What Is A Total Return Swap?

A total return swap (TRS) is a contract that involves one party making payments based on a set rate and the other party making payments depending on the return generated by an underlying asset. This allows the party receiving the returns to benefit from the underlying asset without owing it.

Usually, the underlying or reference asset is a basket of bonds, loans, or an equity index. The person receiving payment at a set rate owns the asset. Financial institutions utilize these swap agreements to manage risk exposure with negligible expenditure. The asset’s returns include depreciation/appreciation, and any earnings generated, for example, interest payments or dividends.

- Total return swap meaning refers to derivative contracts in which a party pays fees to another party based on a specific rate. In exchange, the other party pays the return earned on the reference asset, including interest payments and dividends.

- There are various advantages of total return swaps. For example, it allows the total return payer to remain the owner of the underlying asset while allowing the total return receiver to benefit without owning the asset.

- Unlike repo, TRS agreements do not involve the physical transfer of assets.

- Total return swap agreements come with counterparty and credit risks.

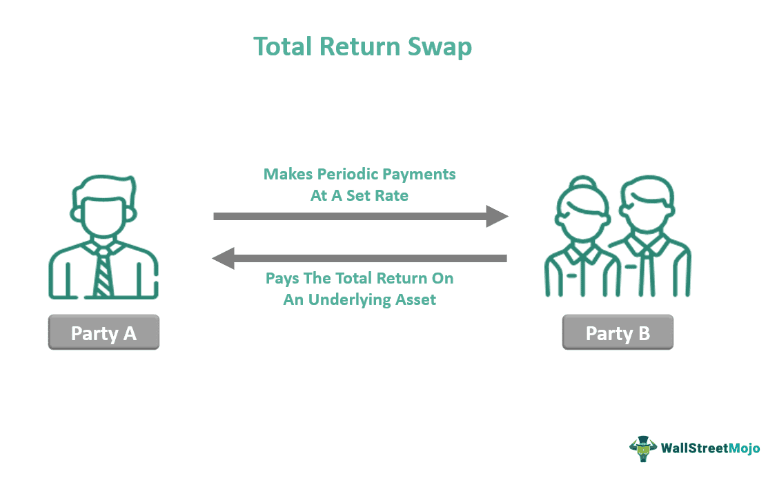

How Does Total Return Swap Work?

The total return swap meaning refers to a financial derivative contract in which a party pays the overall return on an underlying asset and, in return, receives periodic payments from another party at a special rate. Usually, banks, hedge funds, insurance companies, and portfolio managers are the total return payers. They utilize these swap agreements to manage risk by incurring a minimal cost.

The two parties involved in a total return swap agreement are the total return receiver and the total return payer (the asset owner). Total return payers agree to pay the total return receivers the overall returns generated by the reference asset while receiving London Interbank Offered Rate or LIBOR-based returns in exchange.

The underlying asset’s owner forfeits the financial risk associated with it. That said, the person bears the credit exposure risk. For instance, if the asset’s price decreases before the expiry of the contract, the total return receiver pays a sum equivalent to the amount by which the asset price fell.

Thus, simply put, the total return payer purchases protection against a possible decrease in the underlying asset’s value by agreeing to pay the total positive returns generated in the future in return for floating payment streams. This concept is similar to bullet swaps. However, in the case of bullet swaps, payments do not happen until the position closes or the swap ends.

Examples

Let us look at these total return swap examples to understand this concept better.

Example #1

Suppose company DBC and ZNQ entered a total return swap agreement. The former agreed to pay the latter the overall return on a basket of bonds over three years. company DBC paid ZNQ as the underlying asset’s price increased during that timeframe. That said, if the reference asset’s price decreased during that period, company ZNQ would have made payments to company DBC.

Example #2

Suppose two parties (A and B) enter into a TRS agreement. According to the terms, A receives LIBOR and an extra 2% fixed margin. B gets the overall return on the S&P 500 Index on a principal amount worth $3 million.

After a year, if the LIBOR is 4% and the index value increases by 12%, A pays B 12% and, in return, gets 6%. After netting the payment at the end of the TRS agreement, B received $180,000 [3 million x (12% – 6%)].

Tax Treatment

TRS is a form of equity swap. Hence, its tax treatment falls under notional principal contracts. The Internal Revenue Service or IRS needs the taxpayers to differentiate between non-periodic and periodic payment instruments in such agreements. The taxation guidelines are simple for the notional principal contracts involving periodic payments.

The IRS needs taxpayers to recognize a ratable daily part of periodic payments for a taxable duration to which that part relates. Nevertheless, the accounting method utilized by taxpayers does not play any part in deciding how TRS taxation happens.

One must note that TRS may be subject to taxation for taxpayers who obtains the payments. This is because the taxpayer can get different kinds of returns, for example, dividends and capital gains. Under regular taxation, such returns fall into separate categories. That said, in the case of TRS, all types of returns are considered earnings, falling under the federal income tax rules.

Advantages And Disadvantages

Let us look at the benefits and limitations of TRS:

Advantages

- These agreements offer operational efficiency; the total return receivers do not have to deal with payment calculations, settlements, interest collections, etc.

- The total return payer or asset owner retains the ownership of the underlying asset.

- Such a contract allows total return receivers to make a leveraged investment; they do not have to acquire the asset to obtain the benefits.

Another key advantage of total return swaps is that they allow investors access to restricted markets.

Disadvantages

- These agreements carry interest rate risk.

- Investors may incur losses if the underlying asset’s price or the overall returns keeps fluctuating. However, they must pay the interest irrespective of the losses. This is counterparty risk; it is higher for hedge funds.

Total Return Swap vs Repo vs Credit Default Swap

Investors often find the concepts of total return swap, repo, and credit default swap confusing. However, eliminating such confusion is essential to avoid making wrong financial decisions. In that regard, one must know their critical differences. So, let us look at them.

| Total Return Swap | Repo | Credit Default Swap |

| TRS is a swap agreement in which one party pays fees at a certain rate to another party in exchange for the returns generated by the reference asset owned by the second party. | A repo is a short-term secured loan. In this case, a party sells government securities to another party, agreeing to buy them back at a higher price. | This type of financial derivative contract enables investors to offset or swap their credit risk with another investor. |

| TRS outsources market and credit risk. | Repos come with credit risk and interest rate risk. | A credit default swap or CDS outsources only credit risk. |

| TRS doesn’t involve the physical transfer of an asset. | It involves the sale of securities. | Unlike repo, credit default swaps do not involve an actual sale of financial instruments. |

Frequently Asked Questions (FAQs)

Are total return swaps OTC?

A TRS agreement is an over-the-counter or OTC contract. It captures the agreement between two entities to exchange the underlying or reference asset’s total return.

Are total return swaps off balance sheet?

The total return receiver is not the legal owner of the underlying or reference asset, just like a lessee is not the legal owner of a vehicle. Total return swaps are off-balance sheet transactions; the underlying asset does not appear on the total return receiver’s balance sheet.

How do hedge funds use total return swaps?

It is common for hedge funds to use these financial derivative contracts. This is because by entering such agreements, hedge funds can get exposure to the reference asset without making a significant investment.

Who regulates total return swaps?

The SEC or Securities and Exchange Commission, and the CFTC, or Commodity Futures Trading Commission, regulate the total return swap market.

Recommended Articles

This article has been a guide to what is a Total Return Swap. We explain its examples, compare it with repo and credit default swap, tax treatment, and advantages. You may also find some useful articles here –