Part of our Bond Pricing & Yield Curves guide

What Is Biased Expectations Theory?

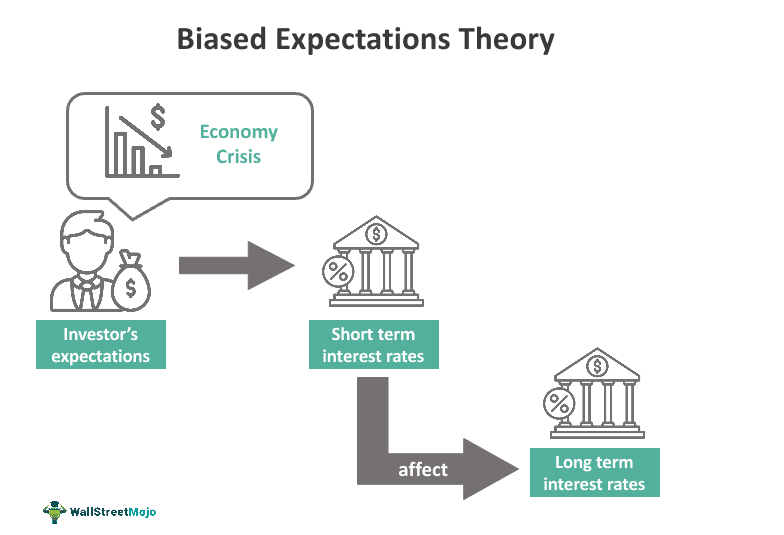

Biased expectations theory is a financial concept that describes how market expectations of short-term interest rates influence long-term interest rates. The primary goal of this theory is to explain how market sentiment shapes the interest rates of financial instruments with longer maturities.

The biased expectations theory has two main variants: the preferred habitat and liquidity preference basis. These theories are further influenced by several factors that impact bonds and deposits, including supply, demand, premiums, and other market conditions. It’s important to note that the term structure of the biased expectations theory differs from that of the unbiased expectations theory.

Key Takeaways

- Biased expectations theory is a financial concept where the long-term interest rates are impacted by the current market rates and investors’ expectations.

- Here, investors can be optimistic as well as pessimistic. If they behave positively, the yield curve will rise ahead. Or else it may lower the future rates of long-duration bonds.

- It includes two types of theory under this type: preferred habitat and liquidity preference theory.

- The only difference between unbiased and biased expectations is that the former attempts to predict how long-term interest rates affect future short-term interest rates.

Biased Expectations Theory Explained

Biased expectations theory is a widely accepted framework that illustrates the relationship between long-term interest rates and the market’s perception of short-term rates. In this theory, investors attempt to predict the future interest rates of long-term financial instruments by relying on market expectations for short-term rates. This implies a causal relationship between the two. The theory aims to understand how investors’ expectations influence current interest rates. For instance, if investors have a pessimistic outlook for one-year bonds, it can lead to fluctuations in the interest rates of five-year bonds.

This theory incorporates several assumptions and factors. Market expectations, premiums, and bias factors play significant roles. The bias factor is subjective and depends on an investor’s expectations. For example, if an investor anticipates that inflation will lead to higher bond interest rates, this is considered a bias factor. However, these biases can vary from one investor to another.

Furthermore, the duration and biased expectations term structure also play a crucial role. According to proponents of the theory, investors’ preferences for bonds with different durations can impact long-term interest rates. Bonds and instruments with longer durations are more significantly affected by short-term ones, leading to varying shapes of the yield curve in the context of the biased expectations theory.

The direction of the yield curve, whether upward or downward, depends on the prevailing market expectations. If investors anticipate that short-term interest rates will rise, they may expect an upward-sloping yield curve, where long-term rates follow suit. Conversely, if expectations change, the yield curve may adjust accordingly. The biased expectations theory seeks to explain these movements in the yield curve.

Types

Based on its function, there are two types of biased expectations theory term structure. So, let us look at them:

#1 – Preferred Habitat Expectations

The preferred habitat theory states that investors cannot consider short and long-term instruments as substitutes for each other. Instead, they need to prefer both based on their maturity. In short, there must be a valid reason to opt for another one. For example, a long-term investor wanting a higher return will prefer higher-yield bonds.

In many cases, investors will not prefer a longer-duration bond if they earn a similar yield from a shorter bond. The only way to switch to the latter is to have the upper hand on the interest rates. However, investors still prefer the former due to the risk attached.

#2 – Liquidity Preference Expectations

As the name suggests, investors tend to give preference to liquid assets. They try to pay more premiums for more liquid instruments. Here, more liquidity depends on the duration of assets. For example, six months or one-year bonds are more liquid compared to four years old maturity bonds.

The theory explains that the term structure strongly impacts long-term interest rates. As a result, the investors will pay more premiums for highly liquid assets. In turn, they tend to accept a lower rate for it. However, for a less liquid asset, they expect a higher return. Thus, the liquidity preference theory for expecting a higher interest rate causes the yield curve to rise high. Therefore, investors will give more preference to short-term securities than long ones. However, the long-term instruments will remain unsold with liquidity risk. As a result, it becomes vital to offer the right premium that balances the risk associated with it.

Examples

Let us look at the examples of biased expectations theory to comprehend the concept better:

Example #1

Suppose Ohan and Lasin are two investors operating in the bond and corporate market. Out of both, the former is a long-term investor, and the latter believes in short-term investment. While both have different choices, they aim at earning higher yields. So, when Lasin was investing, he had two options (a 3-year bond and a 1-year bond), which provided almost equal interest rates. Therefore, he chose the latter. At the same time, Ohan had the same offer, but the risk of the 1-year bond was higher. Therefore, he invested in a 3-year bond.

Here, the investors applied the biased expectations theory for their investment decisions. Their expectations for the bonds less than one year would decide the yield curve of longer bonds.

Example #2

Imagine two friends, Anna and John, considering different savings accounts. With a cautious outlook, Anna prefers a stable 2% annual interest rate. Meanwhile, with an optimistic view of the economy, John expects interest rates to rise and aims for a higher return. Applying the theory, their expectations about short-term interest rates influence their choices. Anna selects a 1-year savings account with a fixed 2% rate, while John opts for a 5-year account with a 4% interest rate, anticipating that rates will increase over the next few years. This example illustrates how personal biases and market expectations can guide investment decisions based on the biased expectations theory.

Biased Expectations Theory vs Unbiased Expectations Theory

Although biased and unbiased expectations theory involves the calculation of future interest rates, they have wide characteristics. Therefore, it is crucial to look at their differences:

Frequently Asked Questions (FAQs)

What are the drawbacks of the biased expectations theory?

The primary drawback of this theory lies in its reliance on the bias factor. Bias introduces a significant level of uncertainty, as it varies from one investor to another and can change over time, making it challenging to predict accurately.

Why are biased expectations theories of the term structure of interest rates considered biased?

These theories are considered biased because they incorporate a bias factor that represents investors’ preferences. This bias factor is essential, as it reflects investors’ perceptions, preferences, and choices, which, in turn, influence the demand and supply of financial instruments. Therefore, bias is a fundamental aspect of these theories.

What assumptions underlie the biased expectations theory?

The biased expectations theory operates under certain assumptions. It assumes that all information regarding financial instruments is readily available in the market. Additionally, it assumes that investors act rationally, making informed decisions throughout the process.

Recommended Articles

This has been a guide to what is Biased Expectations Theory. We explain its types, examples, and comparison with unbiased expectations theory. You can learn more about it from the following articles –

Recommended Articles

Continue with these closely related articles from the same guide.