What Are Equity Swaps?

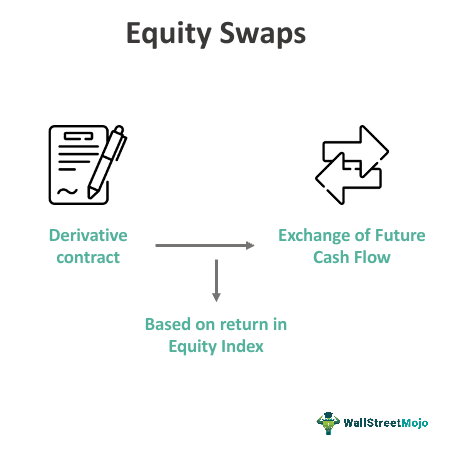

Equity Swaps is defined as a derivative contract between two parties that involve the exchange of future cash flows, with one cash stream (leg), determined on the basis of equity-based cash flow such as return on an equity index, while the other cash stream (leg) depends on fixed-income cash flow like LIBOR, Euribor, etc.

As with other swaps in finance, variables of an equity swap are notional principal, the frequency at which cash flows will be exchanged, and the duration/ tenor of the swap. It can also be used to hedge the equity risk in times of negative return environments and is also used by investors to invest in a wider range of securities.

Key Takeaways

- Equity swaps are derivative contracts involving the exchange of cash flows based on the performance of one or more underlying equities.

- In an equity swap, one party pays the equity’s total return (dividends and capital appreciation) while the other pays a fixed or floating rate.

- Equity swaps provide investors with exposure to the returns of equities without the need to directly own the underlying shares.

- Equity swaps are commonly used to hedge, manage portfolio risk, gain synthetic exposure to specific equities, or implement trading strategies.

Equity Swaps Explained

Equity swaps are a type of derivatives used in the financial market where cash flows are exchanged between the parties to the contract. The two parties agree that a set of cash flows will be exchanged in future which will depend on the performance of the equity market.

They are typically used for speculation, hedging of portfolio diversification and management. Among the two parties in the contract, one of them agree to get a fixed amount as payment over the entire life of the contract. The other party gets a return that is dependent on the equity index. The return may be due to dividend payment of capital gain. Thus, in this case the underlying asset is either a stock or equity index.

The swap rate, which is the amount that the party getting the fixed payment pays to the other, is predetermined when they agree. This rate does not change.

This is a good financial instrument that helps in hedging against loss in the equity market and is often used to speculate against the performance of the equity market in the future. The returns either act as gain when the market goes up of protects form loss when it goes down.

Thus, this financial instrument is very versatile in nature and can be very well customized as per the requirements of the parties and market conditions, investment goals and the risk tolerance levels.

Types

Thus, type of equity swaps trading can be in various forms. Let us try to understand them in detail.

- Total return swap – One party under this contract will get a total return in the form of capital gain or interest of dividend on the equity index, which is the underlying asset and will pay the other party in a fixed or floating rate.

- Price return swap – In this, the parties to the contract exchange the capital appreciation or depreciation of the index or equity. The settlement of the swap contract is done based on changes in the price of stock, excluding the dividend.

- Dividend swap – This is based only on dividends given out by the stock, which is the underlying asset. One of the parties agrees to take or pay this dividend that is used for income generation or hedging.

- Fixed interest rate – In this, one party agrees to pay a fixed interest rate and in exchange, gets a return on the equity.

- Floating interest rate – In this kind of contract, one party pays to the other on the basis of a floating interest rate and receives the returns on equity.

Pricing

The pricing and valuation of this type of derivative contract can be explained in the following manner.

During equity swaps pricing, the present value of all the future cash flows are settled against each other. The remaining amount is the price of the swap agreement. The original value of both cash flows is equal to zero. But once trading starts, they can either increase or decrease, depending on the underlying asset.

In this, the first leg represents the fixed payments made by the fixed receiver and the equity leg is the variable payment based on equity index performance.

Initially, the present value of all the future cash flows is determined by taking a discount factor based on risk-free rates. Then, the equity cash flows are determined, which include the dividend and capital gains, and along with that the fixed cash flows are also determined. Then comes the net cash flow calculation, where the fixed and the floating is netted against each other for each date of payment.

Various financial models related to equity swaps pricing are used in the above valuation, which makes it quite complex and accounts for volatility, dividends, and future expectations from the market. There are also some counterparty risks involved which should be considered in the valuation.

In this entire process, various forms of critical financial data are used, like equity prices, dividend rates, interest rates, etc; these data must be correct and updated. Otherwise, the pricing will be incorrect.

Example

Let us understand the concept of equity swaps trading with the help of a suitable example.

Consider two parties – Party A and Party B. The two parties enter into an equity swap. Party A agrees to pay Party B (LIBOR + 1%) on USD 1 million notional principal, and in exchange, Party B will pay Party A returns on the S&P index on USD 1 million notional principal. The cash flows will be exchanged every 180 days.

- Assume a LIBOR rate of 5% per annum in the above example and appreciation of the S&P index by 10% at the end of 180 days from the commencement of the swap contract.

- At the end of 180 days, Party A will pay USD 1,000,000 * (0.05 + 0.01) * 180 / 360 = USD 30,000 to Party B. Party B would pay Party A return of 10% on the S&P index i.e. 10% * USD 1,000,000 = USD 100,000.

- The two payments will be netted off, and in net, Party B would pay USD 100,000 – USD 30,000 = USD 70,000 to Party A. It should be noted that the notional principal is not exchanged in the above example and is only used to calculate cash flows at the exchange dates.

- Stock returns experience negative returns very frequently, and in case of negative equity returns, the equity return payer receives the negative equity return instead of paying the return to its counterparty.

In the above example, if the returns of stocks were negative, say -2% for the reference period, then Party B would receive USD 30,000 from Party A (LIBOR + 1% on notional) and in addition would receive 2% * USD 1,000,000 = USD 20,000 for the negative equity returns. This would make a total payment of USD 50,000 from Party A to Party B after 180 days from the start of an equity swap contract.

Settlement Process

The settlememnt process of this type of derivative contract can be in the below mentioned ways.

- Cash settlement – In this process, there is actual cash payment that take place between the parties as per the net difference in cash flows. However, there is no delivery if the underlying asset.

- Physical settlement – In this, the actual underlying asset is delivered by one equity swaps trader of the contract to the other during settlement.

Advantages

The following are advantages of equity swaps:

- Synthetic Exposure to Stock or Equity Index – Equity swaps can be used to gain exposure to stock or an equity index without actually owning the stock. Forex. If an investor who has an investment in bonds can enter into an equity swap to take temporary advantage of market movement without liquidating his bond portfolio and investing the bond proceeds in the equities or index fund.

- Avoiding Transaction Costs – An investor can avoid transaction costs of equities’ trade by entering into an equity swap and gaining exposure to stocks or equity index.

- Hedging Instrument – They can be used to hedge equity risk exposures. They can be used to forgo short-term negative returns of stocks without forging possession of the stocks. During the period of negative stock return, equity swaps trader can forgo the negative returns and also earn a positive return from the other leg of the swap (LIBOR, fixed rate of return, or some other reference rate).

- Access to a Wider Range of Securities – Equity swaps can allow investors exposure to a wider range of securities than that is generally unavailable to an investor. For example – by entering into an equity swap, an investor can gain exposure to overseas stocks or equity indices without actually investing in the overseas country and can avoid complex legal procedures and restrictions.

Disadvantages

The following are disadvantages of equity swaps:

- Like most of the other otc derivatives instruments, equity swaps are largely unregulated. Though new regulations are being formed by governments around the world to monitor the OTC derivatives market.

- Equity swaps, like any other derivatives contract, have termination/expiration dates. Thus, they don’t provide open-ended exposure to equities.

- Equity swaps are also exposed to credit risk, which doesn’t exist if an investor invests directly into stocks or equity index. There is always a risk that the counterparty may default on its payment obligation.

Equity swaps are used to exchange returns on a stock or equity index with some other cash flow (fixed rate of interest/ reference rates like labor/ or return on some other index or stock). It can be used to gain exposure to a stock or an index without actually possessing the stock.

Frequently Asked Questions (FAQs)

1. How does an equity swap differ from an equity forward or futures contract?

An equity swap is a financial contract between two parties to exchange future cash flows based on the performance of an underlying equity asset, whereas an equity forward or futures contract obligates the buyer to purchase the underlying asset at a predetermined price on a specified future date.

2. How are dividends handled in equity swaps?

Dividends in equity swaps are typically handled through adjustments in the cash flows exchanged between the parties. The party receiving the dividend payment may have their payment reduced, while the other party may receive an additional amount to compensate for the dividend.

3. What are the risks associated with equity swaps?

Risks associated with equity swaps include counterparty, market, liquidity, and operational risks. Counterparty risk arises from the potential default of the other party, while market risk refers to fluctuations in the underlying equity’s price. Liquidity risk can impact the ability to exit or enter positions, and operational risk pertains to administrative and processing issues.

Recommended Articles

This has been a guide to what are Equity Swaps. We explain them with example, pricing, settlement process, advantages and disadvantages. You can learn more about accounting from the following articles –