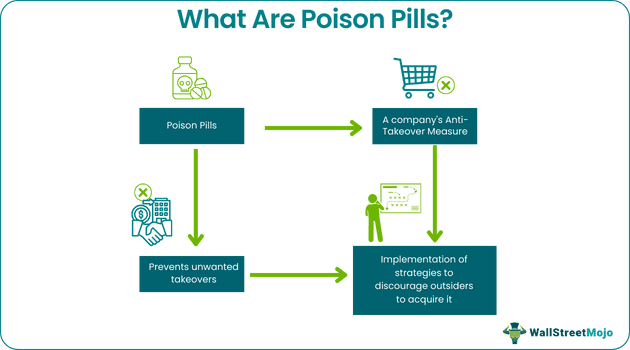

Poison Pills Definition

Poison pills refer to adefensive technique where the company tries implementing strategies that would prevent it from getting acquired by an external member. In the process, the board of directors decide to offer outstanding shares to existing shareholders at a discounted price so that no outsider buys the same and gains control over it.

Also known as the shareholder’s rights plan, this method is useful for minority shareholders as it protects them from an unprecedented takeover or a hostile management change. In short, poison pills in finance and business are tactics that prevent acquisitions by unwanted entities.

- The poison pill is a psychology-based defense method. In this approach, minority shareholders are guarded against an unpredictable takeover or a hostile management change utilizing methods to escalate the acquisition cost and create discouragement.

- It can be carried in two ways: make an acquisition a tough nut to crack or have harmful side effects that unfold in different stages. Common poison pills are preferred stock plans, FLIP-IN, FLIP-OVER, back-end rights plans, golden handcuffs, and voting plans.

- Netflix, GAIN Capital, Micron Tech, and Pier 1 Imports are examples of poison pills.

How Do Poison Pills Work?

Poison pills are the defensive measure that companies use to prevent external sources from gaining control or exercising majority rights over them. In the process, the organizations either make the outstanding shares available to the existing shareholders at high discounts or increase the acquisition cost to a very high level and create disincentives if a takeover or management changes happen to alter the decision maker’s mind.

This negative way of defending or preventing acquisition appears to be adopted to ensure no control is gained or exercised over the company in question. This, in turn, affects the stock prices of the companies as well. It appears the same as consuming poison pills to get rid of all life problems. Hence, so named.

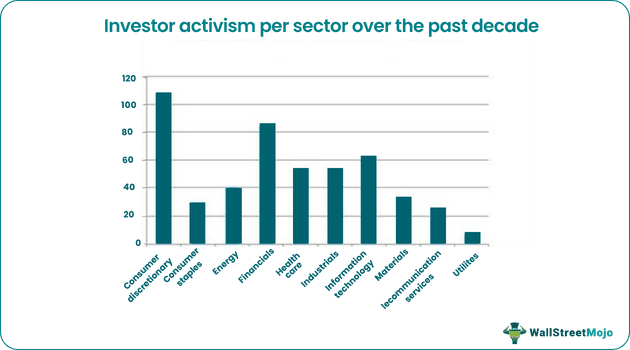

Hostile takeovers and defense mechanisms cannot be classified in black-and-white compartments. There are certain gray areas also. Not all takeovers are bad; neither are all takeover defense mechanisms in the company’s best interests. Some of these investors have significant knowledge of the industry and company affairs, sometimes much better than its management itself. These days, corporate raids or hostile takeovers have manifested themselves in a relatively constructive form called “Investor Activism” these days. Any act of investors to influence corporate paths or shareholders’ long-term goals is viewed as activism.

According to S&P Capital IQ, “The agendas vary among investors and focus on specific areas, including cost reductions, reorganizations, corporate spin-offs, revamped financial structures, greater leverage, and more shareholder-oriented uses of cash and liquidity to realize higher enterprise value in the public markets.”

S&P Capital IQ stated that; from 2005 to 2009, 89 activist actions occurred, while in the past five years, from 2010 to 2014, 341 actions took place. There has been a volume increase each year since 2010, and this trend has sustained itself strongly in 2015. Thus we can see that the practice that took the corporate world by storm in the 1980s is relevant even today.

Before ascertaining whether Poison Pills are doing any good to the company, we need to understand that any company has many stakeholders affected differently during a potential takeover. The board of directors has different financial stakes and responsibilities toward the company and the shareholders. Shareholders have a financial interest in maximizing the value of the company’s shares. At the same time, corporate executives who also have ownership in the company may either stand to gain or lose from the takeover.

Other company employees, usually at the lower and middle levels, stand to lose most of the time due to mergers. News of acquiring companies announcing mass layoffs during mergers is also not unheard of.

Video Explanation of Poison Pills

History

Every phenomenon in the world has a history behind it, and Poison Pills is no exception. The blatant occurrences of hostile takeovers and defense mechanisms were in full momentum in the 1980s. Hostile takeovers became the order of the day. In the 1970s, corporate raiders like T. Boone Pickens and Carl Icahn sent chills down the spine of many corporate boards. There was no legalized defense tactic in place. In 1982, M&A lawyer, Martin Lipton of Wachtell, Lipton, Rosen & Katz, came as a knight in shining armor and invented the “poison pill” defense to prevent hostile corporate takeovers. According to experts, this was the most significant legal development in corporate law in the 20th century.

The legality of poison pills had been vague when they first came in the early 1980s. However, the Delaware Supreme Court advocated poison pills as a valid defense tactic in its 1985 decision in Moran v. Household International, Inc.; many jurisdictions outside the U.S. consider poison pills as illegal and place constraints on their applicability.

So what’s the story behind such an awkward name? It dates back to the tradition of espionage prevalent during the monarchical era. Whenever an enemy caught a spy, he immediately swallowed a cyanide pill to escape interrogation and revelation of truth. Poison Pill owes its name to this practice.

Reasons

A “Poison Pill” is a popular defense mechanism for a “target company” wherein it uses shareholder’s rights issues as a tactic to make the hostile acquisition deal expensive or less attractive for the raiders. This strategy also acts as a tool to slow down the speed of potential hostile attempts in the future.

The Board of directors generally adopts them without the approval of shareholders. It also comes with a provision that the rights associated can be altered or redeemed by the board when required. It is to indirectly compel direct negotiations between the acquirer and the board to build grounds for better bargaining power.

It can pinch in two ways: They can either make an acquisition a very hard nut to crack, or they can have negative side-effects that unfold in various stages.

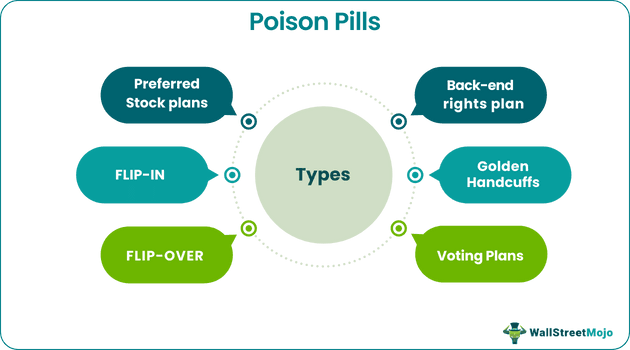

Types

Poison Pill is an all-encompassing term, and there are various forms in which it is triggered in a practical corporate setting. Some of the widely used tools are:

#1 – Preferred stock plans

Before 1984, when hostile takeover just jutted their ugly head, Preferred stock plans were primarily used as Poison pills. Under this plan, the company issues a dividend of preferred stock to the common shareholders, with voting rights. Preferred stockholders could exercise special rights whenever outsiders suddenly bought a large chunk of shares.

#2 – Flip-In

Post-1984, certain other methods also saw the light of the day. One such tactic is the Flip-in poison pill. When corporate raiders buy sizable holdings in a company, Flip in is one of the most preferred strikes back. Here the target company buys many shares at a discounted rate to counter the offer, which eventually leads to the dilution of control of the acquirer. E.g., if an investor buys more than 15% of the company’s stock, other shareholders from the bidder buy an increased number of shares. The greater the additional shares purchased, the more diluted the acquirer’s interest. It also increases the cost of the bid. Once the bidder gets a hint that such a plan is being executed, he may become cautious and become discouraged to pursue the deal further. It may also be possible that the bidder then comes up with a formal offer to the board for negotiation.

#3 – Flip-Over

Flip-over is the opposite of Flip-in and happens when the shareholders choose to buy shares in the acquirer’s company after the merger. Let’s say the target company’s shareholders exercise the option of buying two-for-one shares in the merged company at a discount. This option usually comes with a pre-determined expiration date and no voting rights.

Diluting the acquirer’s interest makes the deal quite expensive and exasperating. If the acquirer backs off, the target company can also redeem those rights.

#4 – Back-end rights plan

Under this defense mechanism, the target company shuffles employee stock-option plans and designs them to become effective in the event of any unwelcome bid. It entails giving shareholders the privilege to obtain shares with a higher value if the acquiring company takes a majority stake. This way, the acquiring company would not quote a lower price for the shares. However, if the acquirer is ready to offer a greater price, the Back-end rights plan falls through under exceptional circumstances. It is nothing but a move to deter the acquisition.

#5 – Golden Handcuffs

We all agree that employees are the biggest assets of a company. Golden handcuffs are nothing but various incentives offered to the crème-del-a-crème of the company to ensure that they stay on. Usually, Golden handcuffs are issued in deferred compensation, employee stock options (ESOPs), or restricted stock, which can be earned after the employee reaches a particular performance threshold.

However, not many of us know that Golden handcuffs can also be used as an anti-takeover mechanism. When an unsolicited bid happens, this Poison Pill gets triggered. The key staff becomes vested in stock options, and their golden handcuffs are removed. These employees, some with extremely rich experience and insight, are now free to leave the company. Therefore, the acquirer will lose key executives of the target company, which will make the path difficult for him to tread.

#6 – Voting Plans

Designed on the same lines as the Preferred Stock Plan and Flip-in, this tactic involves voting rights as a tool of controlling mechanism. When an investor obtains a substantial block of shares, preference shareholders (apart from the large block holder) become authorized to have super-voting rights. It is difficult and unattractive to obtain voting control by the bulk share purchaser.

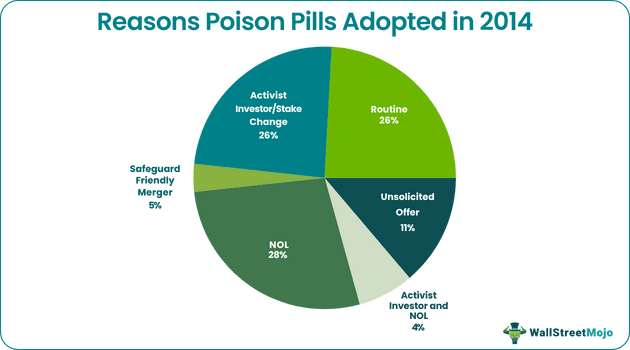

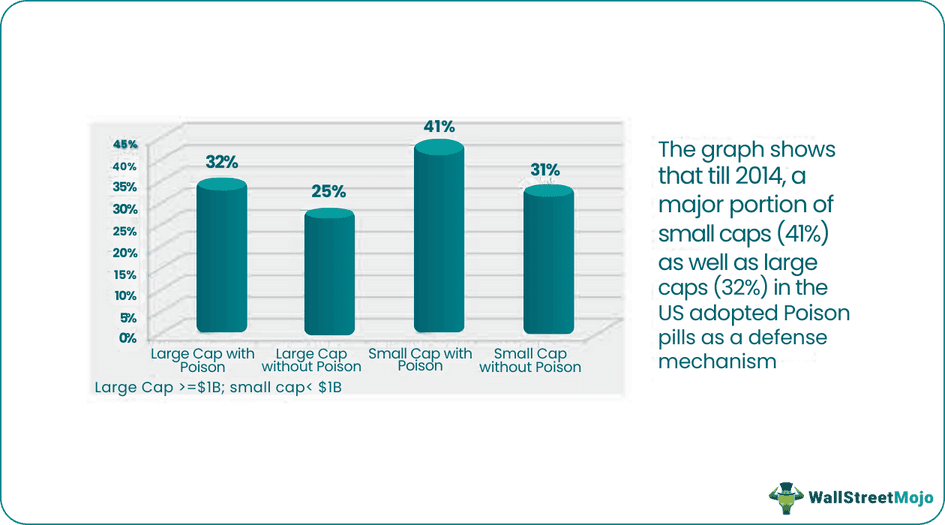

Trends

Let us have a look at the graphical representation of the common poison pills trends until 2014:

Source: The University of British Columbia

Examples

Let us consider the following examples to understand how poison pills in business and finance work:

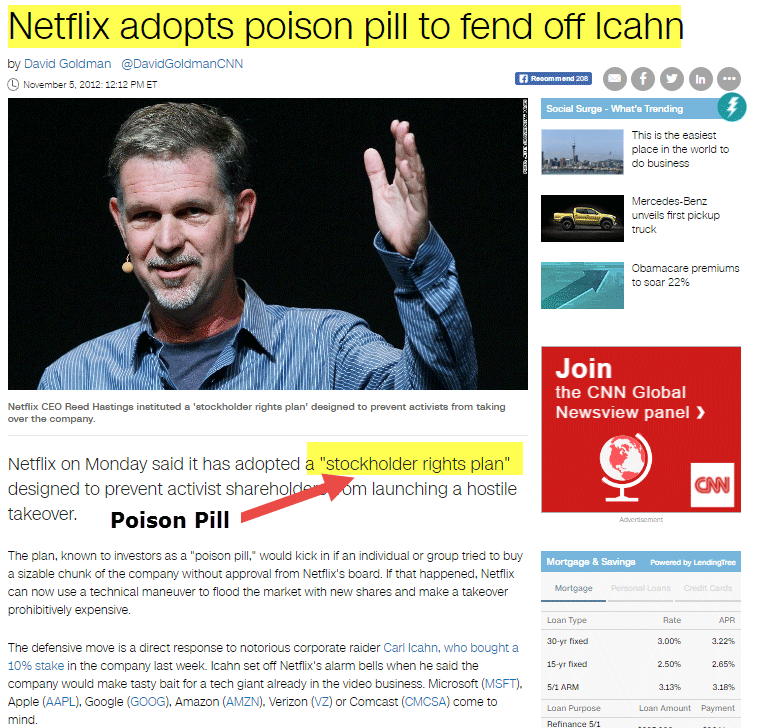

Example 1 – Netflix

Carl Icahn, an institutional investor, caught Netflix off-guard in 2012 by acquiring a 10% stake. The latter responded by issuing a shareholder’s right plan as a “Poison Pill,” a move that irked Carl Icahn to no end. A year later, he cut his holding to 4.5%, and Netflix terminated its right issue plan in December 2013

source: money.cnn.com

Example 2 – GAIN Capital

When FXCM Inc planned to acquire GAIN Capital Holdings, Inc. in April 2013, GAIN responded by triggering a “poison pill.” Rights were decided to be distributed to the common shares at the rate of one-for-one of the company held by stockholders. Upon the occurrence of an unforeseen event, each right would authorize stockholders to buy one-hundredth of a share of a new series of participating preferred stock at an exercise price of $17.00, which was later raised.

source: Leaprate.com

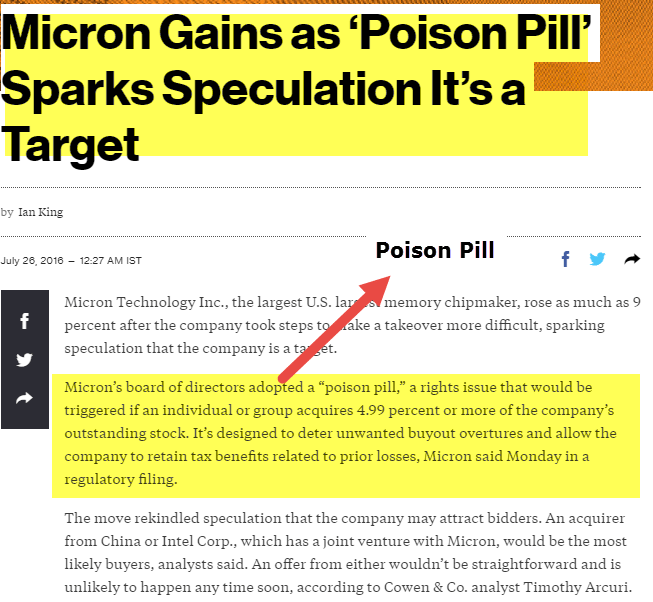

Example 3 – Micron Tech

The Board of Directors of Micron Technology Inc., the largest US memory chipmaker, adopted a “Poison Pill” strategy in the apprehension of a hostile takeover. The tactic was a rights issue that would be triggered if an individual or group acquired 4.99% or more of the company’s outstanding stock.

Source: Bloomberg.com

Example 4 – Pier 1 Imports

The agreement entitled every common stockholder the right to buy a fraction of junior preferred stock at the price of $17.50. The preferred shares would have similar voting terms to common stock, diluting the control of any shareholder capturing a big stake. More recently, in September 2016, Pier 1 Imports Inc resorted to the Poison Pill measure when hedge fund firm Alden Global Capital LLC disclosed a 9.5% stake in the former.

Example 5 – Covid 19

The concept of poison pills, which seemed fading from the finance and business sector, returned again during the Coronavirus pandemic with a new name “Crisis Pills.” In 2020, stock prices plummeted, and volatility levels increased in the markets across the world. Many companies, including airlines, retail businesses, etc., started facing challenges, which reflected their struggles, thereby affecting their market reputation.

As a result, the corporations became likely to be taken over by the more powerful entities in the market. Hence, many companies announced adopting a poison pill strategy.

Advantages and Disadvantages

Poison pills are measures that prevent businesses from being considered a good acquisition option. As a result, they have no fear of getting controlled by those they don’t want. While there are benefits to the process, there are limitations to it as well. Thus, before an entity chooses to opt for poison pills, it must know both the pros and cons of considering this measure.

Let us have a quick look at these:

| Advantages | Disadvantages |

|---|---|

| It is a strong defense mechanism for a “target company,” allowing the company to identify fruitful acquisitions and discourage the actions of corporate raiders. The “Poison Pill” also acts as speed-breakers of potential raids. The spin-off effects are usually positive and could lead to shareholders earning higher premiums if an acquisition is favorable. | It has the power to impact shareholder value adversely. A large number of shares impact its valuation. The flip leads to more purchases at a lower share price. E.g., in 2008, Microsoft offered Yahoo! shareholders $31 per share, representing a 62% premium at the time, but pulled out its hand after being stung by the “Poison Pill” Yahoo! shares prices took a hit since this proposal and its Head Jerry Pinto also lost his position. |

| Poison Pills are usually triggered as a negotiation tactic to clinch a sweeter deal. It allows the company to buy time and grants management the right to dictate the terms of any takeover in a most lucrative manner. |

Shareholder Value Lost Due to Poison Pills

Source: Harvard Law School Forum

Poison Pills & Golden Parachute

Golden parachutes and poison pills are two terms that are widely used when companies look for prevention against unwanted or hostile takeovers. While poison pills are the name given to collective anti-takeover measures, golden parachutes are one of the types of such pills used to ensure no unwanted source gains control over the existing shareholders by taking over an organization.

When the golden parachutes strategy is applied, the existing shareholders or the company make it difficult and extremely expensive for new interested shareholders to replace the main personnel of the company.

Frequently Asked Questions (FAQs)

Are poison pills legal?

This strategy is generally legal in the United States and many other countries. For example, in the US, the legality of poison pills is governed by state laws, and most states have statutes that allow companies to adopt such plans. However, the legality is not absolute and can be challenged in the court.

What are stock poison pills?

Poison pills are facilities companies possess in stock issuances that protect one from getting a controlling stake. Typically, they set share ownership limits that trigger more issuing of shares to stockholders at a discount or for free.

Are poison pills good for shareholders?

This defense mechanism can have negative and positive implications for shareholders, and their overall impact will depend on the specific circumstances of the target company. For example, some believe they benefit shareholders by giving the company’s management and Board of directors more time to explore other options, such as seeking favorable bids and ensuring shareholders receive fair value for their shares.

Recommended Articles

This article has been a guide to Poison Pills and their Definition. Here, we explain its types, examples, connection with golden parachutes, and history. You can also have a look at the following articles related to the above topic: