Credit Default Swaps (CDS) Definition

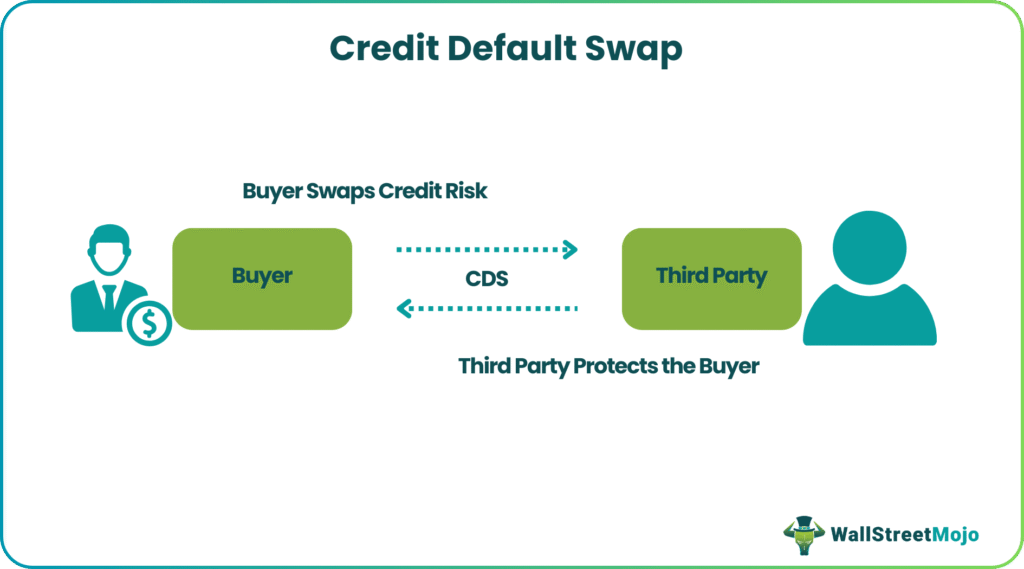

A Credit Default Swap (CDS) is a financial agreement between the CDS seller and buyer. The CDS seller agrees to compensate the buyer in case the payment defaults. In return, the CDS buyer makes periodic payments to the CDS seller till maturity.

In the event of default, the seller pays the entire agreed amount, including interests. Primarily, the CDS shifts the risk exposure away from the buyer. Usually, buyers swap to protect themselves from the default of government bonds, corporate debts, and sovereign bonds.

Key Takeaways

- A Credit Default Swap is a type of insurance that protects a party against payment defaults.

- In return, the buyer has to pay interest over the agreed period of time.

- In case of a default, the seller has to pay the entire agreed amount, including the interest.

- CDS was bought for leveraging portfolios, hedging, arbitration, and speculation.

- In the 2008 financial crisis, AIG lost $99.2 billion. $30 billion of the losses were due to the collapse of CDS.

Credit Default Swap Explained

CDS were invented so that the buyer could shift the burden of risk in case of payment defaults. It acts like an insurance policy wherein the buyer is supposed to make regular periodic payments to the seller. Typically, buyers swap to protect against the default of government bonds, corporate debt, and sovereign debt.

CDS is also known as a credit derivative contract or instrument. Derivative Contracts are formal contracts that are entered into between two parties, namely one buyer the other a seller. Thus, they act as Counterparties for each other. Such a contract involves either physical transaction of an underlying asset in the future or financial payoffs where one party pays another based on an underlying asset.

Although similar, CDS is different from insurance. Unlike insurance sellers, CDS sellers are not required to be regulated entities. Although most CDS sellers are banks, some sellers are less accountable. Unlike insurance, CDS sellers are not required to maintain a reserve. As a result, if there is a default, a CDS seller might lack the funds to pay the buyer back.

Credit Default Swap Examples

Consider the following example. A company issues a bond; the bondholders bear the risk of non-payment. To shift this risk exposure, bondholders could buy a CDS from a third party. This will shift the burden of risk from the bondholder to the third party. In return, the buyer of CDS pays interest periodically. Usually, these third parties are banks, hedge fund companies, and insurance companies.

Consider another example. Thomas buys a bond from XYZ Ltd. at a face value of $1000 with a coupon rate of 10%. So, Thomas is supposed to receive $100 per annum ($1000*10%). Here, Thomas bears the risk of non-payment by XYZ Ltd. So, to shift the credit risk, Thomas swaps with Sheehan Enterprise. Sheehan, in return, charges $20 per annum. Sheehan Enterprise will pay Thomas the principal amount of the bond and the coupon amount every year.

Now in case of no default, Sheehan will end up making a profit of $20 per annum, and Thomas benefitted by being risk-free.

Pricing of CDS

The pricing of CDS is determined by the Hull and White valuation model. The details of the pricing model are as follows.

- The Hull and White valuation model

This is the most used CDS valuation. According to Bloomberg, the following equation gives the present value of payments to be made for the agreed period:

The next task is to calculate the spread of CDS which could be calculated using the following equation:

Pros and Cons of CDS

CDS has the following advantages. These swaps protect the buyer against the risk of non-payment by an entity. The cost of such protection is very low. Due to the lower risk, the buyer can invest in riskier investments. This simply means more investment and could push the national economy upwards.

The sellers have a portfolio with a vast diversity of such swaps, which covers the risk of one or more swaps going default. So at the end of the day, they end up making a good profit.

CDS disadvantages are overlooked. The swaps went unregulated for the longest time till 2010. There was no one to ensure whether the seller of CDS had enough reserve money to pay the buyer in case of a default. CDS sellers further mitigate risk by hedging with other CDS deals.

How CDS caused the financial crisis of 2008?

According to Reuters, the major companies that sold swaps during 2007 were American International Group (AIG), Pacific Investment Management Company, and Citadel Hedge Fund. Lehman Brother, a leading investment banking company, owed $600 billion in debt. $400 billion of which were covered by swaps.

CDS are largely over-the-counter instruments. That means they are not traded on an exchange. One bank just agrees with another bank to do a CDS deal. There was no reliable central agency providing information. Banks all over the world bought CDS protection from AIG. In 2008, AIG was not able to make good on that promise of payment. As a result, every one of those banks lost that protection. The companies that sold swaps did not expect this magnitude of payment defaults. Nor were they prepared for a financial crisis. The lack of liquid cash or liquidity failed these companies.

AIG was a global company with about $1 trillion in assets prior to 2008. But during the financial crisis of 2008, AIG lost $99.2 billion. The company’s Credit Default Swaps caused the collapse. It ended up costing AIG $30 billion. Finally, Federal Reserve had to bail out AIG. But nothing could stop the downfall of the CDS market. Investors realized that CDS was not capable of insuring large capitals. Eventually, people stopped buying CDS.

Frequently Asked Questions (FAQs)

How does credit default swap work?

The credit default swap index (CDX) tracks and evaluates total returns for different areas of the bond issuer market, allowing the index’s overall return to be compared to funds that invest in similar products.

Can anyone do a credit default swap?

Almost anyone can purchase a CDS. Like most other derivatives, credit default swaps can be employed by investors who do not own the asset but want to profit by holding a position in it. Such an agreement is called a naked credit default swap.

How much does a credit default swap pay?

When a bond defaults, the CDS buyer is entitled to the notional principal less the bond’s recovery rate. Its value determines the bond’s recovery rate shortly after default. So, if the recovery rate on bonds worth $1,000,000 is 75%, then the CDS payout is $250,000.

Recommended Articles

This has been a guide to Credit Default Swap (CDS) and its Definition. Here we discuss how credit default swap work along with pricing, examples, pros & cons You can learn more from the following articles –