What Is A Variance Swap?

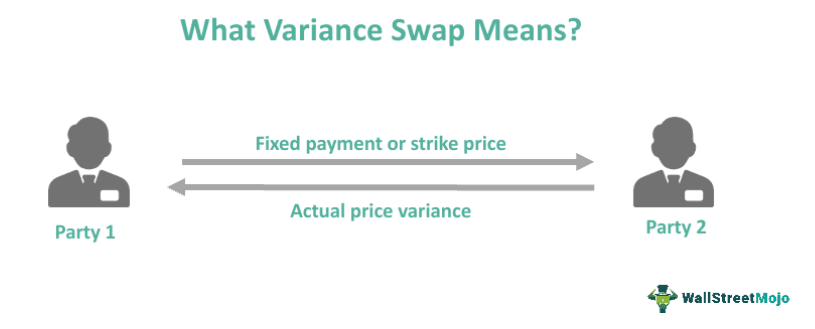

A variance swap is a type of financial derivative where one party agrees to pay the other party the difference between the realized variance and a pre-agreed-upon strike variance of the underlying asset over a specified period of time. It enables investors to speculate on or hedge against an underlying asset’s volatility.

The major benefit of variance swap pricing is that it allows investors to speculate on or hedge against an underlying asset’s volatility regardless of the underlying asset’s price direction. Hedge funds and other institutional investors commonly use it to manage portfolio volatility risk.

Key Takeaways

- A variance swap is a financial derivative contract in which the buyer and seller agree to exchange fixed payments for the seller’s promise to pay the buyer an amount based on the variance of price movements.

- It primarily enables investors to speculate on or insure against the volatility of an underlying asset.

- Hedge funds and institutional investors commonly use variance swaps to manage portfolio volatility risk.

- Unlike variance swaps, in volatility swaps, the buyer agrees to pay the seller the difference between the realized volatility and the strike volatility.

Variance Swap Explained

A variance swap allows the buyer to speculate on the volatility of an underlying asset without owning it or using other derivatives, such as options. Instead, the buyer agrees to pay the seller a fixed amount known as the strike price. This is in exchange for the seller agreeing to pay the buyer the square of the difference between the underlying asset’s average value and the strike price multiplied by a predetermined number of days. A stock index, a currency, a commodity, or any other financial instrument with a measurable level of volatility can serve as the underlying asset.

When the underlying asset’s volatility exceeds the strike price, the buyer of the variance swaps profits. And the seller will incur a loss, as will the buyer.

A variance swap has the following key characteristics:

- Volatility Exposure: The main purpose of the swap is to allow investors to speculate on or hedge against an underlying asset’s volatility. Volatility measures the uncertainty or risk in an asset’s or derivatives’ value.

- Complexity: They are complex derivatives that sophisticated investors and institutions typically use. They necessitate a thorough understanding of volatility and the concepts that underpin it. They also demand advanced mathematical and statistical techniques.

- Determining Positions: It allows investors to take a position on volatility independent of the underlying asset’s price direction. For example, an investor with a long position may want to hedge against the risk of a stock price decline. But they may also want to benefit from an increase in volatility.

- Hedge Funds And Institutional Investors: They are helpful for hedge funds and other institutional investors to manage volatility risk in their portfolios. Additionally, traders use them to speculate on volatility.

- Short-Term Contracts: They typically have a short-term contract period, usually less than a year.

Examples

Let us look at a few examples to understand the concept better:

Example #1

Let us assume that a hedge fund manager considers that the volatility of a particular stock will fall in the future. They could enter into a variance swap pricing contract with a counterparty. They can thus agree to pay a fixed amount if the stock’s volatility rises and receive a variable amount if the volatility falls. It enables the hedge fund manager to profit from their belief that the stock’s volatility will fall. They can also limit their potential losses if the volatility rises.

Example #2

An investor anticipates that the volatility of a specific stock will rise in the future. A variance swap could be entered between the investor and a counterparty, such as a bank. The investor would pay the counterparty a fixed strike price under the terms of the swap. And the counterparty would pay the investor the square of the difference between the realized volatility of the stock and the strike price. If the realized volatility of the stock is greater than the strike price, the investor will profit. Otherwise, the investor will lose.

Variance Swap Replication

Replicating a variance swap pricing involves making a separate investment with the same potential payoffs as the variance swap but in a simpler and less expensive form.

A popular replication strategy combines long and short positions in options on the underlying asset with different strike prices and expiration dates. The portfolio is designed so that the total payoff from the options equals the variance swap payoff.

An investor can gain exposure to the volatility of an underlying asset without directly trading it by replicating a swap. It can also hedge against an existing position in the underlying asset.

Variance Swap vs Volatility Swap

- A variance swap is a derivative contract in which the buyer agrees to pay the seller the difference between an underlying asset’s realized variance and a predetermined strike variance, usually over a set period. A volatility swap is a similar type of derivative contract in which the buyer agrees to pay the seller the difference between the realized volatility of an underlying asset and a predetermined strike volatility rather than the variance.

- Variance Swaps are more commonly used for hedging purposes because they accurately represent the underlying risk. Volatility swaps are more commonly used for speculation because they are widely understood and used as a metric.

- Variance is calculated as the average squared differences between the returns and the mean return. Volatility, on the other hand, is calculated as the standard deviation of the returns.

Frequently Asked Questions (FAQs)

What is vega notional in variance swap?

In a variance swap, the vega notional is the dollar amount per unit of volatility used to calculate the payout. It represents the payout’s sensitivity to changes in the underlying asset’s implied volatility. The vega notional standardized swap payouts allow traders to compare them across different assets and markets.

What is a corridor variance swap?

A financial derivative known as a “corridor variance swap” ties the payout to the variance of an underlying asset’s actual volatility to a predefined range or “corridor.” If the realized volatility is greater than or less than the top or lower bounds of the corridor, the swap buyer is paid. If the realized volatility is within the corridor, the buyer must pay.

What is the delta of a variance swap?

The delta of a variance swap measures how sensitive the swap’s value is to changes in the underlying asset’s price. In contrast to conventional options, variance swaps do not have a straight delta because they are based on the underlying asset’s volatility rather than its price.

Recommended Articles

This article has been a guide to what is Variance Swap. Here, we compare it with volatility swap and explain the topic in detail with its examples, and replication. You may also find some useful articles here –