NBFC Meaning

NBFC stands for Non-banking Financial Company that offers different types of financial services. They do not possess a banking license but provide specific banking services and generally refrain from accepting demand deposits from the public.

They are also known as non-bank financial institutions (NBFIs) and shadow banks. They operate outside the traditional banking system by engaging in and providing various activities like offering loans, retail sector-housing finance, issuing securities, marketing and selling insurance, hire purchase finance, equipment lease finance, and investments.

- NBFC’s full form is a Non-banking Financial Company. They are designed to offer different financial services, including bank-related financial services.

- They are different from commercial banks. They do not possess a banking license but provide specific banking services and generally refrain from accepting demand deposits from the public.

- In the United States, they are generally classified into foreign nonbank financial companies, U.S. nonbank financial companies, and U.S. nonbank financial companies supervised by the Federal Reserve Board.

- LIC Housing Finance Limited is an example of a non-banking financial company in India.

NBFC (Non-Banking Financial Company) Explained

NBFC’s evolution in Europe and America is traced back to the nineteenth and early twentieth centuries due to increased urbanization. The expansion of cities and the need for automobiles produced a huge demand for loans. To meet this need, numerous private groups began to create building and loan associations and private enterprises offering installment credits to vehicle buyers. The sector’s expansion reflected the flow of savings and multiple types of investments.

In India, non-banking financial companies have succeeded in increasing the range of financial services offered to the public during their growth period. However, there is a significant NBFC crisis in India at certain times due to the liquidity crunch faced by such companies. Hence, governments are taking the initiative to impose strict rules and regulations for controlling the activities of shadow banking while preserving their growth potential because they are critical to a nation’s economic development.

Non-banking financial companies benefit a nation in many ways, specifically for developing countries. It creates economic efficiencies through financial innovations and performs supplementary to banking activities. It facilitates financial inclusion by creating easy access to credit and useful and affordable financial products and services delivered in an ethical and sustainable means.

It is different from the formal banking system. Commercial banks are confronted with stringent regulatory constraints; in such cases, NBFCs play a complementary role for commercial banks by connecting the financing needs of the consumers to customized financial products. A comparison between commercial banks and non-banking financial companies discloses the following:

- Unlike the banks, NBFCs are not subjected to stringent and substantial regulations.

- Lack of transparency in non-banking financial companies’ business operations

- Non-banking financial companies don’t derive funds from public deposits, but they issue securities, borrow from banks, etc.

- The liabilities of non-banking financial companies are not insured, but commercial bank deposits are often guaranteed to a limited extent by the government.

- During a financial crisis, banks have easy access to central bank liquidity.

- Non-banking financial companies are doing more fee-based activities than fund-based ones.

- Non-banking financial companies have more flexible structures than banks in the organized sector.

- Non-banking financial companies bridge the credit gap.

The Hargreaves Lansdown provides access to a range of investment products and services for UK investors.

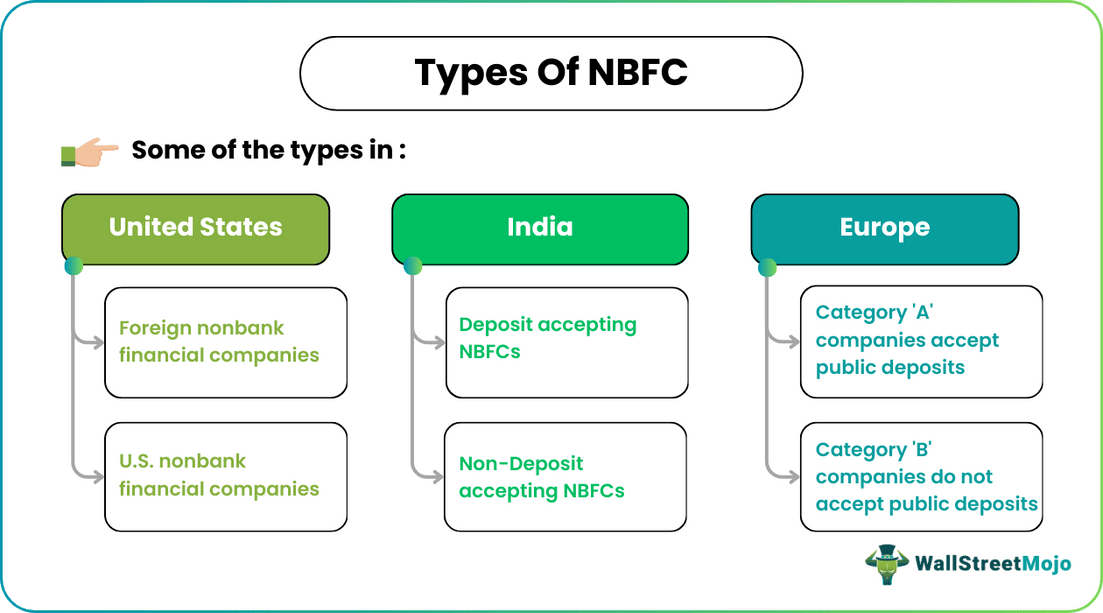

Types of NBFC

In the United States, it is generally classified into three based on the Dodd-Frank Wall Street Reform and Consumer Protection Act:

- Foreign nonbank financial companies

- U.S. nonbank financial companies

- U.S. nonbank financial companies supervised by the Federal Reserve Board

In India, the categories are:

- Based on the types of liabilities: Deposit and non-deposit accepting non-banking financial companies

- Non-deposit taking NBFCs by their size: Systemically important and other non-deposit holding companies (NBFC-NDSI and NBFC-ND)

- Based on the activity: Asset Finance Company (AFC), Investment Company (IC), Loan Company (LC), Infrastructure Finance Company (IFC), Systemically Important Core Investment Company (CIC-ND-SI), Infrastructure Debt Fund, Non-Banking Financial Company, Non-Banking Financial Company – Factors (NBFC-Factors), Mortgage Guarantee Companies (MGC), Non-Operative Financial Holding Company (NOFHC)

In Europe:

- Based on liability structure: Category ‘A’ companies accept public deposits, and Category ‘B’ companies do not take public deposits (Category ‘B’ companies with under a billion euros and category ‘B’ companies with over €1B)

- Based on the nature of the activity: Development finance institutions, leasing companies, investment companies, modaraba companies, house finance companies, venture capital, discount & guarantee houses, corporate development companies.

NBFC Example

LIC Housing Finance Limited is an example of a non-banking financial company in India. It is a subsidiary company of Life Insurance Corporation of India (LIC). Established in 1989, it became a listed company in 1994; it’s the leading entity in the “housing finance mortgage loan sector” in India. Its primary function is to supply consumers with home loans and mortgage loans. In addition, it also provides financial assistance for building repairs and renovations.

Disclosure: This article contains affiliate links. If you sign up through these links, we may earn a small commission at no extra cost to you.

Frequently Asked Questions (FAQs)

What are an NBFC and its functions?

Non-banking financial companies are financial institutions offering specific financial services, including some banking services. However, they do not have a banking license and generally don’t have to provide the demand deposit account (DDA) to the public. Its functions and businesses include offering loans, home mortgages issuing securities, selling insurance, leasing activities, etc.

What are NBFC examples?

Examples are housing finance companies, merchant banking companies, stock exchanges, companies engaged in the business of stock-broking/sub-broking, currency exchanges, venture capital fund companies, and insurance companies.

What is the difference between banks and NBFC?

Non-banking financing companies engage in lending activities and make investments. For these reasons, their activities are similar to that of banks. However, non-bank financing companies are different from banks in the following ways:

Demand deposits: Non-banking financing companies cannot accept demand deposits which is withdrawable on demand.

Payment mechanism & self-drawn cheques: Non-banking financial companies are not allowed to form part of the payment and settlement system and cannot issue cheques drawn on themselves.

Recommended Articles

This has been a Guide to NBFC and its Meaning. We explain types of Non-banking financial company, examples, and its comparison with conventional banks. You can learn more about investment banking from the articles below –