Part of our Statistical Concepts guide

What Is An Eigenvector?

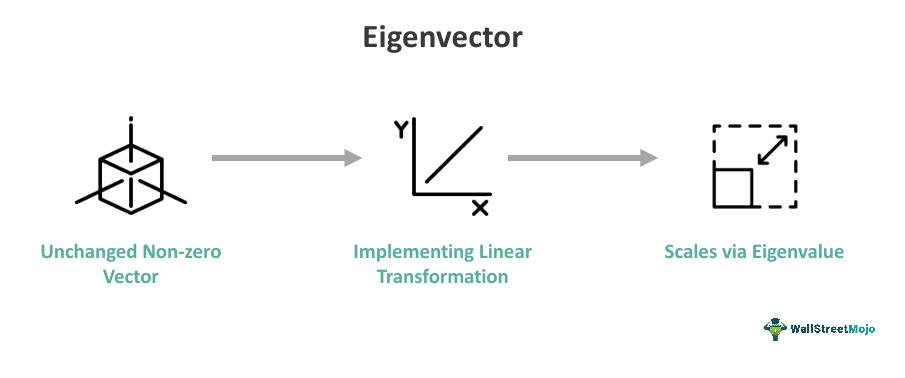

An eigenvector is a concept from linear algebra that depicts a non-zero vector that remains unchanged in direction when a linear transformation is implemented to it, only scaling via a scalar element called the eigenvalue. Eigenvectors play a critical position in portfolio management and risk control.

In finance, such matrices often represent the covariance shape of asset returns. Eigenvectors of those covariance matrices are related to fundamental additives, which constitute the guidelines of variance within the data. By analyzing the eigenvectors and eigenvalues of a covariance matrix, economic analysts can perceive key chance elements in a portfolio. In short, this helps them understand how distinct belongings contribute to standard chance.

Key Takeaways

- Eigenvectors are non-zero vectors that continue to be unchanged in course, subject to a linear transformation, effectively scaling by means of a scalar factor known as the eigenvalue.

- These are derived by means of fixing the system of equations (A – λI)v = zero. Here, A is a matrix, λ is the eigenvalue, I is the identification matrix, and v is the eigenvector.

- Associated with each eigenvector is an eigenvalue, which quantifies the scaling element of the eigenvector during a linear transformation.

- In finance, these are helpful for hazard evaluation, portfolio diversification, and knowledge of the primary components of hazard in a portfolio.

- It assists in perceiving assets that make contributions to portfolio chance, enabling the construction of properly assorted portfolios that efficaciously seize hazard elements.

Eigenvector Explained

An eigenvector is a fundamental idea in linear algebra, depicting a selected path within a vector area. When a linear transformation is implemented to a vector, the converted vector can also trade in each route and significance. They are mathematical tools that help to research the underlying shape and relationships within a set of economic belongings. These vectors are a result of the covariance matrix, a statistical measure that quantifies the diploma to which distinctive assets in a portfolio move together. The idea of eigenvectors came from linear algebra, in particular matrix evaluation, and was adapted for monetary packages to advantage insights into portfolio diversification and change control.

It helps pick out the dominant patterns of co-movements among properties in a portfolio. By inspecting those vectors, buyers can figure out the essential additives of threat and return. Each eigenvector corresponds to a unique danger factor, and the associated eigenvalues quantify the importance of everything.

Through eigenvector evaluation, financial professionals can assemble portfolios that effectively capture the essential sources of chance and return, facilitating effective asset allocation. This technique, rooted in mathematical principles, enhances the understanding of complex financial relationships and supports the development of strategies that stabilize hazards and praise them in investment portfolios.

Properties

Eigenvectors own many properties that lead them to be essential in numerous mathematical and implemented contexts:

- Direction Preservation: They retain their path while subjected to a linear transformation, effective scaling by using a scalar element known as the eigenvalue. This property is essential in the knowledge of the dominant directions of variants in datasets or matrices.

- Orthogonality: They are similar to awesome eigenvalues of a symmetric matrix are orthogonal. Thus, this orthogonality belonging is helpful for dimensionality reduction in applications like Principal Component Analysis (PCA).

- Eigenvalue Dependence: Eigenvectors with identical eigenvalues are linear. They span a subspace, representing particular directions within that subspace.

- Normalization: They often normalize to unit duration, facilitating interpretation. The lengths of the eigenvectors constitute the relative significance of the corresponding eigenvalues in shooting variance or danger.

- Factor Decomposition: In thing models, eigenvectors assist in decomposing a matrix into fundamental elements, assisting in the identification and quantification of commonplace assets of variation.

- Principal Components: Eigenvectors are the idea for essential additives in PCA, enabling the illustration of high-dimensional information in phrases of the excellent instructions of variance.

- Application in Systems of Linear Equations: They are usually applicable to diagonalize matrices, simplifying the answer of structures of linear equations, which has programs in physics, engineering, and different fields.

How To Find?

Finding eigenvectors includes a chain of mathematical steps implemented to the covariance matrix of asset returns. Below is a brief:

- Covariance Matrix: One can begin with the covariance matrix, which captures the pairwise relationships among unique belongings in a portfolio. This matrix is symmetric and wonderful semi-specific.

- Eigenvalues and Eigenvectors: Then solve the characteristic equation det(C – λI) = 0, in which C is the covariance matrix, λ represents the eigenvalue, and I is the identification matrix. This equation yields the eigenvalues, which quantify the amount of variance associated with each eigenvector.

- Principal Component Analysis (PCA): Eigenvectors are a result of the predominant components of the covariance matrix. These additives are the normalized eigenvectors similar to the eigenvalues received in the preceding step.

- Normalization: Now, normalize the eigenvectors to unit duration. This step guarantees that every eigenvector represents a direction in the portfolio space, and their lengths indicate the proportion of total portfolio variance they account for.

- Interpretation: Each eigenvector corresponds to a unique threat issue or significant issue. Therefore, analyzing those vectors permits traders to recognize how one-of-a-kind assets make contributions to usual portfolio risk and become aware of opportunities for diversification.

Examples

Let us explore it better with the help of examples:

Example #1

Assume a portfolio inclusive of three imaginary stocks: A, B, and C. By calculating the covariance matrix in their ancient returns, we find eigenvalues and eigenvectors. Let’s say the primary eigenvector, related to the critical eigenvalue, reveals a not-unusual marketplace aspect affecting all stocks. This implies a systemic chance shared through A, B, and C.

The second eigenvector would possibly represent a unique risk element particular to Stock A, indicating an idiosyncratic hazard that does not affect the whole market. The 0.33 eigenvector can also highlight a correlation among Stocks B and C, indicating a zone-particular risk.

Here, eigenvectors help dissect the portfolio’s risk shape. Thus, the first eigenvector shows market hazard, the second highlights stock-unique risk for A, and the 0.33 identifies a quarter-precise correlation between B and C, providing insights for higher danger management and diversification techniques.

Example #2

In a 2023 article by Yahoo Finance Canada, concerns had been raised about the absence of transparency and accuracy in tax checks in Ontario. The article highlights the opacity surrounding the assessment method, emphasizing capability inaccuracies that could impact owners’ tax burdens.

The article indicates that the present-day device might want to effectively mirror the real marketplace values of homes, mainly due to disparities in tax checks. Critics argue that a more transparent and precise approach, possibly incorporating superior analytical gear like eigenvectors, may want to deal with these problems. This is because Eigenvectors, extensively used in monetary analysis, could offer an advanced method for evaluating the complicated relationships and elements influencing belonging values, doubtlessly leading to a fairer and extra dependable tax evaluation device in Ontario.

Applications In Finance

Eigenvectors have diverse applications in finance, contributing to more profound know-how of portfolio dynamics, threat control, and efficient asset allocation:

- Risk Decomposition: It helps in breaking down the overall chance of a portfolio into specific factors or predominant components. This permits buyers to become aware of and manage various assets of chance, improving the danger-return profile in their portfolios.

- Portfolio Diversification: By reading eigenvectors, investors can discover belongings that contribute to portfolio hazards and those that provide diversification blessings. Thus, this record aids in constructing nicely varied portfolios that limit exposure to specific chance factors.

- Factor Models: They play a pivotal position in issue fashions, assisting in picking out and quantifying common danger elements that pressure asset returns. In other words, factor analysis based on eigenvectors enhances the modeling of complicated financial relationships.

- Efficient Frontier Construction: It is instrumental in building efficient frontiers, illustrating the surest alternate-off between threat and return. In addition, this helps the layout of portfolios that maximize returns for a given level of threat or minimize risk for a centered level of go-back.

- Correlation Analysis: It provides insights into the correlation shape among belongings. Understanding these relationships allows traders to navigate market trends and make informed selections on asset allocation.

Difference Between Eigenvalue And Eigenvector

Following is a depiction of the essential variations between eigenvalues and eigenvectors:

Frequently Asked Questions (FAQs)

Can eigenvectors be negative?

Eigenvectors cannot have positive or negative values by themselves. They serve as guidelines in the spatial domain. The scaling factor for the corresponding eigenvector at some point in a linear transformation indicates the eigenvalues associated with eigenvectors, which can be harmful, zero, or high-quality.

How are eigenvectors applicable in Principal Component Analysis (PCA)?

In Principal Component Analysis (PCA), eigenvectors are essential. PCA uses the covariance matrix’s eigenvectors to identify the critical elements of the orthogonal guidelines that account for the majority of the variance in the data. In finance, this approach is often for chance assessment and dimensionality discounting.

Are eigenvectors unique for a matrix?

No, they are not unique to a matrix; a matrix can have multiple linearly independent eigenvectors corresponding to the same eigenvalue. However, the set of all eigenvectors associated with a specific eigenvalue forms a subspace.

Recommended Articles

This article has been a guide to what is Eigenvector. Here, we explain how to find it, its examples, properties, comparison with eigenvalue, and applications. You may also find some useful articles here –