Credit Derivatives Meaning

Credit derivatives (CDs) are derivative contracts that enable a lender to transfer a debt instrument’s credit risk to a third party in exchange for a payment. However, there is no actual transfer of ownership of the instrument. They protect the lender against the loss associated with the risk of default by the borrower.

CDs are extensively used in the commercial banking sector across the US. The banks use them to mitigate credit risk exposure and expand their credit portfolio. In addition, insurance companies also use them to improve returns on their asset portfolio. CDs are traded over the counter, and their price depends on the borrower’s credit rating.

Key Takeaways

- Credit derivatives (CDs) are a type of derivatives instrument that allows the transfer of credit risk from a lender to a third party against payment of a fee.

- Credit risk is the risk of loan or debt default.

- There are three parties to a credit derivative contract: borrower (reference entity), lender (protection buyer), and third party (protection seller).

- Credit derivatives may be funded or unfunded. They include credit default swap, credit spread option, credit linked note, and collateral debt obligation.

- CDs are the buffer against economic volatility.

Credit Derivatives Explained

Lenders or investors possess varying degrees of risk tolerance. Debt securities come with several types of risk: interest rate, liquidity, credit, prepayment, etc. To hedge them, investors enter into a derivative contract. Derivatives are financial instruments that confer the same value as their underlying financial assets to the holder without the right of ownership over them.

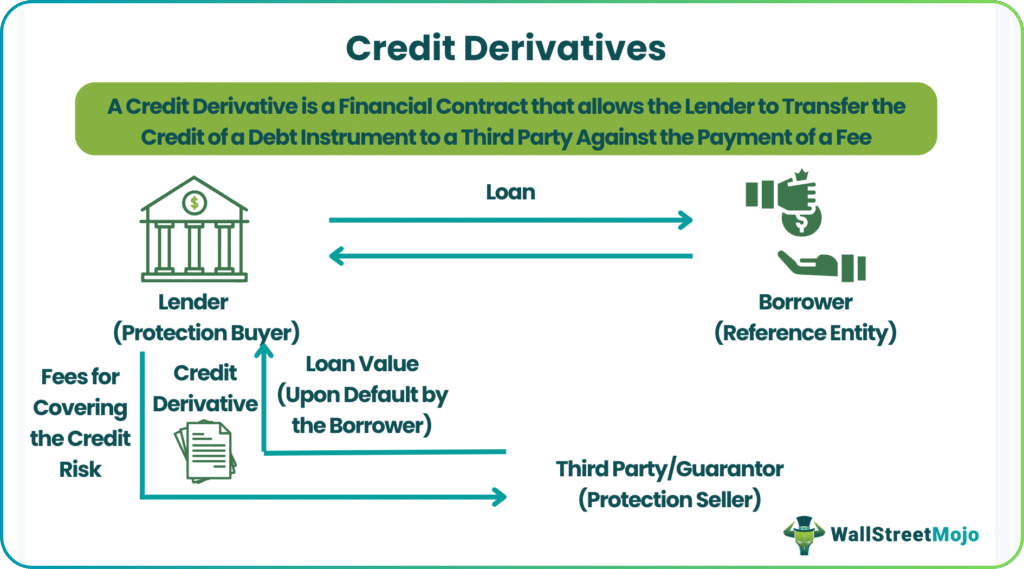

Therefore, a credit derivative is a type of derivative contract that derives its value from the underlying debt instrument and is used to protect the lender against credit risk. Credit risk means the risk that borrowers may default on their loan or debt obligations.

To reduce the potential credit risk exposure related to risky borrowers, lenders enter into a CD with a third party (counterparty) for selling debt securities without the transfer of their ownership. The counterparty guarantees to cover the default on a loan or debt on behalf of the borrower in return for a certain sum.

Thus, if the loan account defaults, the lender gets the securities’ value repaid as per the credit derivative agreement. But if the loan account comes to a successful closure, the counterparty gets to keep the exorbitant fees it charges for providing the insurance to the loan.

How do the Credit Derivatives Function?

A CD involves mainly three participants:

- The borrower who needs credit (reference entity)

- The lender who needs insurance for the loan (protection buyer)

- The third party or the guarantor who wants to profit by covering the risk of a loan default (protection seller/counterparty)

Let us suppose that the borrower, an XYZ Coffee Shop, needs a credit line of $100000 for developing its business. However, the firm has an unhealthy credit rating amongst financial institutions.

Now, suppose the XYZ Coffee Shop applies for the credit of $100000 from the ABX Bank. In that case, it will face a hurdle in securing the loan from the bank owing to its bad credit record.

In this case, the bank will issue the loan. However, it will enter into a contract with a third party to mitigate the credit risk associated with the loan. Such a contract is referred to as a credit derivative.

Here, ABX Bank is the protection buyer, the third party is the protection seller, and XYZ is the reference entity. ABX will have to pay a certain fee to the third party in lieu of covering the risk of loan default for the term of the CD contract.

The value of the CD will depend on the creditworthiness of the reference entity and the third party. The CD will enable the bank to transfer the entire loan default risk to the guarantor or the third party.

Therefore, if the XYZ coffee shop defaults on its loan, the third party will pay the remaining amount or the interest of the loan to the bank and close the loan. However, if the XYZ Coffee shop doesn’t default upon its loan, the third party retains the fees on the CD contract.

Hence, in the light of the above explanation, we can see that the CD has:

- Enabled the credit line to the XYZ Coffee Shop

- Covered the credit risk of the loan account of the ABX bank and

- Benefitted the third party in terms of fees received from the ABX bank

Types of Credit Derivatives

CDs are useful instruments for offloading a lender’s credit risk to a third party and securing its credit asset. There are two main categories of CDs: Unfunded and Funded.

#1 – Unfunded Credit Derivatives

Unfunded CDs are instruments where the protection buyer (lender) does not receive any initial payment from the protection seller (counterparty) for covering the credit risk. Under such a contract, the counterparty pays only when the borrower defaults. Therefore, unfunded CDs expose the lender to the risk of default from the counterparty.

There are different types of unfunded CDs.

Credit Default Swap (CDS)

In this type of contract, both the protection seller as well as the protection buyer of the credit asset negotiate a deal where:

- The buyer undertakes to make regular payments (swap spread or premium) to the seller over the term of the contract, and

- The seller makes good the loan in the event of default by the borrower or reference entity.

It is the most popular derivate product, widely used in the commercial banking sector.

Credit default swap option

It is a contract that offers its buyer a right, without obligation, to enter into a CDS agreement on a future date at a specific strike price.

Credit spread option

This type of CD involves simultaneously buying and selling an option of the same class (with the same underlying asset and expiry date) at a different strike price. The difference in the strike prices yields profit.

Total-rate-of-return swap

It involves the transfer of both credit and interest rate risks associated with the underlying financial asset to a third party. Here also, the transfer of risk is without the transfer of the ownership of the underlying asset.

#2 – Funded Credit Derivatives

Funded CDs are instruments where the lender is not exposed to the credit risk from the counterparty. This is because the counterparty pays an appropriate sum to the lender to cover any loan default in the future. Now, let’s discuss the different types of funded CDs.

Credit linked note (CLN)

It is a type of funded CD that allows the protection seller to transfer a specific set of its credit risk to a third party (investor in the note). If the borrower doesn’t default, the note is redeemed at par at maturity. However, if the default occurs, it is redeemed at less than the par value.

Constant Proportion Debt Obligation (CPDO)

It is a type of CD that allows the investors exposure to credit risk through a note that has the credit rating embedded in it. This is done to utilize the dynamic leveraging of trades. CPDO offers high yields with low credit risk.

Collateralized debt obligation (CDO)

It is a form of CD where banks collect all their loans and make a bundle that acts as debt instruments. These instruments are backed by an asset or collateral security and then sold to the investors in small parts after splitting them into tranches. They are only available for sale to institutional investors.

Examples of Credit Derivatives

Example #1

Let us assume that Lehmann Brothers (LB) purchases bonds issued by General Electric (GE) in large amounts. LB expects GE to pay some good returns on its bonds semi-annually. But LB is afraid that if GE goes bankrupt, it will lose money.

So, LB decides to buy credit default swaps (CDS), a form of CD, from AIG in order to secure its investment based on GE bonds. Thus, if GE goes bankrupt, LB will get its investment from AIG. But, on the other hand, if GE never fails, it keeps getting the returns from GE. However, it has to forgo the amount it paid as a premium for the CDS.

Example #2

Suppose a company XYZ is issuing a bond with a $1 million par value and 7% coupon rate. ABC Bank has excess funds at its disposal and is willing to invest in XYZ bond. However, XYZ is rated low by the credit rating agency. Therefore, ABC bank seeks a credit default swap (CDS) from MNM to mitigate its exposure to credit risk.

ABC will pay 1% of the face value of the bond (fees) to MNM in return for its insurance against XYZ’s default. If XYZ defaults, ABC (CDS buyer) will get a payment from MNM (CDS seller). However, if XYZ doesn’t default, MNM stands to benefit as it gains the fees without covering for any default.

Frequently Asked Questions (FAQs)

What are credit derivatives?

CDs are financial instruments that derive their value from the underlying asset without actually owning it. Hence, they act as a risk-hedging tool for banks to protect them from the credit risks of a high-valued loan if it defaults. Banks mostly use CDs as an insurance policy on debts or loans.

What are the benefits of credit derivatives?

They help in bringing macro-economic stability as markets become more efficient and liquid. In addition, they facilitate effective pricing and credit risk distribution among market participants.

What are the risks in credit derivatives?

Credit derivatives come with the risk of default by the protection seller. This was why AIG, one of the world’s largest insurers with over $1 trillion in assets, reached the brink of collapse in 2008. The insurer’s subsidiary AIG Financial Products (AIG FP), engaged in credit-default swaps for banks, financial institutions, and hedge funds. However, they couldn’t cover the simultaneous default of a large number of debt instruments.

Recommended Articles

This article has been a Guide to Credit Derivatives. Check out the meaning, types, examples of credit derivatives & how lenders use them to swap their credit risk. You can learn more from the following articles –