Part of our Balance Sheet guide

Non-Current Liabilities Examples Explained

Non-Current liabilities show the real burden on the company, and default may lead to the closure of the business. Hence, it is always necessary to verify the factors that can meet such obligations and hedge themselves from bankruptcy. Also, disclosing all the non-current liabilities is necessary for the prescribed format, and the standard gives valuation per the guidelines.

For investors, stakeholders, and analysts, want to ensure that the company they are investing in is clear of any suspicious activity and that the revenue generated through the primary revenue-generating activity suffices the debt obligations and other such commitments. However, in the real world with stiff competition and constant technological advancements, it might not be as easy to do so.

Therefore, companies often take up short and long-term loans to fund their projects and growth plans. It becomes important for the top management to ensure that the ratio of debt and the projected growth of the company are not lopsided. There have been multiple companies that have built an empire through debt funding and repaid them in a timely manner. However, the number of companies that do not fulfill their debt obligations is numerous too.

The reason behind discussing the factor of taking up loans to grow a company and other factors is to reiterate the fact that investors generally look at the total debt to total assets ratio to gauge the amount of leverage the company has used. The lower it is, the better cashflow management it indicates.

In a non-current liabilities example balance sheet, it is also important to show signs of active efforts to reduce the debt obligations. In an ideal scenario, any business always strives to be a debt-free company.

Current Liabilities in Video

List

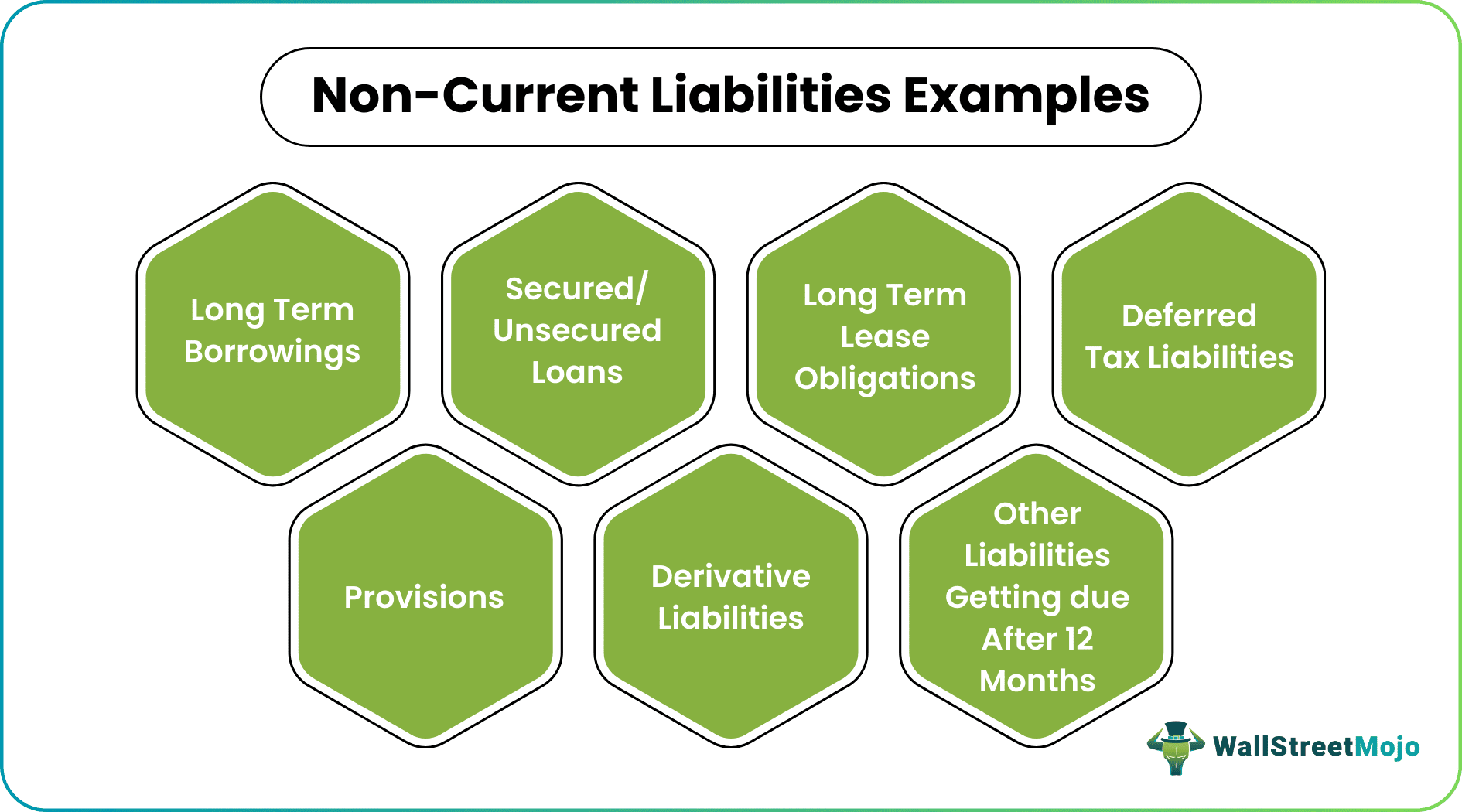

Non-Current Liabilities are those sets of liabilities taken to undertake capex. Its maturity is beyond 12 months from the reporting date

Let’s look at the complete list of non-current liabilities with Examples.

#1 – Long Term Borrowings

Long Term Borrowings are the acceptance of the funds for the need for meeting capital expenditure and making strategic decisions. Therefore, such funds need to be utilized judiciously and only for the purpose for which it was borrowed—moreover, such funds are to be disclosed at amortized cost per the requirement of IFRS 9.

#2 – Secured/Unsecured Loans

The basic difference between Long term and Secure/Unsecured loans is that borrowings can be from anyone, from a retail investor to NBFCs. At the same time, most of the Loans will come from financial institutions against which assets will be mortgaged based on the structure set up as per the agreed terms and conditions.

#3 – Long Term Lease Obligations

Lease payments are the most fundamental and common expenditure a corporation must bear to fulfill its asset requirement. Such lease payments needed to be structured and framed per the IFRS and locally General Acceptable accounting practices. Moreover, the disclosure must also be verified based on the applicable regulations.

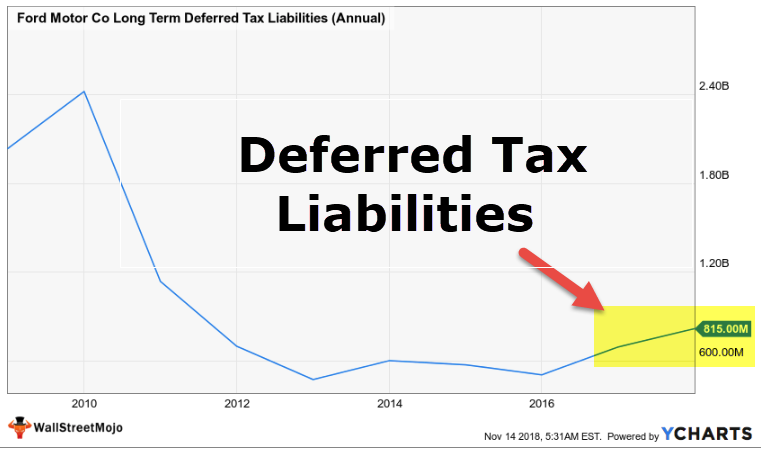

#4 – Deferred Tax Liabilities

Deferred Tax Liabilities show that one has disclosed less income in the current year than books of account, and in the future, the arising tax liabilities will be set off against the same. Deferred Tax liabilities must be created to balance the timing differences between books of account and income tax computation. The basic intent is that one cannot claim more gain in tax calculation by adopting different accounting methods and taking less profit to disclose to the concerned department.

#5 – Provisions

As per the matching concept of the accounting principles, all the expenses and revenues must be recognized in the year to which it is attributed. Therefore, even though the expenditure of the 1st year is incurred in the 2nd year, the expenditure of the 1st year is needed to adequately hit the targeted profit and loss account. Hence, to meet this guideline, a concept named provision is accepted under which an amount equivalent to expense will be transferred to a clearing profit and loss account. Hence, to meet this guideline, a concept named provision is accepted under which amount equivalent to expense will be transferred to a clearing account, which will be reversed next year as and when it will be incurred. Provisions may be for one year, five years, or even for more periods.

#6 – Derivative Liabilities

Current stock market data is highly flexible. One can create and arrange the transactions based on their needs and earn the gains based on the insights for any specific underlying assets. The main aim of such a derivative instrument is to hedge themselves from the transaction exposure they will face in the future. Therefore, there are full chances of earning loss or profit in a derivative instrument. Derivative instruments must be valued at fair value on every reporting date. Hence, on a fair valuation, if one is getting a mark to market negative, it will be considered derivative liabilities and need to be disclosed in a balance sheet.

#7 – Other Liabilities Getting due After 12 Months

Every company has to fulfill various types of obligations as and when getting due in business. Moreover, such obligations needed to be structured and recorded in the books of account based on the applicable financial regulation.

From the above list of non-current liabilities, we can conclude that.

Non-Current Liabilities = Long term lease obligations + Long Term borrowings + Secured / Unsecured Loans + Provisions +Deferred Tax Liabilities + Derivative Liabilities + Other liabilities getting due after 12 months.

Examples

Let us discuss the concept and its practicalities with the help of a few examples.

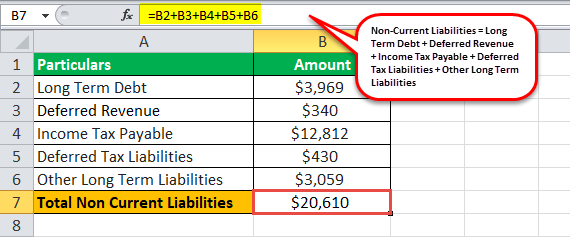

Example #1

Alphabet Inc. has Long term debt of $ 3969 Mn, a Deferred Revenue of $ 340 Mn, an Income Tax of $ 12812 Mn, and Deferred Tax liabilities of $ 430 Mn, Other Long term liabilities of $ 3059 Mn.

Calculation of Non-Current Liabilities Example:

Non-Current Liabilities = $ 3969 Mn + $ 340 Mn + $ 12812 Mn + $ 430 Mn $ 3059 Mn

= $ 20610 Mn.

Hence Alphabet Inc. has non-current liabilities of $ 20610 Mn as of 31st Dec 2018.

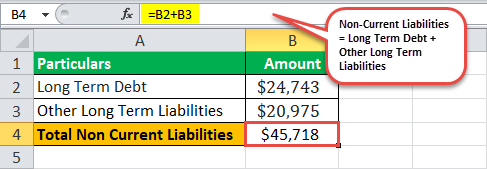

Example #2

Amazon.com, Inc. has a long term debt of $ 24743 Mn, Other long-term liabilities of $ 20975 Mn as of 31st Dec 2018.

Calculation of Non-Current Liabilities Example:

Non-Current Liabilities = $ 24743 Mn + $ 20975

= $ 45718 Mn

Hence, Amazon.com, Inc has non-current liabilities of $ 45718 Mn as of 31st Dec 2018.

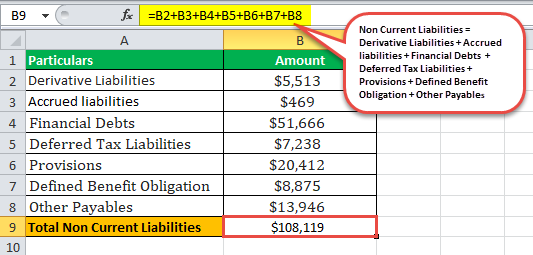

Example #3

BP (UK group company) has Derivative Liabilities of $ 5513 Mn+ Accrued liabilities but not Met of $ 469 Mn, +Financial debts of $ 51666 Mn + Deferred Tax Liabilities of $ 7238 Mn + Provisions of $ 20412 Mn, Defined Benefit obligation plans of $ 8875 Mn + Other payables of $ 13946 Mn as on 31st Dec 2017.

Calculation of Non-Current Liabilities Example:

Non-Current Liabilities= $ 5513 Mn + $ 469 Mn + $ 51666 Mn + $ 7238 Mn + $ 20412 Mn + $ 8875 Mn + 13946 Mn

= $ 108119 Mn

Hence BP has non-current liabilities of $ 108119 Mn as of 31st Dec 2017.

Non-Current Liabilities Vs Current Liabilities

Now that we have a detailed understanding of the concept and its intricacies, you must have noticed that have compared total non-current liabilities examples with current liabilities at different parts of the articles. To ensure a deeper understanding of the concept, let us discuss the contrasting concept as well through the comparison below.

Non-Current Liabilities

- Non-current liabilities refer to the payments a business is due to pay but need not be settled within one financial year.

- The payment terms of these liabilities exceed 12 months.

- They appear on multiple balance sheets as they are obligations that are paid over multiple years.

- They are accrued majorly due to the long-term financial needs of the company.

- The repayment of such liabilities does not have a major impact on the working capital. However, their interest payment has a significant impact on the working capital of the company.

- Since the term of the loan or debt is longer, it usually requires the company to provide collateral or security.

Current Liabilities

- Current liabilities are debt or financial obligations that must be settled within one financial year.

- The credit period of such obligations is lesser than 12 months.

- They appear only on one balance sheet as they become due for settlement before the next one is prepared.

- These obligations are accrued mainly due to the daily operations of the company.

- The repayment of such liabilities reduces the working capital.

- Since they are transacted over a short period of credit, the company usually does not put forth any collateral or security for the same.

Recommended Articles

This article has been a guide to Non-Current Liabilities Examples. Here we provide you with a complete list of Non-Current Liabilities with the help of examples (Amazon, Alphabet, BP). You may learn more about financing from the following articles –