Part of our Bond Pricing & Yield Curves guide

What is the Carrying Value of Bond?

Carrying value of a bond is also known as book value or carrying amount of bond and it is nothing but the sum total of the face value and unamortized premiums (if any) less unamortized discounts (if any) of a bond and this amount is usually projected on the issuing company’s balance sheet.

It’s known that bond prices are volatile since they fluctuate daily. As the price is not constant, it causes the bond to be traded at a premium or discount according to the difference between the market rate of interest and stated bond interest on the date of issuance. These premiums or discounts are amortized over the life of the bond, thereby making the value of the bond equal to the face value on maturity.

Key Takeaways

- The bond’s carrying value, also known as the book value or the net carrying amount, represents the amount at which the bond is recorded on the issuer’s balance sheet.

- The carrying value of a bond can be different from its face value, which is the amount stated on the bond certificate.

- If a bond is issued at a discount (below face value) or a premium (above face value), the difference is amortized over the bond’s remaining life.

- The carrying value of a bond can impact the financial reporting and analysis of both the issuer and the investor. For the issuer, it affects the balance sheet presentation and the interest expense calculation

How to Calculate the Carrying Value of Bond?

The effective interest method is one of the most common ways for amortizing premiums and discounts and perhaps one of the easiest methods for computation of carrying value.

For simplicity, let’s assume a firm issuing a 3 year bond with a face value of $100,000 has an annual coupon rate of 8%. The investors view the firm as having considerable risk and are willing to purchase the bond only if it offers a higher yield of 10%.

Since the YTM (yield to maturity) of 10% is higher than the coupon rate (8%), the bond shall be sold at a discount. Thus, its carrying value shall be less than its face value of $100,000.

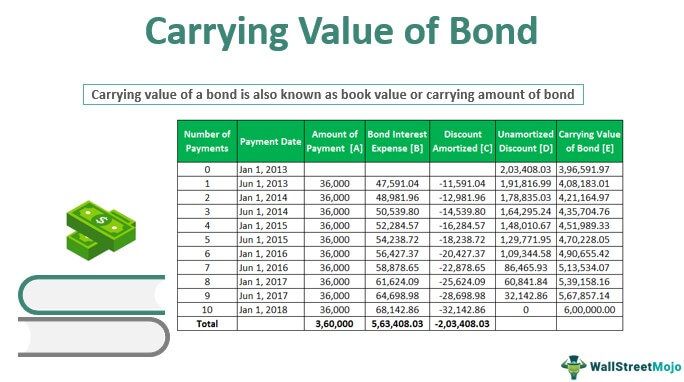

Let us consider another below example with a Bond Amortization schedule for a bond Par value of $600,000 for improved understanding:

| Number of Payments | Payment Date | Amount of Payment [A] | Bond Interest Expense [B] | Discount Amortized [C] | Unamortized Discount [D] | CarryingValue of Bond [E] |

|---|---|---|---|---|---|---|

| 0 | Jan 1, 2013 | 2,03,408.03 | 3,96,591.97 | |||

| 1 | Jan 1, 2013 | 36,000 | 47,591.04 | -11,591.04 | 1,91,816.99 | 4,08,183.01 |

| 2 | Jan 1, 2014 | 36,000 | 48,981.96 | -12,981.96 | 1,78,835.03 | 4,21,164.97 |

| 3 | Jan 1, 2014 | 36,000 | 50,539.80 | -14,539.80 | 1,64,295.24 | 4,35,704.76 |

| 4 | Jan 1, 2015 | 36,000 | 52,284.57 | -16,284.57 | 1,48,010.67 | 4,51,989.33 |

| 5 | Jan 1, 2015 | 36,000 | 54,238.72 | -18,238.72 | 1,29,771.95 | 4,70,228.05 |

| 6 | Jan 1, 2016 | 36,000 | 56,427.37 | -20,427.37 | 1,09,344.58 | 4,90,655.42 |

| 7 | Jan 1, 2016 | 36,000 | 58,878.65 | -22,979.65 | 86,465.93 | 5,13,534.07 |

| 8 | Jan 1, 2017 | 36,000 | 61,624.09 | -25,624.09 | 60,841.84 | 5,39,158.16 |

| 9 | Jan 1, 2017 | 36,000 | 64,698.98 | -28.698.98 | 32,142.86 | 5,67,857.14 |

| 10 | Jan 1, 2018 | 36,000 | 68,142.86 | -32,142.86 | 0 | 6,00,000.00 |

| Total | 3,60,000 | 5,63,408.03 | -2,03,408.03 |

Below is the basis of calculations:

- A = $600,000 * 0.06

- B= E * 0.12

- C = A – B

- D = Prior payment unamortized discount minus current discount amortized

- E = Prior carrying balance minus current discount amortized

Whenever there is an issuance of a bond, a premium or discount account is created, which consists of the difference between the face value of the bond and the cash collected through the sale of the bond. While recording them in the financial statements, the bond premium or discount is netted with bonds payable for computing the carrying value of the bond.

The carrying value/book value of a bond is the actual amount of money an issuer owes the bondholder at a given point in time. This is the par value of the bond less any remaining discounts or including any remaining premiums.

Recording Carrying Value of Bond on Financial Statements

→ Explore all 65 Financial Statements articles

The carrying value or book value of bonds payable includes the following amounts, all of which are found in bond-related liability accounts:

- The face value of the bonds is a credit balance in the account Bonds payable

- The related unamortized discount is a debit balance in the contra-liability account as ‘Discount on Bonds Payable.’

- The related unamortized premium is a credit balance in the adjunct liability account as ‘Premium on Bonds Payable.’

- The unamortized bond costs associated are a debit balance in the contra-liability account.

One should note that the discount, premium, and issue costs are amortized properly up to the moment when the book value of the bonds is needed.

- The carrying value of bonds upon maturity will be equivalent to the par value (amount on which the issuer pays interest and is required to be repaid at the end of the term. For bonds sold at a discount, the carrying value will increase and equal their par value on maturity.

- On the other hand, for bonds sold at a premium, the carrying value will fall and equal the par value on maturity.

Certain structured bonds can have a redemption amount different from the face value and can also be linked to the performance of assets such as FOREX, commodity index, etc. This may result in the investor receiving more or less than its original value on maturity.

Frequently Asked Questions (FAQs)

Does the carrying value of a bond change over time?

The carrying value of a bond may change over time due to the amortization of premiums or discounts, as well as the accrual and payment of interest. Changes in market conditions and the bond’s remaining term can also impact the carrying value.

How does the carrying value relate to the amortization of premiums or discounts?

When a bond is issued at a premium or discount, the premium or discount is typically amortized over the bond’s remaining term. Therefore, this means that a portion of the premium or discount is gradually recognized as interest expense or income over time, which affects the bond’s carrying value.

Can the carrying value of a bond be more significant than its face value?

Yes, the carrying value of a bond can be greater than its face value if the bond is issued at a premium. A premium occurs when the bond’s coupon rate exceeds the prevailing market interest rate. The bonus is amortized over time, resulting in a higher carrying value than the bond’s face value.

Recommended Articles

This has been a guide to the Carrying Value of Bond. Here we discuss how to amortize premiums/discounts and calculate the Carrying Value of Bond and also how to record it on financial statements. You can learn more from the following articles –