Part of our General Ledger guide

Full-Form COA (Chart of Account)

The full form of COA stands for Chart of Account. It is a list of accounts that a company generates to maintain all accounts that have been used for transaction purposes in its accounting system to organize, record, and segregate. This contains various accounts like revenue, expenditure, assets, liabilities, profits, etc.

Chart of account accounting can be used across industries ranging from a simple list in a retail store consisting of 10 to 15 accounts to a very complex coverage in a large business that maintains hundreds of thousands of accounts. Apart from organizing finances, it also gives the stakeholders a clearer vision of the company’s financial health.

Chart of Accounts Explained

Chat of accounts or COA is very helpful for a business in systematically segregating all its accounts. It helps company management and all stakeholders, especially supply chain partners, business analysts, and investors.

This is adjustable per business requirements; however, it requires expertise and effort to keep consistent records in a chart of accounts. Any discrepancy can give the wrong picture of business health. In the modern world of high-tech business management, software and systems are careers, and businesses still owe a great deal of attention and care to handling the most basic elements like the chart of accounts.

A chart of account structure is created in alignment with the business needs. On the one hand, it can contain complex intersections of rows and columns; on the other hand, it can have a straightforward set of accounts. In any case, it should be robust, definitive, and purposeful.

A complex Chart of Accounts may have more features such as allotment of accounting numbers, priority, and detailed information. However, in general, they use a general ledger for their compilation.

A chart of account samples contains at least three sections: Account name, type of account, and description.

The specificity of business units numbers these departments accounts in that order. In the table below, taking account number 103001, the first two digits may signify the department while the rest four denote the account category. Observe the specificity used as a certain number of system codes.

Sample

Since we now know the fundaments and the basic outline of the implications of the concept, let us understand the chart of account accounting with the help of a sample.

| Account Name | Account Number | Description |

|---|---|---|

| Current Assets | ||

| Accounts Receivables | 101001 | $100 |

| Inventory | 101002 | $100 |

| Non-Current Assets | ||

| Plant Property & Equipment | 102001 | $100 |

| Transport | 102002 | $100 |

| Current Liabilities | ||

| Accounts Payable | 103001 | $100 |

| Accrued Liabilities | 103002 | $100 |

| Non-Current Liabilities | ||

| Long-Term Debt | 104001 | $100 |

Example

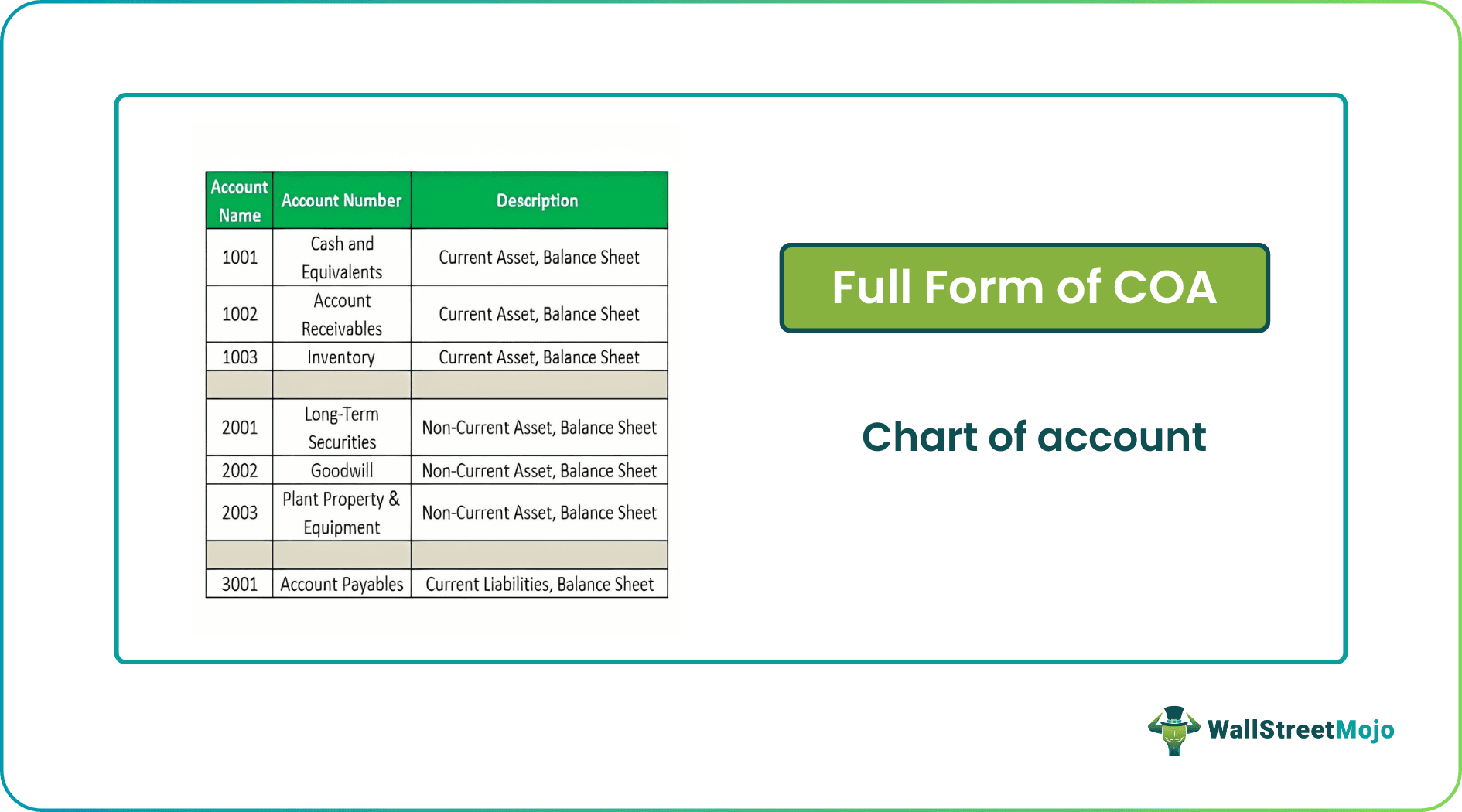

Let us understand the concept of chart of account structure with the help of an example. This example shall help us understand the intricacies of the concept and help us grasp the ebbs and flows of the concept.

Suppose a company buys $1 million worth of land for its manufacturing business. The accounts department must make journal entries to keep records and maintain financial guidelines for the company. The following will be the entry in the books of accounts:

| Account Name | Account Number | Description |

|---|---|---|

| 1001 | Cash and Equivalents | Current Asset, Balance Sheet |

| 1002 | Accounts Receivables | Current Asset, Balance Sheet |

| 1003 | Inventory | Current Asset, Balance Sheet |

| 2001 | Long-Term Securities | Non-Current Asset, Balance Sheet |

| 2002 | Goodwill | Non-Current Asset, Balance Sheet |

| 2003 | Plant Property & Equipment | Non-Current Asset, Balance Sheet |

| 3001 | Accounts Payable | Current Liabilities, Balance Sheet |

On the date, dd/mm/yyyy, account number 2003, Plant property and equipment account, debited with $1 million while account number 1001 credited with $1 million. Notice that the two accounts’ information can be fetched from the Chart of Accounts below.

Types

As discussed earlier, based on the structure of the company, the management can choose to adopt different types of chart of account accounting. Let us understand them through the discussion below.

- Operating: This tracks operative accounts, i.e., regular transaction accounts.

- Business: Which uses all accounts relevant to the business or corporate function.

- Country-Specific: Those who operate based on different accounting standards or legal standards of countries.

Importance

We know that following a chart of account structure helps organize the accounts for organizations. However, there are various other factors that solve a lot of problem relating to accounting for businesses. Let us understand the importance through the points below.

- This is as important as any other element in a business. It serves the purpose of mapping any accounts related to the business. It also helps businesses make better decisions and follow accounting and reporting standards.

- Assume a big supermarket with hundreds of SKUs on sale and thousands of products on its shelves. The supermarket owner’s efficient management is a function of how well he knows his products’ demand and supply profile.

- For this, he maintains an Excel file with definite segregation of the SKUs and products. Whenever any product is sold, an Excel entry is made to reorder it. Likewise, a business maintains all its accounts of financial nature with a chart of accounts to make bookkeeping efficient.

Benefits

Let us understand the benefits of chart of account accounting through the explanation below.

- A good COA is always well-prepared in its initial stages and serves the purpose by further improvisations until it addresses business needs.

- It reduces the effort and time to consolidate information on management requests in the future.

- It can also be used in benchmarking business units and reduces procedures related to reconciliation.

Limitations

Despite the various benefits mentioned above, there are a few factors from the other end of the spectrum that prove to be a hassle for businesses. Let us understand the limitations of adopting a chart of account structure through the points below.

- These are simple and serve no complex requirements of the management.

- It has limited checks and balances, as any error in making a chart of accounts will not be determinable by linkages or checks.

- Even with the limited purpose that COAs serve, companies must follow guidelines set out by the US GAAP (Generally Accepted Accounting Principles) and FASB (Financial Accounting Standards Board).

- It may not be beneficial for small organizations or sole proprietorships because of the disproportionate costs and labor involved in its maintenance.

COA Vs General Ledger

Despite the fact that both chart of account structure and general ledger help businesses organize their accounting, there are differences in their fundamentals and implications. Let us understand the differences through the comparison below.

- A Ledger or General Ledger is the actual book of accounts used for making accounting entries. In contrast, a Chart of Accounts is simply a listing of all accounts related to a company’s business.

- A Ledger is made by summarizing all available journals and then further accounting books like a trial balance. On the other hand, it is an independent record used for further correspondence and recordkeeping.

- Furthermore, a Chart of Accounts can be used by multiple companies for their record. At the same time, Ledger is specific to a company because of its inherent nature of keeping transactional business entries.

Recommended Articles

Recommended Articles

For more on General Ledger, explore these related articles from our General Ledger guide.