Volatility Swap Definition

A volatility swap is a forward contract where parties decide in advance to exchange cash flows based on the changes in the overall level of uncertainty or risk in the market. Through this volatility derivative, investors can make money by correctly anticipating and taking advantage of these swings in volatility.

Volatility is a measure of uncertainty and the risks involved. They are the easiest way to trade volatility. A volatility swap can trade spreads between implied volatility and realized volatility levels by speculating on future volatility levels. It can also hedge the volatility exposures of other businesses or positions.

- A volatility swap is a forward contract that provides exposure to pure volatility, making it a straightforward instrument to trade the up and down movements in asset or market prices.

- The amount paid at the contract’s expiration is calculated based on the implied and realized volatility differences in this swap.

- Traders who want to trade on the future index or stock volatility levels can use a swap to go short or long on realized volatility.

- These contracts offer pure exposure to volatility, making them the most straightforward way to trade volatility.

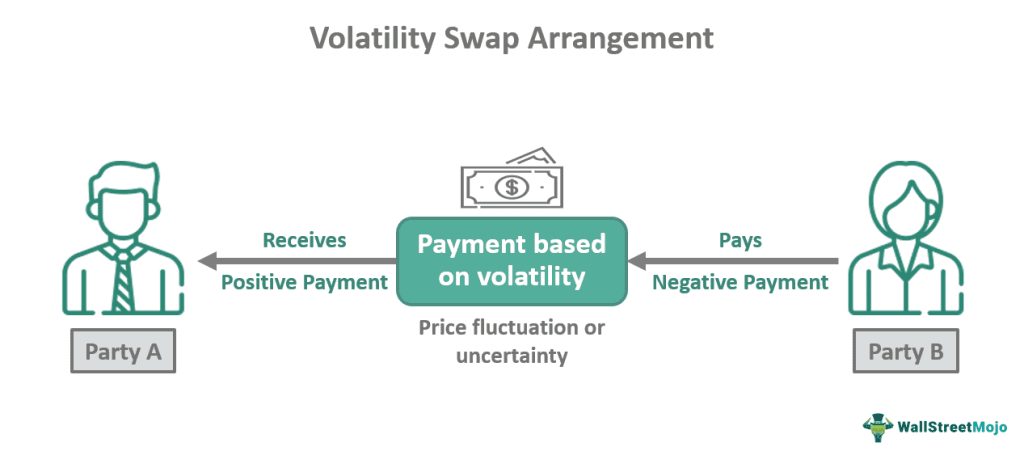

Volatility Swap Explained

Volatility swaps are forward contracts. In the swap, according to the contract, the buying party pays the selling party the difference between the realized volatility and the predetermined strike volatility of an underlying asset. It is also called realized volatility forward contracts based on annualized volatility.

These contracts provide pure exposure to volatility and become the most efficient way to trade the fluctuating movements of asset prices. The amount paid at the contract’s expiration is calculated based on the implied and realized volatility differences in this swap. It’s important to note that volatility measurement can vary and typically rise when uncertainty and risk increase.

Different variations include receiver volatility swaps and FX volatility swaps. In a receiver volatility swap, the buying party pays the selling party the difference between an underlying asset’s realized volatility and the predetermined strike volatility. These swaps are commonly used to hedge or speculate on downward movements in volatility.

On the other hand, an FX volatility swap focuses on the volatility of foreign exchange rates. It allows market participants to trade and manage exposure to fluctuations in currency volatility. It involves exchanging cash flows based on the specified currency pair’s realized or expected volatility levels.

Traders can use this volatility derivative to take positions on the future index or stock volatility levels, either going short (selling) or long (buying) on realized volatility. A long position in this swap receives annualized realized volatility as floating amounts, while a short position works oppositely. Traders can also take advantage of the spread between implied and realized volatility levels by unwinding the swap before expiration. These strategies can be beneficial during turbulent times and help navigate market downturns.

Examples

The following examples will help understand the concept even better.

Example #1

Let’s say, Dave, a trader, is engaged in a volatility swap with a notional amount of $2,000,000. He has taken a long position with a volatility strike of 20%. At the end of the contract, the realized volatility is estimated to be 30%. To calculate the volatility swap payoff, we can use the following formula.

Payoff = Notional Amount * (Realized Volatility – Volatility Strike)

Payoff = $2,000,000 * (0.30 – 0.20)

Simplifying the equation:

Payoff = $2,000,000 * 0.10 = $200,000

Therefore, Dave’s profit from the volatility swap is $200,000.

Example #2

Let’s take another hypothetical example. Daniel is another trader who invested in swaps. Recently elections were held in his country and much negative news spread. The political picture did not look good since the government was accused of corruption, embezzlement, etc. Given the weak stock markets and anticipated financial and political turmoil, Daniel takes a short volatility position. It means he expects the volatility levels to decrease or remain low during this period. Taking a short volatility position can be a suitable strategy in market unpredictability and uncertainty situations.

Advantages And Disadvantages

Let us have a look at the benefits and limitations of volatility swaps below:

| Advantages | Disadvantages |

|---|---|

| It provides a straightforward way to trade volatility, allowing investors to profit from price fluctuations without owning the underlying asset. | Valuing this swap requires an accurate estimation of future volatility levels, which can be challenging due to the unpredictable nature of markets. |

| Traders can tailor their risk exposure by taking long or short positions on realized volatility, enabling them to hedge existing positions or speculate on future market movements. | As with any derivative contract, it carries counterparty risk. If the counterparty defaults or fails to fulfill its obligations, it can lead to financial losses for the investor. |

| It can generate returns in rising and falling markets, making them versatile instruments that can be utilized in different market environments. | These swaps may face liquidity issues, especially for less liquid underlying assets or in times of market stress, which can impact the ease of entering or exiting positions. |

| Including it in a portfolio can benefit diversification and serve as a risk management tool by offsetting potential losses during market downturns. | Accessibility may be limited to confident investors, requiring access to specialized markets or platforms, potentially excluding retail investors. |

Volatility Swap Vs Variance Swap

Volatility and Variance Swaps are different financial instruments that expose investors to volatility. While they both relate to volatility, the two have essential differences.

| Key points | Variance Swap | Variance Swap |

|---|---|---|

| Concept | A variance swap is a forward contract. The arrangement is based on the difference between a predetermined variance delivery price and the realized variance in the desired period. | These are contracts that are based on volatility. |

| Essence | The variance swap is annualized on variance, the square of the volatility realized. | It is the annualized standard deviation of a stock’s returns. |

| Settlement | At settlement time, the realized variance during the period is calculated, and the difference is then multiplied by the contract notional for estimation. | The amount is settled at maturity after estimating the differences between realized volatility and the strike. |

Frequently Asked Questions (FAQs)

1.How to price volatility swap?

Here is how the price is calculated. The notional value is multiplied by the difference in value between the actual volatility and the estimated volatility (volatility strike). Then, it is represented by the formula: volatility swap payoff = notional amount *(volatility-volatility strike).

2.What is the payoff of a volatility swap?

The amount to be received at the settlement involves realized volatility and implied volatility. The difference between these two values is crucial to executing this volatility derivative. A payoff happens when the values of realized volatility and volatility strike differ.

3.Is VIX a volatility swap?

No, the VIX (Volatility Index) is not a volatility swap. Instead, the VIX measures the market’s expectation of future volatility, specifically for the S&P 500 index options over the next 30 days. While both are related to measuring or trading volatility, they are distinct financial instruments with different purposes, methodologies, and underlying assets.

Recommended Articles

This has been a guide to what is Volatility Swap. Here, we explain it with its differences with Variance Swap, examples, advantages and disadvantages. You can learn more about it from the following articles –