Part of our Revenue Recognition guide

Deferred Revenue Meaning

Deferred revenue is the amount of income earned by the company for the goods sold or the services; however, the product or service delivery is still pending. Examples include advance premiums received by the insurance companies for prepaid insurance policies, etc. Thus, the Company reports it as deferred revenue, a liability rather than an asset, until it delivers the products and services.

It is also called unearned revenue or deferred income. It occurs when a company receives payment for goods or services in advance but has yet to fulfill its obligation to deliver those goods or services. In simpler terms, a deferred revenue journal entry represents income that the company has received but has not yet recognized as revenue on its income statement.

Deferred Revenue Explained

Deferred revenue accounting is critical to avoiding misreporting of assets and liabilities. It is essential for Companies that get advance payments before it delivers their products and services. The bottom line is that once the Company receives money instead of goods and services to be done in the future, it should report it as deferred income liability. It will realize such revenue only after the goods and services are provided to the customers. If the Company realizes the revenue as it receives the money, it will overstate its sales. However, deferred income is essential to the Company as it helps it manage its finances and cover operating activities costs.

One common scenario where deferred revenue arises is in subscription-based businesses. Consider a software company that receives an annual payment for its services upfront. Until the company delivers the software or service throughout the year, it doesn’t recognize the total amount as revenue. Instead, it gradually recognizes the revenue throughout the subscription period, aligning with the timing of the service provided.

From an accounting perspective, deferred revenue expense appears as a liability on the balance sheet. This is because the company has a responsibility to fulfill the product or service for which payment has been received. As the company satisfies its obligation, the deferred revenue decreases, and the corresponding amount is recognized as revenue on the income statement.

Understanding deferred revenue is crucial for both investors and businesses, as it impacts financial statements and reflects the company’s financial health. It provides insights into the company’s ability to generate future revenue and fulfill its commitments to customers.

Deferred Revenue (Income) Video Explanation

Examples

Now that we understand the basics and related factors of the deferred revenue journal entry, let us apply the theoretical knowledge to practical application through the examples below.

Example #1

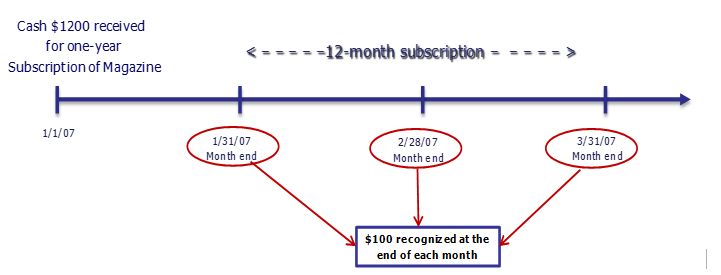

A magazine subscription business where this revenue is a part of the business. Suppose a customer has subscribed for a monthly magazine subscription for one year and paid the whole amount. Let us assume that the customer pays $1200 for the 1-year magazine subscription. The customer will receive the first edition as soon as he pays and the remaining 11 editions every month as they are published. Thus, the Company will account for the cost of 11 magazines to be delivered in the future as unearned revenue and as a deferred revenue liability. As the Company starts delivering these magazines, it will realize them from unearned revenue liability to assets.

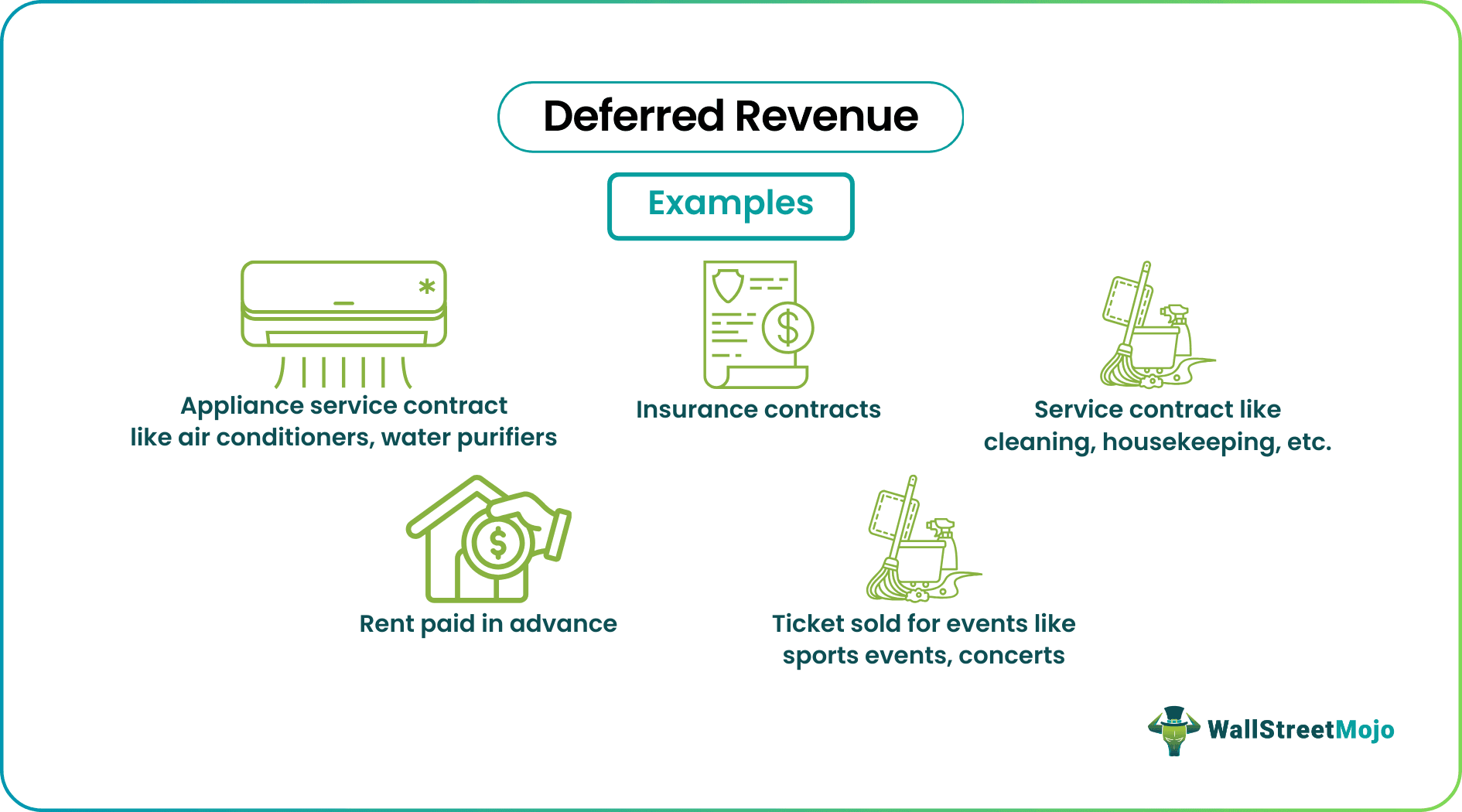

Other examples are:

- Service contracts like cleaning, housekeeping, etc.

- Insurance contracts

- Rent paid in advance

- Appliance services contracts like Air conditioners, water purifiers

- Tickets sold for events like sports events, concerts

Example #2

Typically, it is reported under current liabilities. However, if the deferred income is not expected to be realized as actual revenue, it can be reported as a long-term liability.

As we see below, Salesforce.com’s deferred income is reported under the current liability section. It is $7094,705 in FY2018 and $5542802 in FY2017.

source: Salesforce SEC Filings

Salesforce

Deferred income in Salesforce consists of billing customers for their subscription services. Most subscription and support services are issued with annual terms resulting in deferred income.

source: Salesforce SEC Filings

As noted below, deferred income is reported as the largest in the January quarter, where most large enterprise accounts buy their subscription services. Please note that Salesforce follows the fiscal year with 31st January year-end.

source: Salesforce SEC Filings

Accounting

Suppose a Company XYZ hires a housekeeping Company MNC to look after the cleaning and maintenance of its offices. The contract is for 12 months, and Company XYZ pays $ 12,000 in advance for a year. Thus, at the start of the contract and time of payment, MNC has not yet earned $ 12,000 and will record it:

| Account | Debit | Credit |

|---|---|---|

| Cash | $12,000 | |

| Deferred Revenue | $12,000 |

It is how Deferred Revenue on the Balance Sheet will look like

Now, after working for a month, MNC has earned $ 1000, i.e., it has provided its services to XYZ. Thus, it will accrue its earning

| Account | Debit | Credit |

|---|---|---|

| Deferred Revenue | $1,000 | |

| Service Revenue | $1,000 |

Hence, $ 1000 of deferred revenue expense will be recognized as service revenue. Service revenue will, in turn, affect the Profit and Loss Account in the Shareholders Equity section.

Recognition

Deferred income should be recognized when the Company has received payment in advance for a product/service to be delivered in the future. Such payments are not realized as revenue and do not affect the net profit or loss.

Deferred revenue recognition in a 2-way step:

- Increasing the cash and increasing deposit/deferred income on the liability side

- After the service is provided, decreasing deposit/deferred income and increases the revenue account

Similarly, this will impact the Cash flow statement of the Company:

- At the time of payment of the contract, realize all the cash received as cash from operating activities.

- After the Company starts delivering the goods, no cash will be recorded for that particular contract.

Time to Realize

The time of reporting real revenue may depend on the contract terms and conditions. Some may record real revenue monthly by debit the deferred income, while others may be required to do so after all the products and services are delivered. In such cases, this may lead to varied net profits/losses reported by the Company. The Company may have a period of high profits (when this revenue is realized as actual revenue), followed by periods of low profits.

Why Do Companies Report It?

While the Companies do not have a choice as per the accounting principles not to record deferred income journal entries, however, there are many advantages of doing so:

- As the Company’s deferred income is accrued and realized over time, so are the revenues using the concept of deferred revenue accounting. The payments made by the customers can vary, and this will impact the financial performance of the Company. Shareholders may not like such variable and volatile performance; hence, revenue is reported when earned and not paid.

- This safeguards investors’ interest as the Company cannot treat deferred income as its assets, which will overvalue its net worth. It provides that the Company has outstanding liabilities before it can realize its revenue and convert it into assets.

- It provides information that the Company owes and is liable to its customers. Although the Company has received the cash payment in advance; however, it is still at risk until the Company has performed its duties.

- The Company uses the deferred income to finance its operations without pledging its assets or taking debt from banks and other financial institutions.

Deferred Revenue Vs Unearned Revenue

Let us understand the differences between deferred revenue and unearned revenue through the comparison below.

Deferred Revenue

- Deferred revenue represents payments received in advance for goods or services that a company has not yet delivered or rendered.

- Revenue recognition occurs over time as the company fulfills its obligation, typically recognized gradually over the service or product delivery period.

- Recorded as a liability on the balance sheet until the revenue is earned, at which point it transitions to the income statement.

- Often observed in subscription-based models where customers pay upfront for services that will be provided over a specific period, such as annual software subscriptions.

- Offers insights into a company’s ability to generate future revenue and fulfill ongoing commitments, serving as an indicator of operational efficiency and financial health.

Unearned Revenue

- Unearned revenue is synonymous with deferred revenue, representing payments received before the delivery or completion of goods or services.

- Similar to deferred revenue, unearned revenue sees recognition over time as the company fulfills its obligation to the customer.

- Initially recorded as a liability on the balance sheet, transitioning to the income statement as revenue is earned.

- Commonly found in industries with advance payment requirements, such as prepaid insurance or annual maintenance contracts.

- Provides a clear picture of a company’s financial commitments and the revenue that is yet to be recognized, influencing overall financial statements and reflecting the company’s performance and fiscal responsibilities.

Recommended Articles

This article has been a guide to Deferred Revenues meaning. Here we explain its accounting, why companies report it, examples, and compare it with unearned revenue. You may also have a look at these articles below on accounting basics –

Recommended Articles

Continue with these closely related articles from the same guide.