What is a Liquidating Dividend?

A liquidating dividend refers to residual payment in cash or other assets to the shareholders after reducing all the creditors and lender’s obligations when the business closes entirely. They are often paid to the shareholders when they believe the business is no longer concerned. I.e., the business is not in a position to survive due to external or internal factors for which management is about to liquidate the business. This is the reason it is also known as liquidating distribution.

Explanation

When a company decides to dissolve the business, it is an indication that the company is about to liquidate its assets. It means the business sells the inventory and every asset, including the building and machinery it owns. The only objective of liquidating the assets is to pay off the debt obligations to the secured and unsecured creditors. Finally, the company distributes the residual amount to the shareholders as liquidating dividends.

In the United States, it is a regulatory requirement for the company to pay liquidating dividends. A company could shell out such dividends to the shareholders in one or more installments. They refer to Form 1099 Div with required detail as size and form of payment.

When the shareholder receives it, the amount paid is reported in form 1099 – DIV. The extent of the amount which exceeds the shareholder’s basis is the capital, taxed as capital gain in the hands of shareholders. The tax on capital gain is short-term or long-term, depending on the duration for which the shareholders hold the same. Capital gain is long-term if held for more than a year. Capital gain is short-term if held for less than one year. If shareholders have bought shares in different periods, then the dividend divides into short term or long term. It happens according to the group of shares concerning their date of purchase.

Example

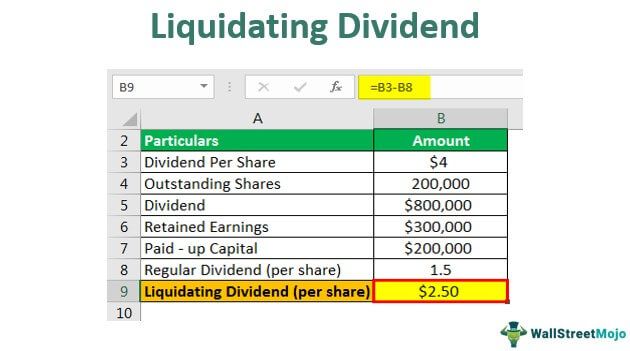

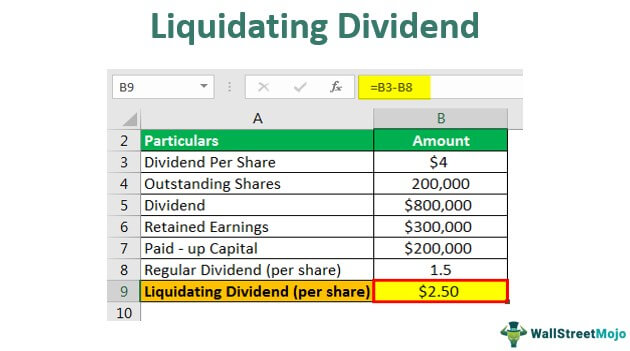

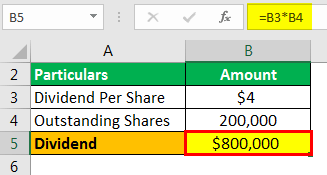

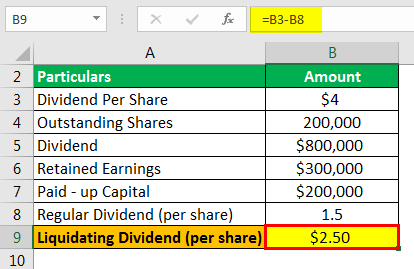

To illustrate liquidating dividends, let’s assume that on 1st March 2018, company X declared $4 as a dividend per share. The company’s outstanding shares are 200,000. In addition, the retained earnings are $300,000.00 and paid-up the capital base of $2,000,000.

Solution –

The Dividend is calculated as follows-

- = $4.00 * 200,000

- = $800,000 shares

The total dividend calculated is $800,000. To pay this dividend, company X will use first the balance in retained earnings of $300,000.00, and the rest of the dividend ($800,000 – $300,000) = $500,000 will be absorbed from the company’s capital base.

Let’s explain the effect of the dividend payment from a shareholder’s perspective. Assume shareholder Y owns 1,000 shares and is expected to receive a dividend payment of $4,000 (1,000 *$4).

The amount of dividend being represented from the regular dividend is calculated as follows:

- =$300,000 retained earnings/ 200,000 outstanding shares

- =$1.50 per share

The liquidating dividend of the total dividend is calculated as follows:

- =$4.00 – $1.50

- = $2.50 per share

Liquidating Dividend vs. Liquidating Preference

When a company or business decides to liquidate dividends, the business is supposed to clarify the order and the form in which the shareholders would receive the dividends. The payment is made according to the preferential order. The companies would decide to liquidate the business when it is not in a position to clear the legal obligations or it becomes insolvent and about to face bankruptcy. As the business is liquidating, the residual assets would flow to the shareholders and creditors.

Secured creditors are the ones who will receive payments in priority over others, followed by unsecured creditors, bondholders, the government for unpaid taxes, and employees in case there are pending salaries and wages. Preferred shareholders and equity stockholders will receive the residual assets if any.

Liquidating Dividend and Ordinary Dividend

The liquidating dividend is paid from the company’s capital base to the shareholders based on their respective invested capital. It differs from an ordinary dividend, which is paid to the shareholders only when the business is doing well and is paid from current profit or retained earnings.

Its return on capital is exempted from tax, and therefore it is not taxable for the shareholders.

It is being made to fully or partially liquidate the business. It is not considered income by an investor as far as accounting treatment is concerned; instead, they are recognized as a reduction in carrying the value of the investment. The ex-dividend date is usually fixed for two business days before the record date because of the T+3 system of settlement in It is being made with the intention of fully or partially liquidating the business. It is not considered as income by an investor as far as accounting treatment is concerned; instead, they are recognized as a reduction in carrying the value of the investment. Any person who owns the common stock on the ex-dividend date is supposed to receive the distribution irrespective of who currently holds the security. The ex-dividend date is usually fixed for 2 business days before the record date because of the T+3 system of settlement in financial markets being used in the United States. Any person who owns the common stock on the ex-dividend date is supposed to receive the distribution irrespective of who currently holds the security.

In the case of ordinary dividends, the board of directors declares the dividend on a particular date, termed declarations data. The same is received by the owners on the payment date when officials mail the check and credit the investor’s account with the distribution amount.

In the context of dividends, it is required to distinguish between liquidating dividends and ordinary dividends because both follow different accounting treatments per regulatory requirements. In the case of traditional dividends, they are recorded as income from investments. In contrast, liquidating dividends are not recorded as income. Still, as the reduction in carrying value of investment or, in other words, they are recorded as a return on the investment. The liquidating dividend is necessarily envisaged as repayment of invested capital and is made from a capital base; therefore, the tax requirement also differs between the traditional dividend and liquidating dividend.

Conclusion

The retained earnings (accumulated profits) are deducted from the total dividend. Then this amount is supposed to be divided by the total number of outstanding shares to get the conventional dividend. Once this dividend is paid out, the remaining balance is what we call liquidating dividends.

In our example, shareholder Y would receive a regular dividend of $1,500 ($1.5*1000) and liquidating dividend of $2,500. It is a return on a shareholder’s investment; therefore, they are not taxable in the hands of shareholders when they receive the same.

Recommended Articles

This article has been a guide to Liquidating Dividend. Here we discuss how liquidating dividends work, examples, and the differences between preference and ordinary dividends. You can learn more about finance from the following articles –