Part of our Balance Sheet guide

What is Off-Balance Sheet Financing?

Off-balance sheet financing is the company’s practice of excluding certain liabilities and, in some cases, assets from getting reported in the balance sheet to keep the ratios such as debt-equity ratios low to ease financing at a lower rate of interest and also to avoid the violation of covenants between the lender and the borrower.

It is a liability that is not directly recorded on the company’s balance sheet. Off-balance sheet items carry enough significance because even if they are not recorded on balance sheet finance, they are still the company’s liability and should be included in the overall analysis of the company’s financial position.

How Does It Work?

Suppose ABC Manufacturers Ltd is undergoing an expansion plan and wants to purchase machinery to establish the second unit in another state. However, it does not have a financing arrangement as its balance sheet is already heavily financed. In such a case, it has two options. It can set up a joint venture with other investors or companies to establish a new unit and obtain fresh financing in the new entity’s name. On the other hand, it can also chalk out the long-term lease agreement with the equipment manufacturer for the leasing of machinery, and in this case, it need not worry about obtaining new financing. Both of the above cases are examples of Off-balance sheet financing.

What is the Purpose of Off-Balance Sheet Items?

- To maintain solvency ratios like Debt to equity ratio below a certain level and obtain funding that which the company would not have been able to obtain otherwise.

- Better solvency ratios ensure maintaining a good credit rating, allowing the company to access cheaper finance.

- It makes balance sheet finance appear leaner, which prima facie may attract investors.

Off-Balance Sheet Financing Video

Key Features

- It results in the reduction in existing assets or exclusion of assets going to be created from the balance sheet.

- There is a change in the Capital structure of the company.

- Assets and liabilities are both understated, giving a leaner impression of the balance sheet finance.

- It involves the use of creative accounting and financial instruments to achieve off-balance sheet finance.

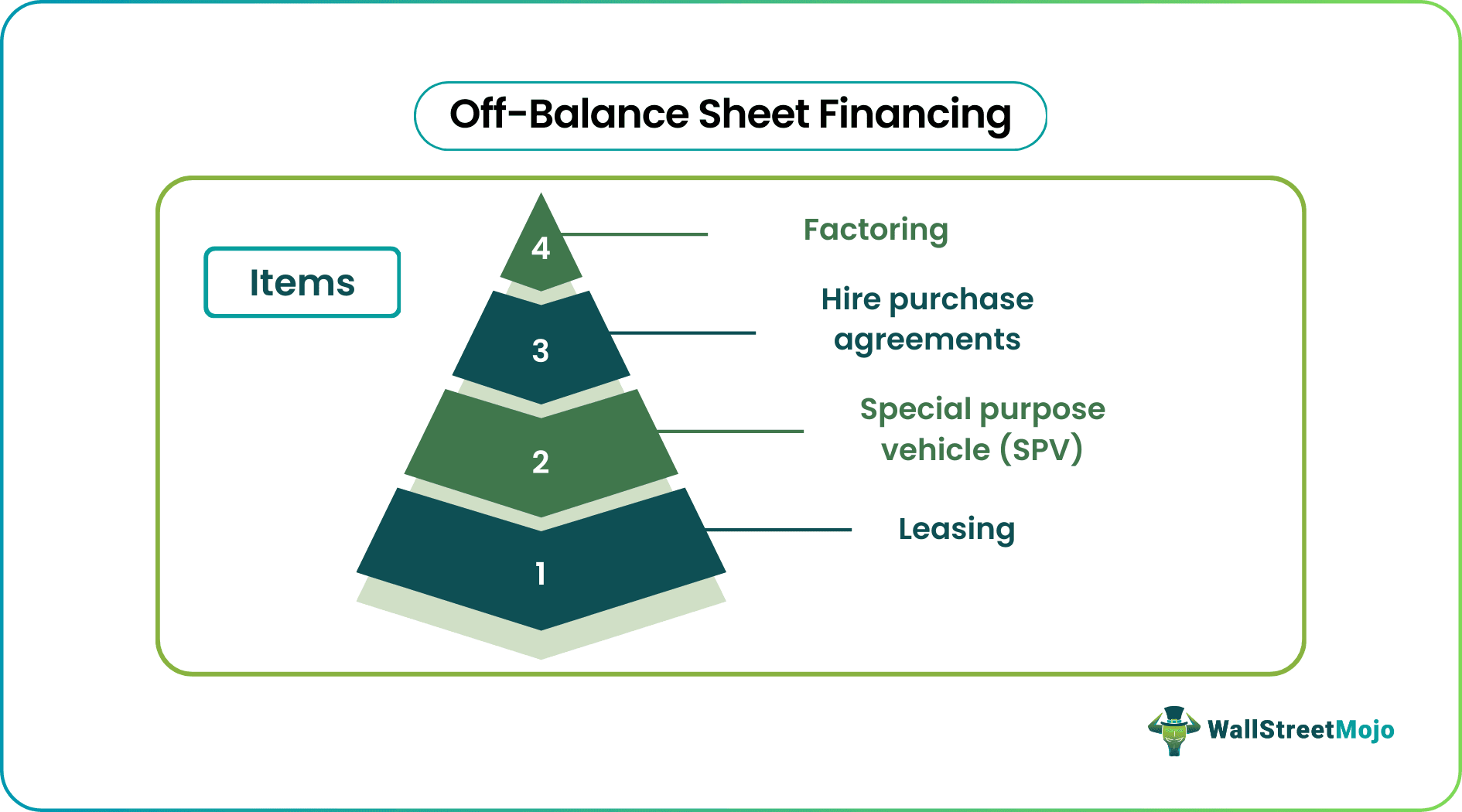

List of Off-Balance Sheet Financing Items

The following are some of the common instruments for off-balance sheet items.

#1 – Leasing

It is the oldest form of off-balance-sheet financing. Leasing an asset allows the company to avoid showing financing of the asset from its liabilities, and lease or rent is directly shown as an expense in the Profit & Loss statement.

- For the lessee, it is the source of financing as lessor bears the asset financing.

- The conventional method to acquire assets that require significant capital outlay;

- It makes it easier to upgrade technology with changing times.

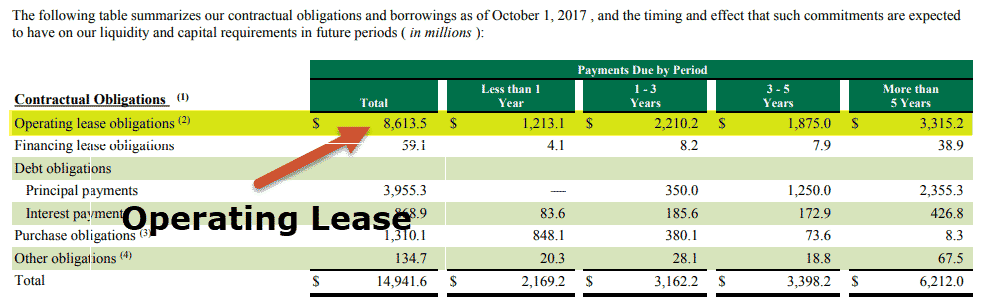

- Only Operating leases qualify as off-balance-sheet financing, and financial leases must be capitalized on the balance sheet as per the latest Indian Accounting Standards.

#2 – Special Purpose Vehicle (SPV)

Special purpose vehicles or subsidiary companies are one of the routine ways of creating off-the-balance sheet financing exposures. It was used by Enron, which is known for one of the high-profile off-balance-sheet financing exposure controversies.

- The parent company creates SPV to enter a new set of activities but wants to isolate itself from risks and liabilities from new activity.

- The parent company need not show the assets and liabilities of SPV on its balance sheet.

- The SPV acts as an independent entity and acquires its credit lines for the new business.

- Suppose the parent company fully owns SPV under accounting standards for most countries. In that case, it needs to consolidate the SPV balance sheet into its own, defeating the purpose of creating off-balance sheet finance. Therefore, companies usually create SPV through a new joint venture with another entity.

#3 – Hire Purchase Agreements

If a company cannot afford to purchase assets outright or obtain finance for the same, it can enter into a hire purchase agreement for a certain period with financiers. A financier will purchase the asset for the company, which will pay a fixed amount monthly until all the terms in the contract are fulfilled. The hirer can own the asset at the end of the hire purchase agreement.

- Under normal accounting, the asset reflects in the purchaser’s balance sheet, and the hirer need not show it in its balance sheet during the period of the hire purchase agreement.

#4 – Factoring

Under factoring, finance is obtained by selling account receivables to Banks. It is a type of credit service offered by Banks and other financial institutions to their existing clients. Banks offer immediate cash to the company after taking some cut from account receivables for offering the service.

- It is also termed as accelerating cash flows sometimes.

- There is no direct liability on the company due to factoring, but there is a sale of some of its assets.

Significance For Investors

Under accounting standards for almost all major countries, it is mandatory to fully disclose all the off-balance sheet financing items for the company for that particular year. Investors should take note of these disclosures to understand the risks associated with such transactions fully.

Recommended Articles

This article has been a guide to what is Off-Balance Sheet Financing and its definition. Here we discuss how off-balance sheet Items works and the list of items used to create them. You may learn more about Advanced Accounting here –