What Is Final Dividend?

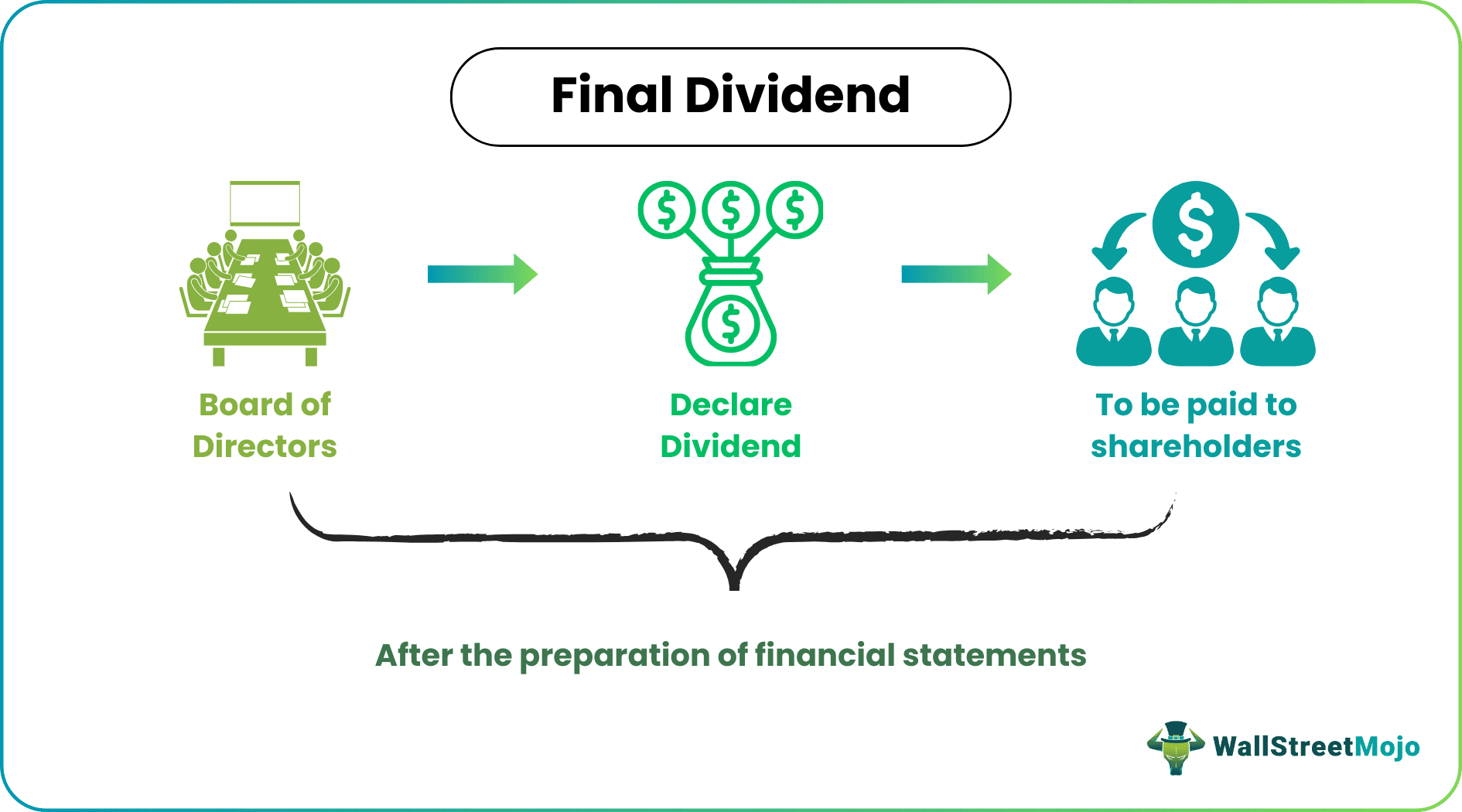

The final dividend is the amount declared by the board of directors to be payable as a dividend to the company’s shareholders after the company’s financial statements are prepared and issued for the relevant financial year and is commonly announced in the annual general meeting of the company.

The dividend is the return the Company provides to the shareholders from the profits earned during the financial year. The Company may announce a dividend during the part of the year called the interim dividend, or it may announce the dividend at the end of the year once it has ascertained the profits and financial position.

Final Dividend Explained

The Final Dividend is the dividend announced by the Company after preparing the final accounts. It is usually announced during the Annual General Meeting of the Company. After the annual accounts have been prepared, the final dividend calculation declaration of the dividend is called the final or year-end dividend. Year-end dividends are paid yearly and are generally higher than interim dividends given by the Company.

- The final Dividend is generally more significant than the interim dividend. It is because the Company tends to be a little conservative during the financial year until it gets the annual accounts, i.e., revenues and expenditures for the year.

- After the Company knows its profits for the financial year, it chooses to retain some portion for future business needs. At the same time, the remaining is distributed amongst the shareholders as the final dividend.

Thus, it is a very important and effective method in which the companies are able to distribute their profits to the shareholders or investors. This provides them a return on their investments and improves the credibility of the organization.

It also indicates that the business is performing well and stable in terms of finances, since they can afford to pay consistent dividends. This acts as a positive signal to the investors who will be willing to put their money in these companies with the hope that the company has good future prospects regarding growth and expansion.

How To Calculate?

The calculation of such dividend as per the dividend policy of a business, involves a few steps as mentioned below. Let us go through them.

The first step in final dividend calculation is to calculate and identify the amount of retained earnings. This information can be obtained from the current income statement, balance sheet and the statement of retained earnings of the company, which is a part of the annual report of the business. Now it is necessary to find out the retained earnings balance at the beginning of the financial year.

Next comes the step where the net profit or the net income has to be identified properly for further calculation.

The next step is to verify whether the business has any contractual obligation from loan agreements or anything similar, where they are required to maintain a minimum level of retained earning balance so that the loan or any similar financial obligation can be met on time. Failure to follow such rules may result in restrictions in dividend payment or legal consequence.

The management must clearly understand the dividend policy and the percentage of income that can be given to shareholders under the final dividend resolution. Some companies have it fixed, while others may have a variable policy, depending on the company’s performance.

Next comes the allocation, where the dividend will be allocated as a percentage of the net profit during final dividend accounting treatment. The remaining amount will remain in the business to be used for other financial obligations, meeting any sudden need or investment purpose.

Then the final amount will be calculated after subtracting any interim dividend paid to shareholders from the total allocated dividend amount. This amount will be distributed at the end of the fiscal year.

The final step is the announcement of the decision and final dividend date in the Annual General Meeting of the company. It will be proposed by the Board of Directors and approved by shareholders through vote. However, the company may pay it in the form of either cash or additional shares, which will again depend on the policy the business follows.

Example

Let us understand the concept of final dividend resolution with the help of a suitable example.

An investor holds 100 shares of a Company ABC, which has announced a final dividend of $ 3.5. The investor will receive $ 350 as the year-end dividend on his investment.

Now, the Company has doubled the dividend for the next year, i.e., it is paying $ 7 per share. Thus, the investor will receive $ 700 as the year-end dividend on his 100 shares held in the Company.

The above example gives a basic idea about the final dividend calculation method. However, there are may important steps in the process, which are already elaborated in the section above.

Final Dividend Video Explanation

Key Points

Some key points to note during determination and calculation of this kind of dividend are given below.

- The Board of the Company decides it and should be aligned with the Company’s dividend policy.

- It is usually a cash dividend and not astock dividend. However, the Company may choose to pay cash and stock dividend or only stock dividend.

- It is announced by the Board and voted by the shareholders during the Annual General Meeting of the Company.

- Approval of such a dividend is considered an ordinary shareholder resolution and an ordinary business.

- It is announced after the company’s financial statements are approved and its financial position and profits are ascertained.

- Once approved, this dividend is the Company’s obligation, and the payment decision cannot be reversed.

- These dividend payments do not require a special provision in the company’s articles of association.

- It is not binding on the Company to announce the final dividend. Although dividend policy may include some fixed payment each year, this dividend is announced along with the final dividend date on the will of the Board of the Company after reviewing the financial position.

- If the Company has not made any profits in a financial year, it may choose not to pay any dividends, or some dividends may be paid out of the free reserves. The government laws on such payment from free reserves for loss-making Companies may differ from country to country.

Thus, it is necessary to follow the above rules and policies of final dividend accounting treatment diligently so that there is no discrepancy or legal consequence regarding the dividend given out to shareholders. The management should be aware of these points to conduct the process smoothly.

Final Dividend Vs Interim Dividend

Although final and interim dividends are paid to the investors as a return on their investment, they have some key differences. So let us look at the differences between the final vs. interim dividend.

- The interim dividend is announced and paid in the middle of the financial year. In contrast, the final dividend is paid after the completion of the financial year.

- The interim dividend is declared before the finalization of the accounts. In comparison, the final dividend is paid after the finalization of the accounts.

- An interim dividend can be canceled with the shareholder’s consent. Still, the year-end dividend, once approved, cannot be canceled, and it becomes an obligation of the Company to pay a year-end dividend.

- The interim dividend is usually lesser than the year-end dividend.

- An interim dividend requires a provision in the Company’s articles of association; however, no such provision is necessary for a year-end dividend.

Final dividends are also called year-end dividends. The term “final” should not be confused with the final dividend paid by the Company, and it ceases to exist. Such a dividend is called a liquidating dividend. A liquidating dividend is a type of payment made by the Company when it closes its operations and pays the shareholders any amount/capital available after selling off the assets and settling its debts/other liabilities. The liquidating dividends are paid from the company’s capital base, whereas the year-end dividend is paid from the profits earned from the operations.

Recommended Articles

This article has been a guide to what is Final Dividend. We explain its differences with interim dividend and how to calculate along with example, and key points. You can learn more about Shareholder’s Equity from the following articles –