Part of our Accounting Concepts guide

What Is Accounting Period?

The accounting Period refers to the fixed period during which all accounting transactions are recorded, and financial statements are compiled to be presented to the investors to track and compare the company’s overall performance for each period. A company shall choose its accounting period wisely and not change it unless the conditions arise such that such change becomes necessary.

The accounting period principle allows companies to follow a weekly, monthly, quarterly, or annual form of bookkeeping. Monthly accounting periods are the most common forms of accounting for firms as it gives them enough data to compare their growth trajectory, sales, inflows, and outflows in detail. However, the beginning of an accounting period can depend on the jurisdiction of the business.

- The term “accounting period” refers to the predetermined time frame during which all accounting transactions are documented, and financial statements are collected to be presented to investors.

- Establishing “regular intervals” for recording accounting transactions and compiling results is essential to determine the company’s financial results. Each interval’s results will reflect the company’s financial performance for that specific interval.

- A financial year begins with a full year (for example, the 1st of April and ends on the 31st of March of the next year). Consequently, the financial year is one year long overall.

- Its related accounting transactions must all be recorded during the same time frame. Obligatory accounting provisions must be created to ensure that the matching principle is upheld.

How Accounting Period Work?

The accounting period concept serves the purpose of analysis and comparison of the financial data of the company for two different periods. When two different periods are referred to, analysis can be made regarding various financial parameters that suggest the company’s growth or downfall. Therefore, it serves as a reference to such a report and is very useful for the stakeholders.

Therefore, all the accounting transactions relating to it shall be recorded in the same period. Requiring, mandatory accounting provisions shall be made so that the matching principle is not violated.

Types

Different periods imply different accounting period costs. Let us understand its different types through the discussion below.

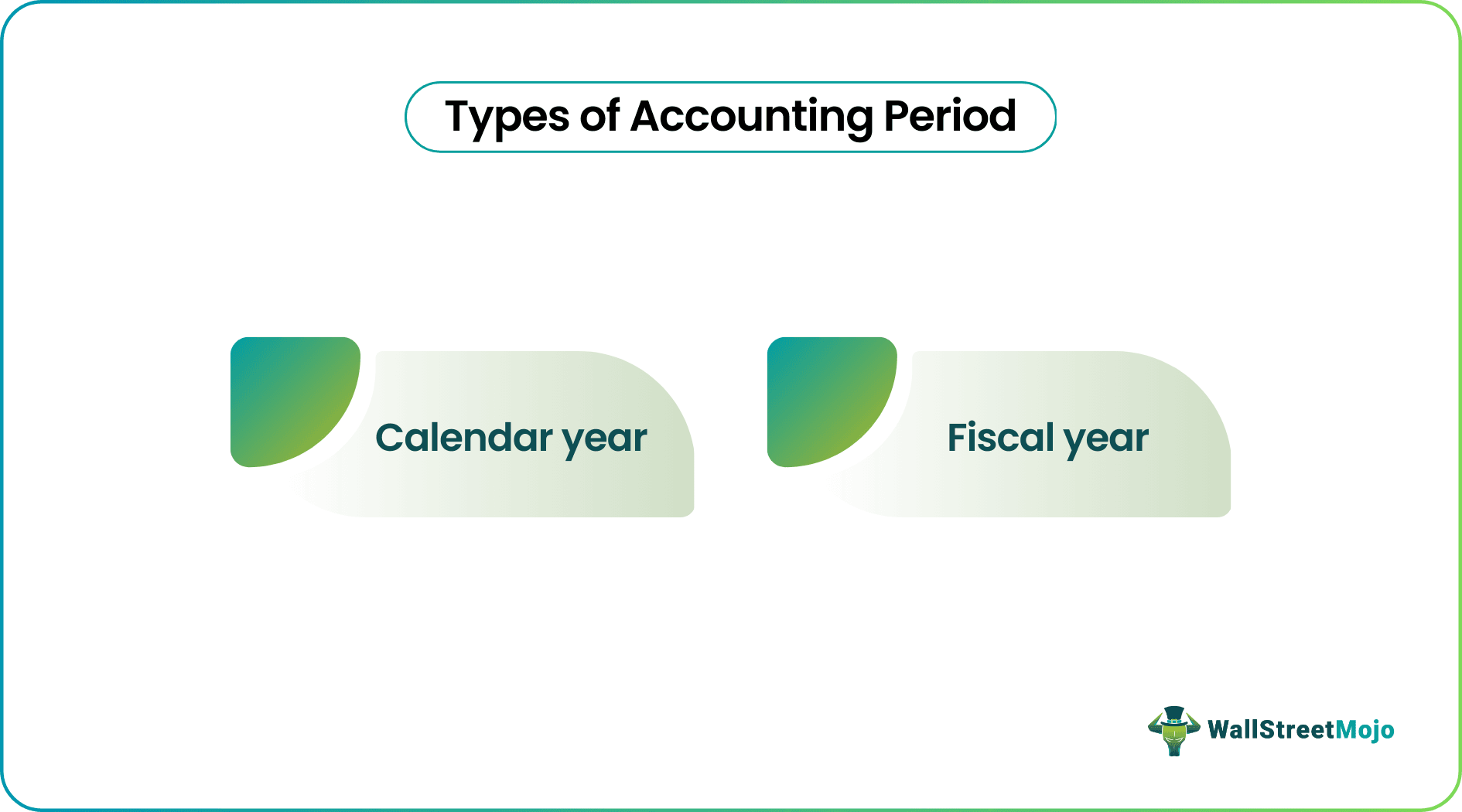

- Calendar Year: For those companies which follow the calendar year, it starts on 1st January and ends on 31st December of the same year.

- Fiscal Year: For those companies which follow the fiscal year, it starts from the first day of any month other than January.

Examples

Let us understand the accounting period concept in detail through the examples discussed below.

Example #1

A company records its transactions from 1st January to 31st December every year and closes its financials. Here, the accounting period is one year, i.e., 1st January to 31st December.

However, not all companies need to follow one year.

Example #2

A company records its transactions from 1st January to 30th June every year and closes its books of accounts after that. Here, the accounting period is that of half-year, i.e., 1st January to 30th June, and the next period shall be from 1st July to 31st December.

Example #3

According to a June 2026 update posted on PeopleSoft Blog, PeopleSoft Asset Management now enables organizations to prevent asset transactions from being processed during the accounting period close.

By restricting asset transactions while financial records are being finalized, organizations can reduce the risk of posting entries to the wrong accounting period and help maintain the accuracy of their financial statements. The feature also supports a smoother period-end closing process by preventing new asset transactions from being processed until the accounting period is reopened or the close is completed.

Importance

The accounting period costs depend on the time frame the company chooses to inculcate. Nevertheless, these costs are almost never given second thoughts as they bring more clarity and definitive data points. Let us understand its importance through the explanation below.

For the company’s financial results to be ascertained, it is crucial to fix “regular intervals” for which accounting transactions shall be recorded, and results shall be compiled. The results of each interval will represent the company’s financial result in each such interval. Thus, the one-by-one comparison is possible only regarding the accounting period. Whether a company has incurred losses or profits is a vague question if any fixed interval is not allotted. Thus, the concept gives meaning to financial statements and helps the investors properly analyze financial results.

Advantages & Disadvantages

Let us understand the advantages and disadvantages of the accounting period principle through the discussion of points from both extremes of this concept.

Advantages

The following are advantages and benefits to the users of the financial statements:

- It is useful in representing the company’s financial position for a fixed interval.

- It is useful in comparison of financial data of two or more periods.

- This concept helps the company set a formal period over which books must be closed.

- The concept is useful for investors as they can refer to the trends of the financial results over several intervals.

Disadvantages

- It may not be useful if the concept of the matching principle is not followed.

- Comparing the results of one period to another does not consider the factual reasons that led to the differences.

- If the tax period is different, two separate accounts will be required to be maintained.

Accounting Period vs. Financial Year

For individuals new to the business world, accounting period concept and financial year often sound like the exact same phenomenon. However, there are differences that have been highlighted through the comparison below.

The accounting period has no fixed length, and it can be of any length, such as one year or less and maybe more than one year. It has two types, namely calendar year and fiscal year. Accordingly, it can start from the first date of any month.

However, a financial year refers to the period starting of one full year (for example, 1st April and ending on 31st March of next year). Thus, the total duration of the financial year is one year, and the starting and end of the financial year are fixed and cannot be changed, unlike the accounting period where the period can be shortened or extended from one year.

Frequently Asked Questions (FAQs)

What is the name of a 12-month accounting cycle?

The government and enterprises utilize a fiscal year (FY), usually a budget year, as the time frame for accounting to create annual financial accounts and reports.

What are the five fundamental accounting concepts?

Five key concepts underlie accounting procedures and the creation of financial statements, even though there are many rules for accountants. The accrual principle, matching principle, historic cost principle, conservative principle, and the principle of substance over form are those.

What does accounting P&L mean?

A profit and loss statement is a type of financial report that details how much your company has made and spent over a certain period. The term comes from the fact that it also displays if you made a profit or loss during that time.

Recommended Articles

This has been a guide to what is Accounting Period. Here we explain its types, examples, importance, advantages, and disadvantages. You can learn more from the following articles –

Recommended Articles

Continue with these closely related articles from the same guide.