Part of our Balance Sheet guide

Examples of Long-Term Liability

Long-Term Liabilities refer to those liabilities or the company’s financial obligations, which is payable by the company after the next year. Examples include the long-term portion of the bonds payable, deferred revenue, long-term loans, long-term portion of the bonds payable, deferred revenue, long-term loans, deposits, tax liabilities, etc.

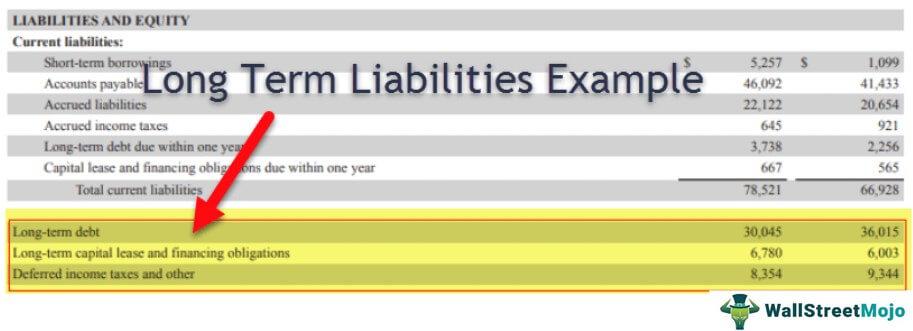

Consider the example of the American retail giant Walmart Inc. in the balance sheet excerpt above. The Long term liabilities include long term debt, long term capital lease, and financial obligations and deferred income taxes.

Most Common examples of long-term liabilities include

- Long-term debt

- Finance leases

- Deferred tax liabilities

- Pension liabilities.

We will discuss each of the examples of long term liability along with additional comments as needed.

Most Common Examples of Long-Term Liabilities

Example #1 – Long-Term Debt

Apart from the simpler concept of bank loans, long term debt also includes bonds, debentures, and notes payable. These may be issued by corporates, special purpose vehicles (SPVs), and governments. Some bonds/debentures may also be convertible to equity shares, fully or partially. The terms of such conversion shall be specified at the time of the issue.

Long-term debt may be either secured i.e., backed by collateral or unsecured.

- Bonds are typically secured i.e., backed by specific collateral assets.

- Debentures are not secured by any collateral and are generally issued for specific purposes, such as planned projects. It is generally the revenue proceeds from the specific project that is later used to repay the debenture principal. Without any collateral backing, these instruments generally have higher credit risk than bonds and other secured debt. It makes it essential to appropriately assess the financial strength and creditworthiness of the issuer. Debentures are generally issued with a longer time to maturity and at lower interest rates as compared to other types of debt.

- Notes are the same as bonds in most cases. However, their prominently distinguishable feature is the shorter maturity of treasury issues—the U.S. Treasury, for example, issues notes with maturities of 2, 3, 5, 7, and 10 years, while bonds are issued for longer terms as well.

Example #2 – Finance Lease

A lease contract is termed as a finance lease, also known as a capital lease if it fulfills any of the following capital lease criteria:

- At the end of the lease period, ownership of the leased asset is transferred to the lessee.

- The term of the lease is at least 75% of the asset’s useful life.

- The present value of lease payments is at least 90% of the asset’s market value.

- The contract allows the lessee to purchase the asset at a bargain i.e., lower than market value.

For lease contracts of over one year, the lessee records a long-term liability equaling the present value of lease obligations. A fixed asset of equivalent value is also recorded in the lessee’s balance sheet.

Example #3 – Deferred Tax Liability

Owing to the difference between accounting rules and tax laws, the pre-tax earnings on a company’s income statement may be greater than the taxable income on its tax return. It is because accounting is done on an accrual basis, whereas tax computation is on a cash basis of accounting. Such a difference leads to the creation of deferred tax liability on the company’s balance sheet.

Deferred tax liabilities are thus temporary differential amounts that the company expects to pay to tax authorities in the future. At a later date, when such tax is due for payment, the deferred tax liability is reduced by the amount of income tax expense realized. The cash account is also reduced accordingly.

Example #4 – Pension Liabilities

Pension obligations give rise to liabilities in case of defined benefit plans only, where the employer (company) promises to pay a specific amount to retired employees, based on their salaries, period of service, etc.

- The employer sets aside funds for this purpose by investing in the pension plan/trust, generally referred to as plan assets. The present value of the pension obligation is referred to as the Projected Benefit Obligation (PBO).

- When PBO exceeds the fair value of plan assets, the plan is said to be ‘underfunded,’ and such excess amount is recorded as a pension liability in the employer’s balance sheet.

- Pension liabilities are thus sensitive to several factors, such as the performance of the underlying plan assets, an increase in salaries, the discount rate used in the calculation of PBO, life expectancy, and other actuarial assumptions.

Consider the example of American pharmaceutical company Pfizer Inc. It contains Pension liabilities, in addition to debt and deferred taxes. Pfizer’s commitments under a capital lease are not significant (as mentioned in the annual report) and are thus not described separately here.

The pension liability is further detailed in the notes section (excerpt below).

Source: Pfizer Inc Filings

Conclusion

Different sources of funding are available to companies, of which long-term liabilities form an important portion. We often come across some or all of the types described above in balance sheets across industries. These are usually looked into as an integral part of financial analysis, especially for financial leverage and credit risk assessment.

It is also essential to understand the computation of such liabilities, their payment schedules, and any additional terms associated with each of them. Such details are available in the notes to accounts in annual reports.

Recommended Articles

This article has been a guide to Long-Term Liabilities Examples. Here we discuss the top 4 Examples of Long-Term Liabilities, including Long-term Debt, Financial Lease, etc. Here are the other articles in accounting that you may like –