Part of our Mergers & Acquisitions guide

What is Hostile Takeover?

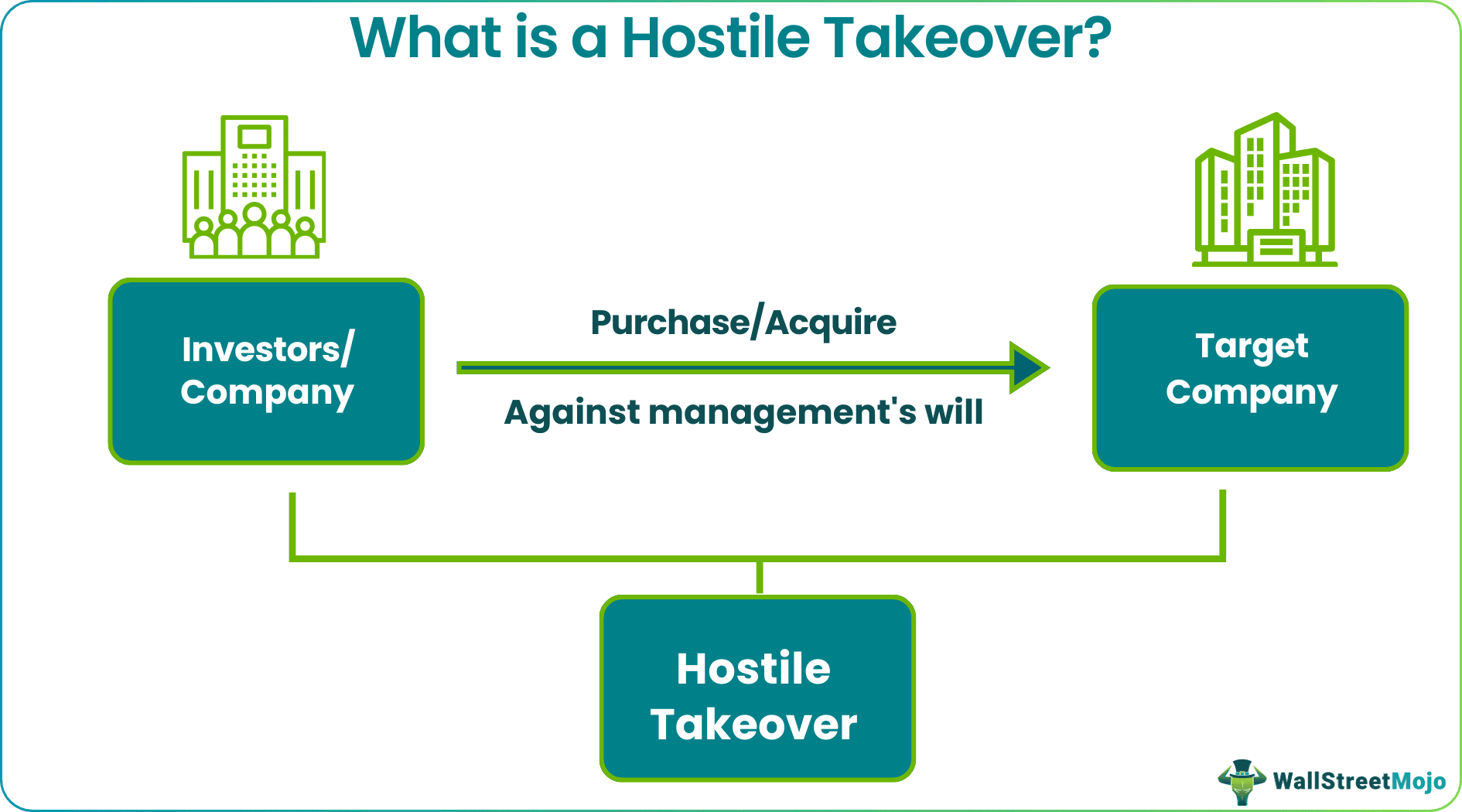

A hostile takeover is a process where a company acquires another company against the will of its management. The company that undergoes acquisition is known as an acquiring company or acquirer, while the one that is acquired is referred to as a target company. It is different from friendly takeovers where the target company is willing to sell itself.

A hostile takeover is done when the acquirer feels the targeted company is performing poorly or undervalued for one or another reason. The acquirer either purchases the company as a whole or chooses to buy major stocks to gain ownership of it.

- A hostile takeover refers to the acquisition process where a company purchases a target company without the latter’s management approval.

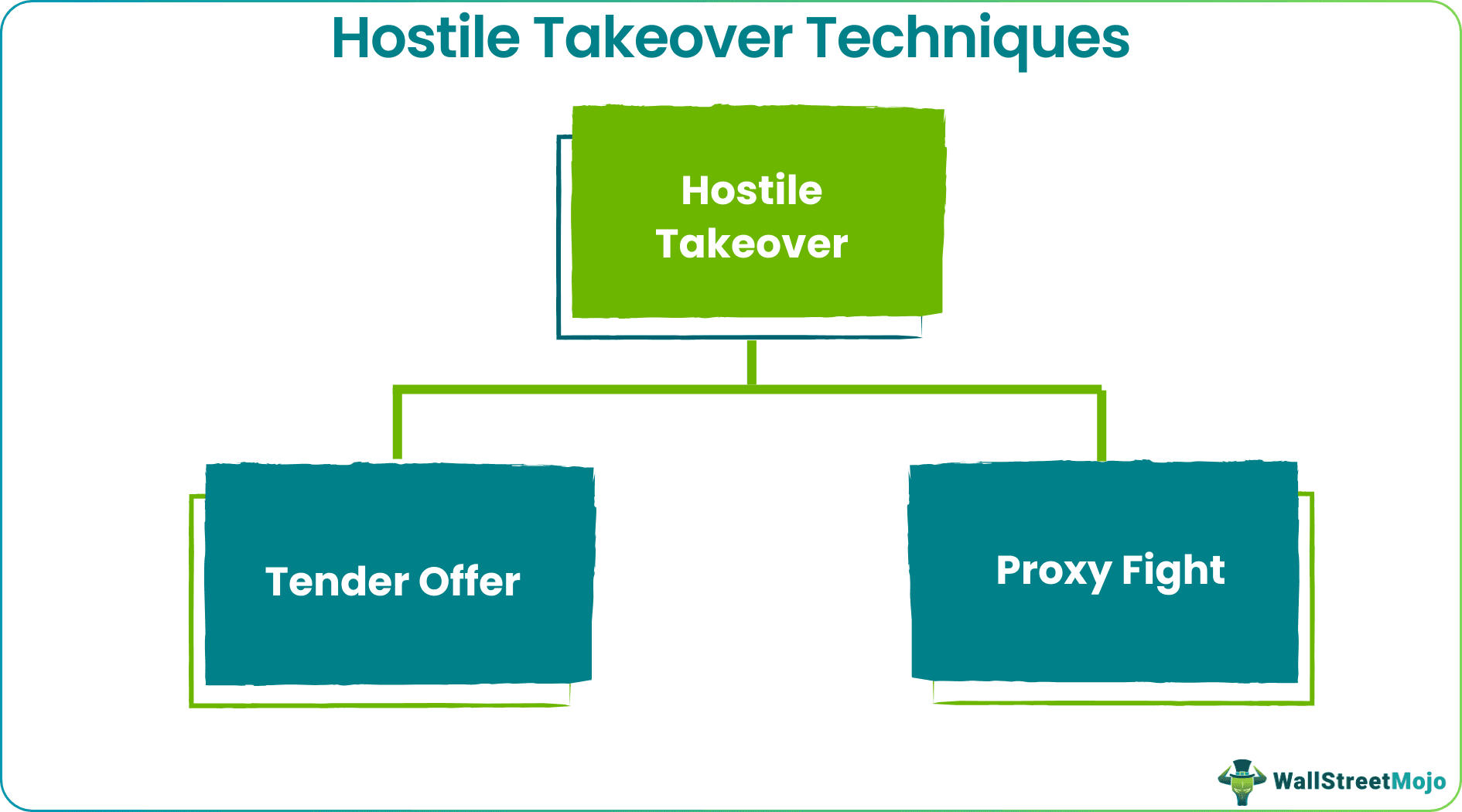

- The tender offer and proxy fight are the two tactics businesses apply to achieve their non-friendly takeover objective.

- The target company tries its best to fight back the takeover attempts if the management is unwilling to sell its venture.

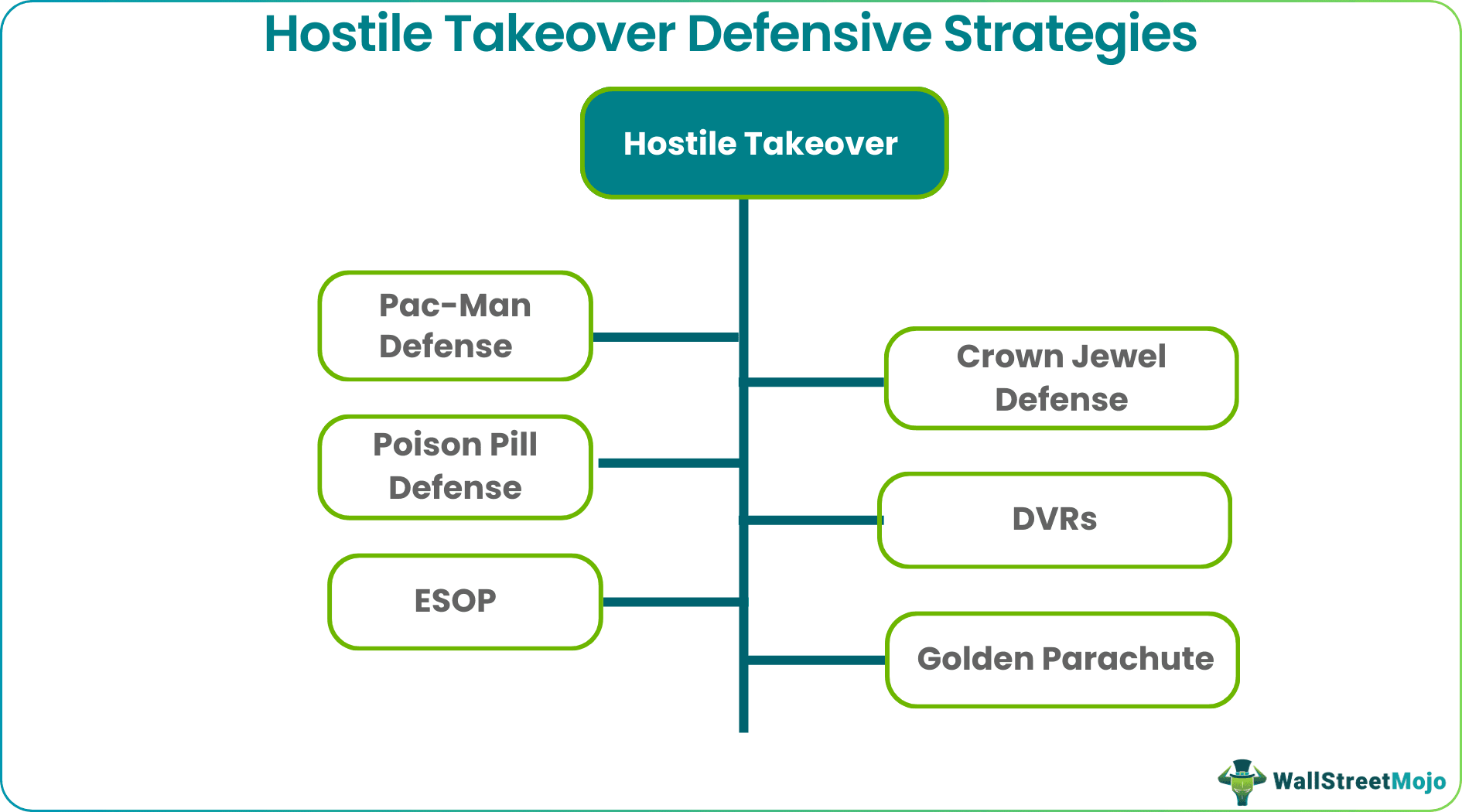

- The common defensive strategies adopted and implemented include Pac-Man, crown jewel, poison pill, golden parachute, employee stock ownership program, and differential voting rights.

How does Hostile Takeover Work?

A hostile takeover in business marks the fight against the company that is unwilling to be sold and another company that has already decided and is firm enough to purchase it.

The acquiring company has nothing to do with the approval of the target company’s management. As it revolves around who will win, both sides try their best to achieve their objective. In their attempt to acquire and not be acquired, respectively, the companies put in multiple offensive and defensive strategies as applicable.

Hostile Takeover Explained in Video

Offensive Strategies

It is vital to explore the hostile takeover strategies businesses use to properly understand hostile takeover meaning and process. Such takeovers run on various strategies. The two most widely observed being used in the corporate world are – tender offers and proxy fights.

1. Tender Offer

The acquisition happens through a tender offer when a group of investors wishes to buy the target company’s majority of shares at a premium price. This premium price is higher than the market price. The offer is presented to the board of directors, who may or may not accept it. As a result, the investors or interested acquirers make the offer directly to shareholders who agree to proceed with the deal given the individual benefits they tend to make. As soon as they agree, the shares are sold, leading to hostile takeovers.

2. Proxy Fight

Another acquisition strategy that most interested acquiring companies adopt and use is proxy fight. As the name implies, this strategy is a firmer approach towards acquisition. An acquirer attempts to convince the existing shareholders to withdraw support for the existing management of the target company. It makes a hostile takeover in business much easier. The only objective is to remove the members in the management who oppose the takeover.

Defensive Strategies

In the process, acquirers leave no stones unturned to take over the company. On the other hand, the target companies try resisting a hostile takeover to the utmost possible extent. There are multiple strategies that target companies utilize to make sure they are not taken over by businesses they don’t wish to.

1. Pac-Man Defense

In this technique, the target company can counter the acquiring company by buying the stocks of the latter. It paves the former’s path to take over the latter, instead. The Pac-Man Defense trick is the best when two companies of similar size participate in such takeovers. Moreover, it is one of the most effective strategies to implement, provided the target company has enough resources to support its decision.

2. Crown Jewel Defense

Under the Crown Jewel Defense strategy, the target companies sell their most valuable assets to make themselves look like an unattractive deal to interested acquirers. They normally go for a friendly third-party business to buy those assets from them as soon as the interested acquiring companies drop their bids. The target companies tend to lose their reputation in the process, and hence, it is often considered a high-risk strategy.

3. Poison Pill Defense

The poison pill defense strategy is used by target companies most widely. Their objective is to make takeovers so expensive that interested acquirers drop their purchasing plan. As a result, they start selling their shares at a discounted price, making the discount inaccessible to prospective acquiring companies. This, in turn, makes it difficult for the interested buyers to bear the increasing share prices, and, therefore, they do not proceed with the takeover.

4. Differential Voting Rights (DVRs)

The target companies put Differential Voting Rights (DVRs) in place. It gives shareholders limited voting rights, while the management has the final say. This way, the companies ensure that even if shareholders turn against the management, no non-friendly takeover can occur.

5. Employee Stock Ownership Program (ESOP)

Under the ESOP tactic, the management grants a significant interest in the company. This ensures that they would never go against them to support any unwilling takeover.

6. Golden Parachute

Golden Parachute is the next defensive strategy that aligns the target company and its top management via a contract. Under this agreement, the former promises to offer those management executives considerable benefits, like bonuses, stock options, medical benefits, etc., even if it terminates them given the company restructuring procedure. As a result, the top-level executives too become loyal to the company and never think of supporting an acquirer interested in an unwilling takeover.

Hostile Takeover Examples

Let us consider the following hostile takeover example for a better understanding of the concept:

Example #1

Company X approaches Company A for takeover, but the target company’s management doesn’t agree to the proposal. Therefore, X applies some offensive tactics to fulfill its desire.

First, it connects with the target company’s shareholders and asks for their proxy vote against the management. As a result, the shareholders, who never received the expected importance in the company, trusted the acquiring party and voted out the existing management. Thus, company X takes over company A conveniently.

Example #2

Recently, Kohl’s accepted how the recent takeover offers have adversely affected the business’s image lately. This confession came following the Starboard Value-backed Acacia Research’s offer to buy Kohl’s share at $64 per head, following private equity venture Sycamore Partners allegedly offering $65 per share for Kohl’s.

Given the constant non-friendly takeover offers, the department store has decided to implement a shareholder rights plan under the Poison Pill policy to avert all such offers with immediate effect from February 4, 2022, to expire in February 2023.

Hostile Takeovers vs Friendly Takeovers

As the names imply, friendly takeovers proceed with the management’s will, while a hostile takeover is the opposite. It means the acquirers can take over a target company even if the latter’s management doesn’t approve it.

The interested buyers prefer friendly takeovers where the management, shareholders, employees, and associated individuals willingly sell the company. However, some acquirers are rigid enough to buy the targeted firm, and they do whatever they can to achieve their objectives.

This is when they implement hostile takeover strategies in business, preparing themselves for a fightback from the target company in the form of their unique defensive strategy.

Frequently Asked Questions (FAQs)

What are hostile takeovers?

A hostile takeover occurs when an acquisition happens without the approval or will of the target company’s management. It results from the rigid wishes of the acquirers who are not ready to give up on their desire to acquire a particular firm. The two most important takeover strategies that businesses use to accomplish the objective are tender offers and proxy fights.

Are hostile takeovers legal?

Yes, it is completely a legal affair. Though the process doesn’t involve any management approval, it is still considered ethical as some target companies do not consider being bought despite performing poorly in the market. In addition, it gives another chance to a company to flourish, and hence, it is appreciated.

What are the benefits of hostile takeovers?

Here are the benefits of a hostile takeover for both the target companies and acquiring firms:

– Improve stock prices

– Increase revenue

– Enhance efficiency

– Show overall growth in performance

Recommended Articles

This article has been a guide to hostile takeover meaning & operation. Here we explore the offensive & defensive hostile takeover strategies along with examples. You may also look at the following articles on Investment Banking to enhance your knowledge further.