Part of our Bond Pricing & Yield Curves guide

What Is Bond Valuation?

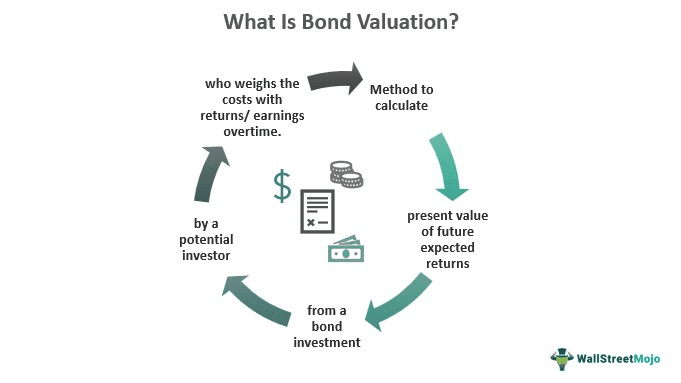

Bond valuation is a method to calculate the present value of the expected future returns, earnings, or cash flow from a bond investment. An investor who invests in a debt instrument such as a bond uses the valuation method to determine whether the cost of the bond is worth the returns over time.

Bond valuations assist an investor in deciding whether the future yields from the bond investment are suitable for their portfolio. Thus, an investor determines the value of a bond through its trading prices, interest rate, and par or face value. While the bond’s interest rates and par value remain the same, changes occur in the bond prices and investors’ returns over time.

Key Takeaways

- Bond Valuation is the method of calculating and estimating the present value of future interest payments to estimate total bond yields at maturity.

- The valuation considers the market interest rate or discounted cash flow rate to value the bond yields accurately for an investor.

- The calculation estimates the interest payments (quarterly, semi-annually, or annually) based on the details mentioned in a bond indenture or agreement. Then adds these annuities to the face value of the bond or principal amount for valuation.

- The par value and interest payments are pre-determined while the investor calculates the return rate.

Bond Valuation Explained

The bond valuation enables an investor to estimate the present value of their future earnings from interest payments and adds it to the bond’s par value or the principal amount.

A bond is a debt instrument, meaning the bond issuer borrows from an investor or lender. In exchange, the bond issuer ensures a fixed interest rate for the period the investor holds the bond. Thus, the interest provides a steady income for the bondholder till the maturity date of the bond. Hence, upon maturity, the borrower repays the bondholder per the face value, less than the face or more than the face value.

On the other hand, a zero-coupon bond will not pay any coupon payments or timely interest to the investor or bondholder. Rather, in the case of a zero coupon bond, the bond price is lowered, or the bond issuer issues the bond at a discounted rate to its face value. Thus, at maturity, the investor receives a guaranteed full amount or par value of the bond. As a result, the difference amount between the purchase price of the bond and the par value at maturity becomes the interest earned by the investor.

Generally, zero coupon bond valuation will result in higher yields to maturity or returns for an investor when the bond matures due to the lower price of the bond at purchase.

A coupon rate is a percentage of the bond’s principal amount or par value. Thus, the timely coupon payments consist of this percentage amount payable to the investor at decided periods, i.e., quarterly, semi-annually, or annually. Hence, factors such as bond price, principal value or par value, coupon rate of a bond, and time to maturity are useful determinants for bond valuation.

Factors

Stock and bond valuation is affected by numerous factors, including changes in the rates of interest, possibilities of inflation, economic conditions, etc. Let us have a look at some of the factors that affect the bond prices:

- Interest rates: When the interest rates change, it affects the discount rate of the bonds issued. In this scenario, the bond prices fall when the interest rates rise and vice-versa.

- Inflation: The expected inflation influences the market in a huge way. The same happens to the bond market. The high expectations of inflation lead to increased rates of interest, thereby lowering the bond prices. However, when the expectations of inflation are low, it’s an opposite scenario, i.e., lower interest rates and higher bond prices.

- Economic conditions: Whether it is the Gross Domestic Product (GDP) or market or customer sentiments, an economy is highly affected. When the economy is towards progress and growth, the interest rates are high and bond prices are low. On the contrary, if the economy is weak, the interest rate is low, and the price of the bond is high.

- Credit rating: The change in the credit rating affects the risk factor associated with an investment. When there is an increase in the credit rating, the credit spread lessens, thereby increasing the price of the bond, while a decrease in the credit rating means a wider credit spread and lower bond price.

- Market Liquidity: A liquid bond market will mean lower volatility in bond value, while an illiquid market will lead to higher volatility in the prices of the bonds.

- Financial state of the issuer: It is one of the most important factors to be taken into consideration. The issuer is the one who requires fulfilling their bond obligations. Hence, their financial status must be assessed. For the issuer of the bond with a well-performing business and fewer debt obligations, the bond price is higher than the issuers with high debt obligations and poorly-performing business.

Methods

The types of bond valuation include traditional, relative, and option-adjusted spread methods.

Tradition Method

This is the conventional means that involves two means of evaluating and pricing bonds. These are discounted cash flow and yield-to-maturity methods. The former is the method used to calculate the present value of the future cash flows from a bond. This helps investors in learning about the returns they can expect from an investment they are considering.

In yield-to-maturity, the investors can calculate the returns that they can expect if the bond is held until maturity. In the process, the current price of the bond is considered along with face value, coupon rate, and maturity period. As a result, investors get a chance to compare bonds and decide where to invest.

Relative Method

As the name suggests, this involves evaluating and pricing a bond with respect to or in relation to other bonds in the market. One such method is credit spread analysis where one bond is compared against a benchmark bond in the market. The credit spread calculated helps investors know about the additional risk associated with the bond being analyzed with respect to that benchmark bond.

The relative method assesses a bond in relation to another bond, which is a benchmark in the market, with similar traits and maturity.

Option-Adjusted Spread (OAS) Method

This type of bond valuation, as the name implies, offers investors an opportunity to adjust their chance of redemption of the bond before maturity. The investors can use callable and puttable bonds and buy and sell the same as and when they realize the potential for profits associated with the bond they hold in the market.

Formula

Let us now look at the bond valuation methods and understand how different determinants contribute. In laypeople’s terms, bond prices are an extremely important and basic determinant for bond valuation outcomes. Thus, if the calculated future price of a bond is high, it holds a high value in an investor’s portfolio and vice versa.

1) Calculating the value of a single cash flow from future coupon payment by estimating its present value for an investor,

Where,

- ‘n’ = Number of years/ number of a coupon payment cycle

- P (v) = Present value of the coupon rate

- CR = Coupon Rate

- F (v) = Future Value

- ‘r’. = Market interest rate, ‘ Discount rate,’ or ‘Yield to maturity.’

A bond’s yield to maturity or discount rate gives the investor an estimate of how their future returns might change due to inflations or currency changes.

- Total Cashflow Formula From Coupon Payments

Or, to calculate the future price of the bond an investor shall use,

2. Total Annuity Formula or Bond Valuation Formula

This formula helps understand how to calculate an investor’s total cash flow or present value of the total annuity by assuming annual or semi-annual coupon payments. This simple formula includes,

How To Calculate?

Bond valuation explains the utility of a bond for an investor. It helps an investor to make a rational choice while making an expenditure or investment based on the current value of future returns. Hence, investors look to invest in a bond that maximizes their returns through higher bond yields to maximize their utility.

Consequently, in the bond valuation calculation, an investor should have certain crucial information for its calculation. Such as,

- Coupon rate

- Estimated coupon payments

- Payment cycles

- Yield to maturity, also known as the discount rate, basically adjusts the future returns based on the market interest rate, inflation, and currency fluctuations.

- Date of maturity of the bond or number of years

Example

Let us now calculate the corporate bond valuation for the investor planning to invest in a bond.

Suppose a 4-year corporate bond is issued with a 12% coupon rate at a $5000 face value. It has a yield to maturity of 10%. According to the bond indenture, coupon payments are payable annually to the investor.

- Present Value Of Single Cashflow From Future Coupon Payments,

- Thus, the estimated future coupon value is F (v) = 12% x $5000

F (v) = $600

- ‘r’ = 10%, representing the actual cash flow or yields the investor shall receive at the bond’s maturity after discounting this rate.

- The timeline for coupon payments is annual. Thus, the investor receives interest or coupon payments after adjustment to the market interest rate.

- Thus, according to the statement, the investor will receive 10% discounted cash flows annually as interest payments till the bond matures. Accordingly, the first annual or coupon payment for the investor will be,

= $545.45

Hence, the first annuity payment for the investor shall be $545.45 after one year from the bond purchase.

2. Total Cashflow Formula From Coupon Payments,

= $ 5,316.99 (Price of the bond after four years at maturity or the total cashflow for the investor)

3. Annuity Formula or Bond Valuation Formula

This formula is a rather simple bond valuation calculator to estimate the future bond valuation for an investor that involves,

= $5316.99

Thus, the future price of the bond after four years at maturity is $5316.99.

Importance

The advantages of using different bond valuation models to assess the price of the bonds are as follows:

- It helps investors figure out the expected return from the bond they hold.

- In addition, they can also assess the risk associated with these bonds.

- When investors are aware of the returns expected and risks associated with the bonds they are issued, they make well-informed investment decisions.

- Based on this valuation, companies can determine the cost of capital to be utilized for debt financing.

Risks

Undoubtedly, evaluating and pricing the bonds is an important aspect of the bond market, but this valuation also has some limitations, which one must know of. Let us have a look at them below:

- The calculations of returns and risks are based on assumptions. In short, the valuation is subjective.

- The changes in the market conditions affect the analysis, thereby influencing the bond valuation.

Frequently Asked Questions (FAQs)

1. How does equity valuation differ from bond valuation?

Although both stocks and bonds are valued using the discounted cash flow method, which assists in calculating the present value of future cash flows from security. However, a major difference between the two securities is that while valuing bond yields, investors will consider interest payments and their future valuation. Thus, bond valuation considers each interest payment segment and adds them to par value.

2. What are bond valuation techniques?

The valuation for this debt instrument or security uses the discounted cash flow method to understand the true value for an investor from bond yields, interest payments, and during bond maturity.

3. How do interest rates affect bond valuations?

Interest rates represent the market interest rates (MIRs) compared to the interest yields from a bond. The comparison and difference between the two interest rates. i.e., MIR and bond interest rate help an investor estimate the present value of future returns. So if the market interest rates are higher, the investor might not be willing to invest in bonds as they may gain higher returns from other investments. Similarly, if the bond interest rate is higher than MIR, then the bond investment is likely.

Recommended Articles

This article has been a guide to what is Bond Valuation. We explain its formula, methods, examples, how to calculate it, factors, importance, and risks. You can also go through our recommended articles on corporate finance –