Recordkeeping Definition

Recordkeeping is a primary stage in accounting that entails keeping a record of monetary business transactions, knowing the correct picture of assets-liabilities, profits, loss, etc. In addition, it assists in maintaining control of the expenses to minimize the expenditure and have important information for legal and tax purposes. In other words, a recordkeeping system is the backbone of any company’s financial structure.

This system not only helps organizations to take decisions for daily activities but also provides detailed insights into the company’s future plans and budgeting for the same. Moreover, it also helps in the governance of the employees and the reporting structure. It is an all-pervasive function within the organization that helps managers across levels to ascertain their workforce’s efforts.

- Recordkeeping is a fundamental aspect of accounting that involves keeping a systematic record of monetary business transactions to determine the accurate picture of assets, liabilities, profits, losses, and other financial indicators.

- It helps businesses control expenses, minimize costs, and provide crucial information for legal and tax purposes.

- Financial records are essential for management to plan the company’s daily operations and make strategic decisions. They rely on ongoing reporting from intermediate levels regarding the organization’s financial status.

- Financial records play a critical role in governing all strategic choices made by the organization.

Recordkeeping Explained

Recordkeeping is the art of recording and disclosing financial transactions. It requires expertise and tactics to help maintain the organization’s image and help obtain funding and bid the tenders of business. In amplifying the accuracy of the transactions, recordkeeping gives a big push and helps maintain the image of the business as an ethical organization in the market.

It is important for businesses to follow recordkeeping principles as it can show the management details regarding the items that are selling faster than the other, if their plans are on track or underperformance is seeping through the plans of the organization.

It also indicates the growth of the business overall. In simpler words, the documentation of every single transaction, daily records, and employee performances within the organization. It gives an overview of the financial and employee-centric growth.

It is important to note that any changes in the method of record-keeping can be allowed only if:

- Substance over form is to be considered.

- For better disclosure requirements

- Needed by accounting standards

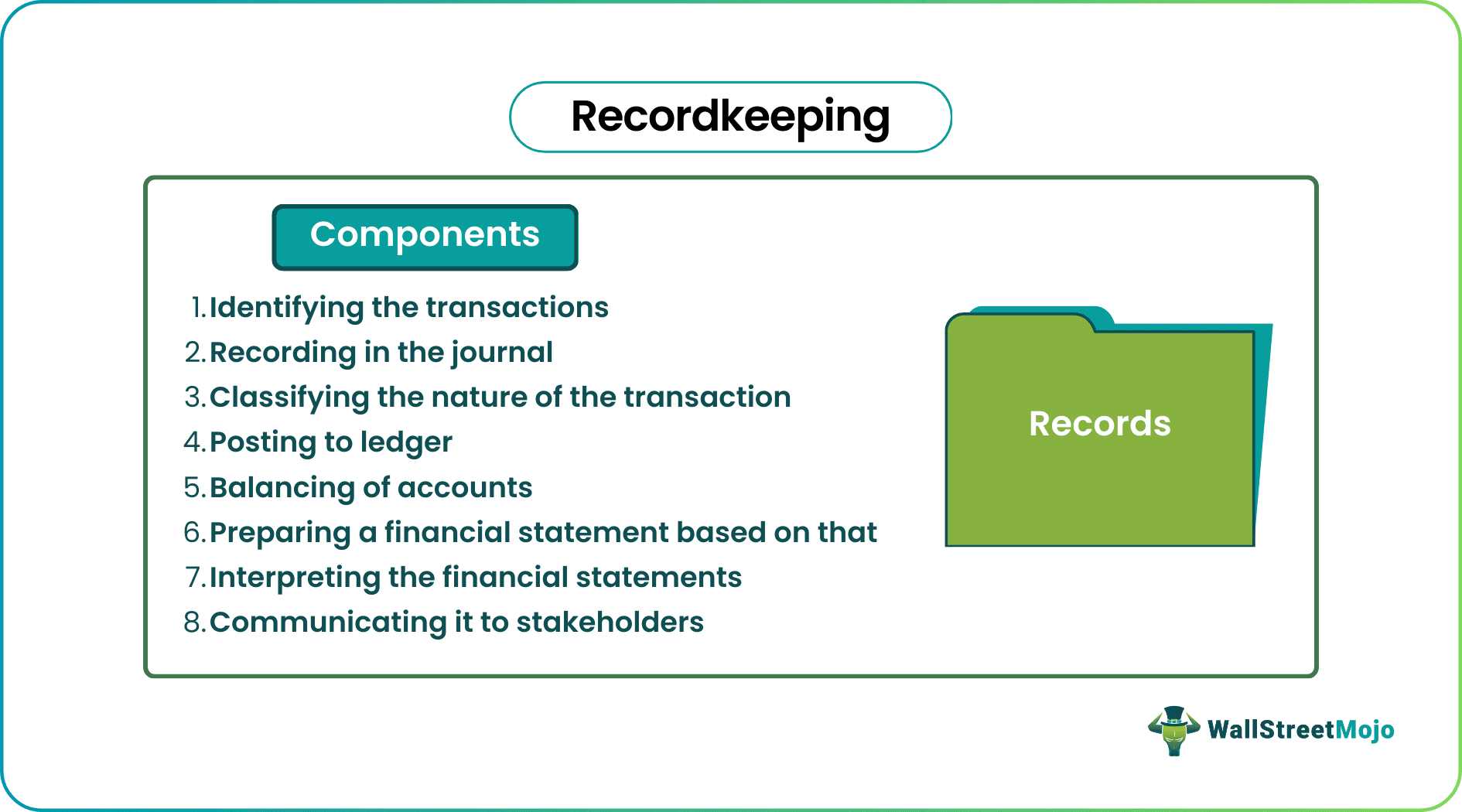

Procedure

Let us understand the procedures involved within the recordkeeping system and how it helps an organization document their growth through the discussion below.

- Identifying the transactions

- Recording in the journal

- Classifying the nature of the transaction

- Posting to ledger

- Balancing of accounts

- Preparing a financial statement

- Interpreting the financial statements

- Communicating it to stakeholders

Requirements

For employers above 10 employees or more in some states, it is important to maintain the documentation of the following checkpoints according to the recordkeeping principles.

- Full name of the employee

- Address

- Date of Birth

- Daily hours of work

- Defining work week

- Social Security Number

Examples

Let us understand the recordkeeping principles with the help of a couple of examples.

Example #1

ABC Limited is a sole proprietor firm operating small shops in Atlanta. It is trading in clothes and has its main inflow and outflow as follows:

- Inflows: Sale proceeds from Customer

- Outflows: Material Purchase from vendors and payment of related expenses

For recordkeeping purposes, ABC Limited will have to maintain daily cash books for maintaining the petty cash and bank balances. At the end of the year, they have to prepare a profit and loss account and Balance sheet to verify the profitability during the year. It is one of the simplest ways of maintaining business transaction records.

Example #2

- Amazon.com is a multinational corporation having operations throughout the globe while employing millions of people. Every day millions of transactions are carried out. To maintain the company’s interest, ensure the proper compliance of statutes, and retain the confidence of the stakeholders, bookkeeping must be carried out.

- Separate teams need to be placed to ensure that every monetary transaction carried out by the business should be recorded in the books without any deviation. Also, such bookkeeping must ensure that transactions are recorded as per the locally applicable generally accepted accounting principles and applicable other statutes.

Criticism

Despite showing a detailed overview of the business, there are a few factors that do not impress organizations and users of the recordkeeping principles. Let us understand the criticism towards this system through the points below.

- Only Monetary Transactions can be Recorded – In business, both monetary and non-monetary aspects are essential. However, record-keeping covers only financial transactions. Non-monetary virtues like trained staff cannot be recorded in the books of accounts.

- Effects of Price Level Changes are not Considered – Inflation is a phenomenon that needs to be considered while recording the assets. However, in accounting, inflation cannot be factored-for while recording the transactions.

- Historical-based Accounting – All the assets are to be recorded as historical costs. This concept will not help identify the present worth of the asset in the market.

Advantages

It is important for any organization irrespective of their size and nature of business to record the growth of their plans and actions. Let us understand the advantages of inculcating a recordkeeping system through the explanation system.

- Permanent and Reliable Record – It helps maintain the permanent record of all the transactions, which will help ensure the reliability of data.

- Arithmetical Accuracy of the Accounts – Continuous recording of transactions will assist in identifying any arithmetical inaccuracies that might have occurred—for example, excess payment to suppliers or double treatment of any transactions.

- Net Result of Business Operations – The profit earned during the given period will be based on ongoing business operations.

- Ascertainment of Financial Positions – It helps identify the business’s financial position.

- Calculation of Dues – All the outstanding liabilities and dues at a given time can be calculated based on the accurate financial statements prepared.

- Control Over Assets and Borrowings – It features better control over assets, and borrowings can be undertaken; this will help manage the funds and various positions of business.

- Identifying Dos and Don’ts – Financial statements help find things that went south and need to be rectified to ensure better operations in the future.

- Taxation – It is highly recommended and needed by tax authorities. To complete their assessments, business people have to appropriately maintain the records, which will help determine the tax liability over them.

- Management Decision Making – Management is highly dependent on the financial records to plan the business operations. Moreover, they also need continuous reporting by the middle level about the progress made in finance terms. The financials maintained by the organization governs all the strategic decisions.

- Legal Requirements – There is a massive requirement of statutes, local GAAPs, IFRSs, etc., to maintain the proper books of account and ensure transparency.

Disadvantages

Despite the various advantages as mentioned above there are a few factors that appear to be hassles or hurdles in the process. Let us understand the disadvantages of the recordkeeping principles through the points below.

- Clerical – Recordkeeping is a highly tedious and perpetual job for large organizations. It becomes tough for them to maintain the same.

- Manual and Monotonous – It is a highly manual job. The same work needs to be carried out every time the transaction occurs. This makes it a highly monotonous job.

- Subjective needs to be Checked before Analyzed – Various accounting aspects like depreciation, stock valuation, etc., require assumptions that make the accounting highly subjective. The viability of such assumptions needs to be verified before analyzing the financial statements.

Frequently Asked Questions

What are IRS recordkeeping requirements for businesses?

In order to comply with IRS regulations, businesses must maintain records of all financial transactions and activities impacting their taxes for at least three years after filing the tax form or two years after the tax payment, whichever is later. The records must encompass all sources of income, expenses, and deductions and must be accurate, complete, and readily available for the IRS to inspect.

What is manual vs. digital recordkeeping?

Manual recordkeeping involves maintaining records by hand, using pen and paper, while digital recordkeeping involves using electronic tools such as spreadsheets, databases, or accounting software to keep records. Manual recordkeeping is more time-consuming, prone to errors, and less efficient than digital recordkeeping.

What are the impacts of poor recordkeeping?

Poor recordkeeping can significantly impact businesses, including inaccurate financial statements, non-compliance with tax laws, difficulty making informed business decisions, and potential legal and financial consequences. Additionally, it can lead to lost revenue, decreased efficiency, and a damaged reputation.

Recommended Articles

This article has been a guide to Recordkeeping and its definition. Here we explain the recordkeeping procedure and examples, advantages, and disadvantages. You can learn more about excel modeling from the following articles –