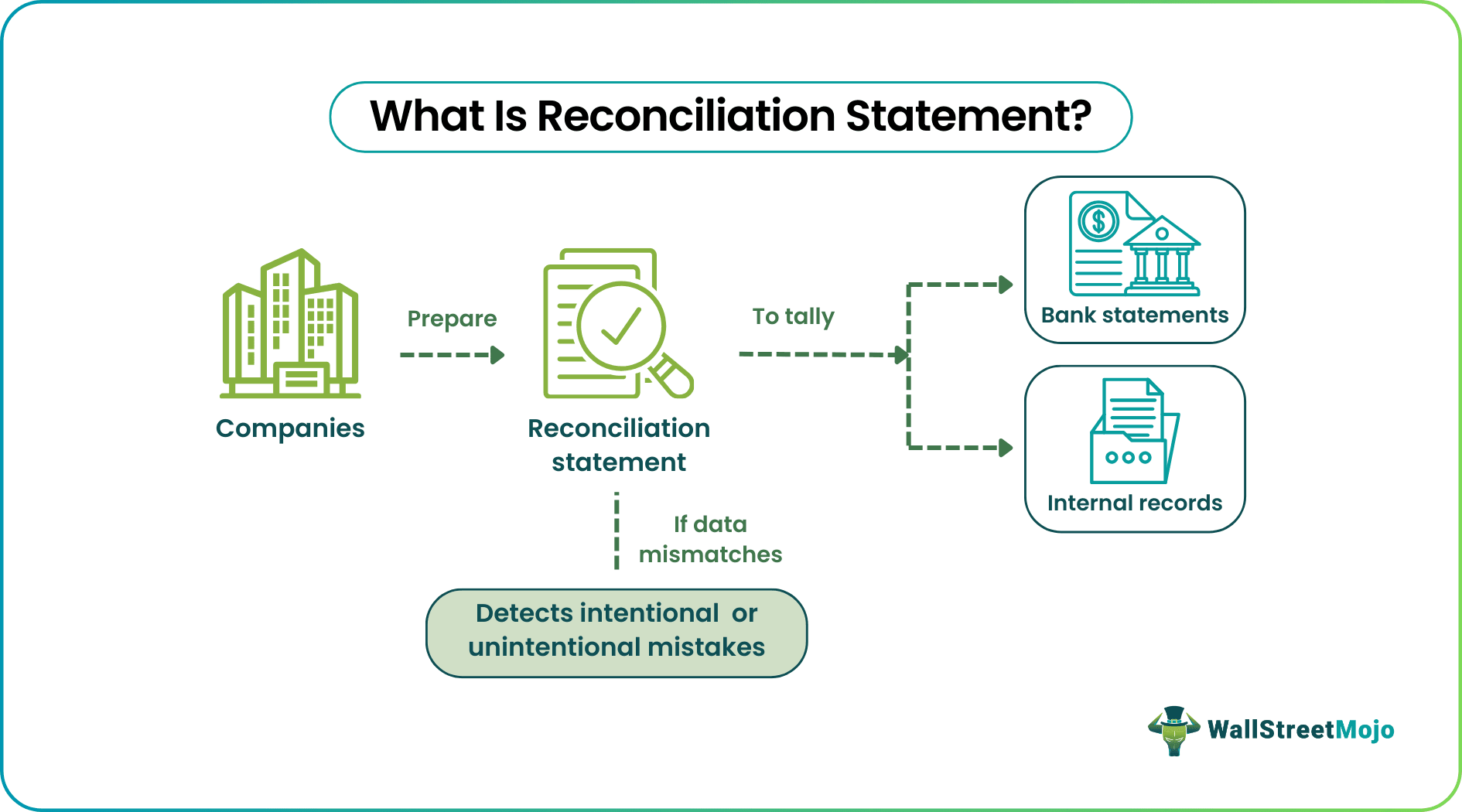

What Is Reconciliation Statement?

A reconciliation statement refers to the banking summary prepared by the banks to list down the bank’s account balances and compare the same with their internal records. The purpose behind preparing these statements is to detect the differences between the entries of the two statements and work on rectifying them.

Preparing reconciliation statements is a significant task for any company as it helps them manage the business finances well. When there is a discrepancy in the statements, they get to know where the issue lies and treat them accordingly, thereby helping them know their exact financial position.

Reconciliation Statement Explained

A reconciliation statement contains a list of differences between bank balance as per bank statement vis-à-vis books of accounts, debtor-creditor reconciliation, debt balance reconciliation, or any other reconciliation where there is a difference in the records of two separate legal entities. It aims to nullify the difference in the same or next accounting period to have parity in the books of accounts of both legal entities.

In the process of making this statement, a company starts with listing down its own internal records, which reflects its account balance. This account balance is the figure obtained when the company adds and deducts the amounts to and from its finances while reconciling items. This reconciliation of the company records is done in another additional column added, which is then available for further adjustments. These further adjustments are made when the data is compared with the account balances depicted in the bank statements.

The comparison between the two records maintained by two entities helps the company’s internal records to be checked against discrepancies, thereby letting accounts professionals work on rectifying them so that the statement reflects accurate data. While these discrepancies, in many cases, are caused due to human error or unintentional attempts, there are events where the differences in records are due to fraudulent attempts or voluntarily mistreated data.

An independent person should prepare a bank reconciliation statement, so it helps get a more correct and clearer picture of accounts. It keeps accounts up to date and helps simplify accounting errors and theft. In Corporate entities, at the end of every month, the bank reconciliation statement is made and reviewed by two independent persons.

Purpose

The reconciliation statement is maintained for multiple reasons, beginning from detection of tan issue to rectification of it. Let us have a look at the following points to check the reasons for which these statements are prepared:

- The most common objective of preparing these statements is to identify discrepancies. The internal records of financial flows must match the balance reflected in the bank statements. This is because the money is getting in and out from the banks and hence there must be not any mismatch.

- Once the difference is detected, the reconciliation statement lets users adjust the entries wherever the issues are.

- Tracking bounced outflows is yet another task in which these statements help. If a company has to track bounced checks or solen cash, the gaps can help identify such events along with the amount.

- Detection of frauds is possible by analyzing these statements and checking for respective adjustments.

- The accounts payable and accounts receivables are easily trackable.

- When the internal records tally those in the bank statements, annual audits are easy to take and handle.

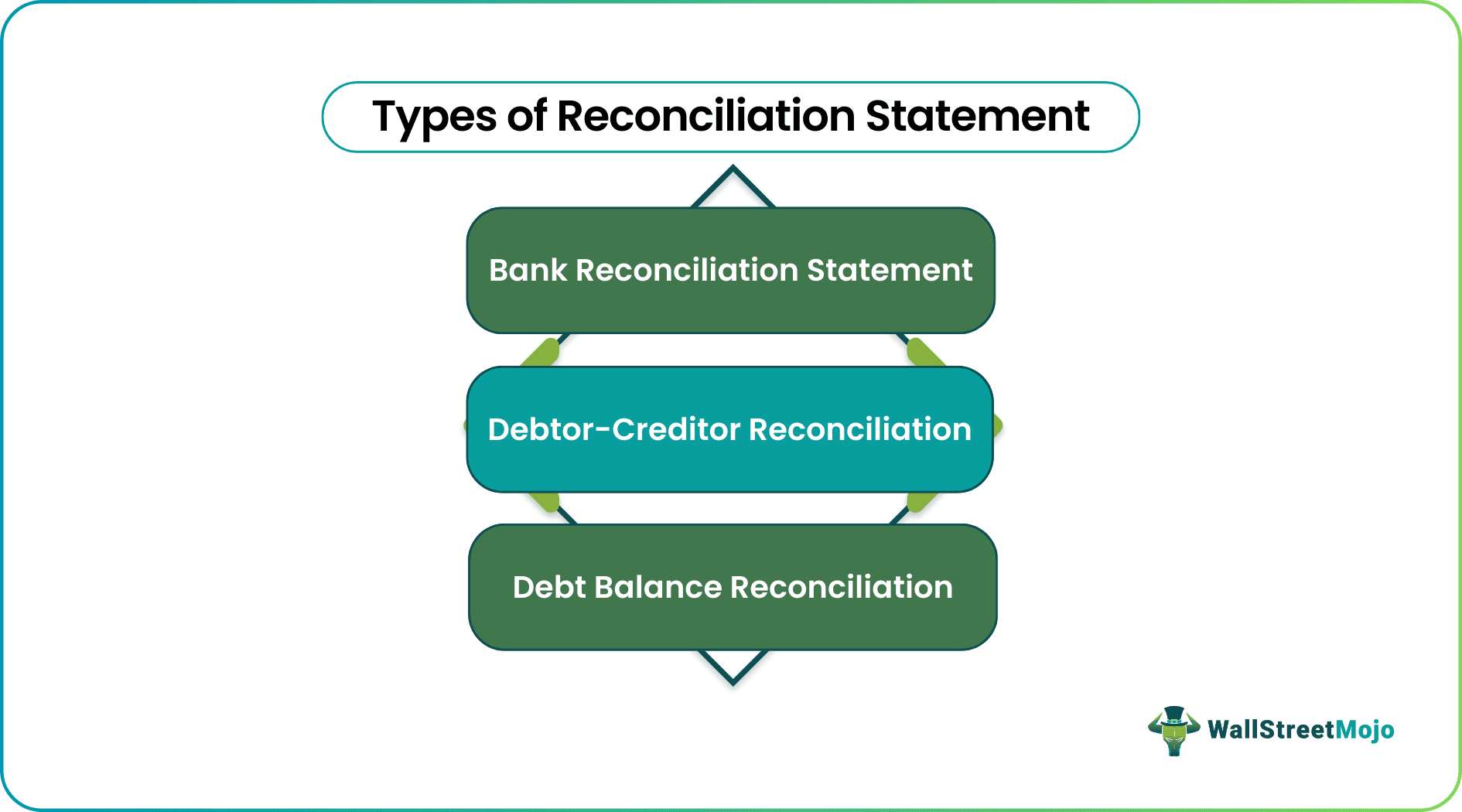

Types

Reconciliation statements exist in multiple forms. Let us have a look at them in brief:

#1 – Bank Reconciliation Statement

Bank reconciliation statement is often called a BRS. It is required to reconcile the difference between bank balances per bank statement and a bank balance per book of accounts. In companies, accounting is on a real-time basis, and sometimes cheque clearing will take time; hence in such cases, there is a mismatch in records of two different entities.

#2 – Debtor-Creditor Reconciliation

Debtor creditor reconciliation is required when there is a mismatch between the balance of the creditor in the debtor’s books and the debtor’s balance in the creditor’s books.

Reasons for differences can be as follows:

- The amount directly deposited by the debtor not recorded by the creditor;

- Debit note and credit notes not recorded by either party

- Goods sold but not yet reached hence not recorded.

Balance reconciliation is required to ensure that all purchases and sales transactions are recorded properly. These are reconciliation items that will lead to a mismatch. Balance confirmation is sought from the top 10 parties as it is audit documentation. The same method, as explained above, can be used to prepare a reconciliation statement.

#3 – Debt Balance Reconciliation

Debt balance reconciliation is the same as the bank reconciliation statement- Debit balance as per bank statement vis-à-vis books of accounts.

Reasons for differences can be –

- Interest accrued not recorded in books of accounts

- Late payment fees and charges not recorded in books of accounts

- The interest amount booked differs from the actual amount the bank charges.

How To Prepare?

The preparation of these statement involves a series of steps. They have been listed below per the reconciliation statement rules and guidelines, essential to be followed by the makers. Let us have a look at them below:

- The first step is to gather all bank records. Companies can obtain all bank balance records and transaction statements online or visit their banks to have a list of transactions for that period.

- The second thing is to have all business records ready. The internal records are to be made available for a quick go-through.

- Have an in-depth look into transaction statements. In the bank statement, the companies are recommended to check the deposits and withdrawals made for the period in question.

- The firms must go through the income and expenses as recorded in the company record books.

- Identify discrepancies in the records maintained by both entities. While reading through the statements from banks and their internal records, businesses must be mindful of noticing any differences between the iflow and outflow reflected in both record books.

- As soon as the differences are identified, the companies should check for anything that they left entering or removing from the statements, by mistake. On detecting the issue, they are required to adjust the entries in the both the record books for accuracy.

- Now when the discrepancies are identified and settled, the last step is to compare the end balance.

Examples

Let us consider the following instance to understand the reconciliation statement meaning and purpose in detail:

Example 1

A bank statement with a bank of America of Disney limited shows a balance of $2000 as of 30th September 2022, whereas the bank balance as per records of Disney limited was $ 4100 on the same date. On detailed scrutiny of two records, the accounting manager found the following transactions are missing in either of the books of accounts.

Cheque deposited in the bank on 29th September not reflected in the bank statement yet amounting to $2500. The cheque was issued to the vendor on 26th September, amounting to $700, not presented and hence not reflected in the statement. On 30th September, the bank debited bank charges to $300 on account of annual maintenance charges plus cheque dishonor charges.

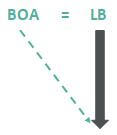

Now let us start with the bank balance as per the bank statement. Bank of America’s (BOA) Balance is $2000, and its ledger balance (LB) is $4100.

Cheque deposited but not cleared $2500.

Explanation: We have to match BOA and LB. At present, LB is higher than BOA balance, so to reach LB from BOA balance, we have to add $2500 to $2000, which makes a total of $4500. The starting point, in this case, is the balance as per BOA. The upward arrow in the above diagram indicates the amount to be added to reach the desired result. Hence $2500 will be added to the BOA balance in the reconciliation statement.

Cheque issued but not presented $700.

Explanation: Cheque issued but not presented will reduce bank balance shortly. Currently the, ledger balance is lower than the bank balance; hence, it should be deducted from the bank balance. The downward arrow in the above diagram indicates that the BOA balance has to reach LB.

Banks directly debit bank charges.

Bank charges debited by the bank will reduce bank balance as per books of accounts and starting point balances as per bank statement; hence this should be added.

The above diagrammatic representation is the easiest way to understand what is to be added and deducted. We aim to match both balances. First, determine your starting point. Based on the transaction, determine which balance will go up and down and make upward and downward arrows. As per the above, if the starting point is bank balance, the arrow should reach the ledger balance.

Let’s see the above example of the reconciliation statement in a tabular format.

Bank Reconciliation Statement

The standard reconciliation statement format to reflect the records as of 30th September 2022

| Particulars | Amount in ($) | Amount in ($) |

|---|---|---|

| Particulars | Amount in ($) | Amount in ($) |

| Balance as per Bank Statement | $2,500 | |

| Add: Cheque deposited | $2,000 | |

| Bank charges debited | $300 | |

| Less: Cheque issued not cleared | $700 | |

| $1,600 | ||

| Balance as per books of accounts | $4,100 |

Example 2

In October 2020, OpenGov, a US-based government software solution provider, introduced a new feature to automate the entire process of reconciliation. This announcement came following its acquisition of ClearRec and rebranding itself as OpenGovBank Reconciliation. This new venture offers government staff with little knowledge on bookkeeping and accounting to follow step-by-step instructions to prepare reconciliation statements. The new software is integrated ERP cloud software, a product of OpenGov itself, to ensure automation of reconciliation statement making.

Advantages and Disadvantages

Undoubtedly, the benefits of preparing reconciliation statements are many. However, anything that has advantages, also exhibit some limitations. And these statements are in no way an exception. Therefore, let us have a look at the merits and demerits of preparing these statements, below:

Benefits

- These statements help identify the transactional mistakes that have been made unintentionally. This normally leads to minimal differences.

- Such statements allow companies to detect frauds reflected through the huge gaps between the inflow and outflow figures.

- Once the unintentional mistakes are identified, executives try to be mindful of them and they do not repeat the mistakes again.

- Time to time reconciliation helps in proper maintenance of company records and no chances of one gap to be stretched broadening the differential gap.

- It helps track payables and receivables.

Limitations

- There are chances of compensating errors to arise in the reconciliation statement. Hence, the accuracy factor is still questionable. An example of compensating error can be the amount received from Mr. Smith credited to the account of Mr. James. Despite this, it is of utmost required as it helps us keep track of unpresented cheques, unknown debits to a bank account direct credit by customers.

- There might be a mismatch in dates recorded in the internal records books and the bank books.

- Checks yet to be cleared might lead to reconciliation difficulties.

Recommended Articles

This has been a guide to what is Reconciliation Statement. Here, we explain how to prepare it, its examples, advantages, purpose, types, and disadvantages. You can learn more from the following articles –

Recommended Articles

Continue with these closely related articles from the same guide.