What Are Long Term Liabilities?

Long Term Liabilities, often referred to as Non-Current Liabilities, arise due to liabilities not due within the next 12 months from the Balance Sheet Date or the Operating Cycle of the company and mostly consist of Long term Debt.

The term ‘Liabilities’ in a company’s Balance sheet means a particular amount a company owes to someone (individual, institutions, or Companies). Or in other words, if a company borrows a certain amount or takes credit for Business Operations, it must repay it within a stipulated time frame.

Long Term Liabilities Explained

Long-term liabilities are those types of financial obligations that will take a minimum of one year to be settled. These long-term commitments are essential parts of the financial statements of the business because the investors use it, shareholders and other stakeholders of the business understand the current financial obligation and the ability of the business to meet them on time.

The term Long-term and Short-term liabilities are determined based on the time frame. Long-term liabilities that need to be repaid for more than one year (twelve months) and anything which is less than one year are called Short-term liabilities.

For example – if Company X Ltd. borrows $5 million from a bank with an interest rate of 5% per annum for eight months, then the debt would be treated as short-term liabilities. However, if the tenure becomes more than one year, it would come under ‘Long-Term Liabilities’ on the Balance Sheet.

Based on these values of long term liabilities balance sheet, the creditworthiness and financial strength of the business can be evaluated. Creditors use it to make decisions regarding the extension of credit facilities, which will be used for the growth and expansion of the business. In the balance sheet, they are listed separately, and they are considered to be long-term debts of the company.

However, sometimes, some companies plan to refinance and convert their current obligations into long term liabilities list. If such intention is there, then the company should include the current liability within the long-term liability in the balance sheet and show it for better clarity. However, such liabilities are commonly met using the profits, investment income, or liquidity obtained from new loan agreements.

List Of Long-Term Liabilities On Balance Sheet

Based on the nature of the long term liabilities balance sheet taken by a Company, here is the list of Long-term liabilities on the Balance Sheet:

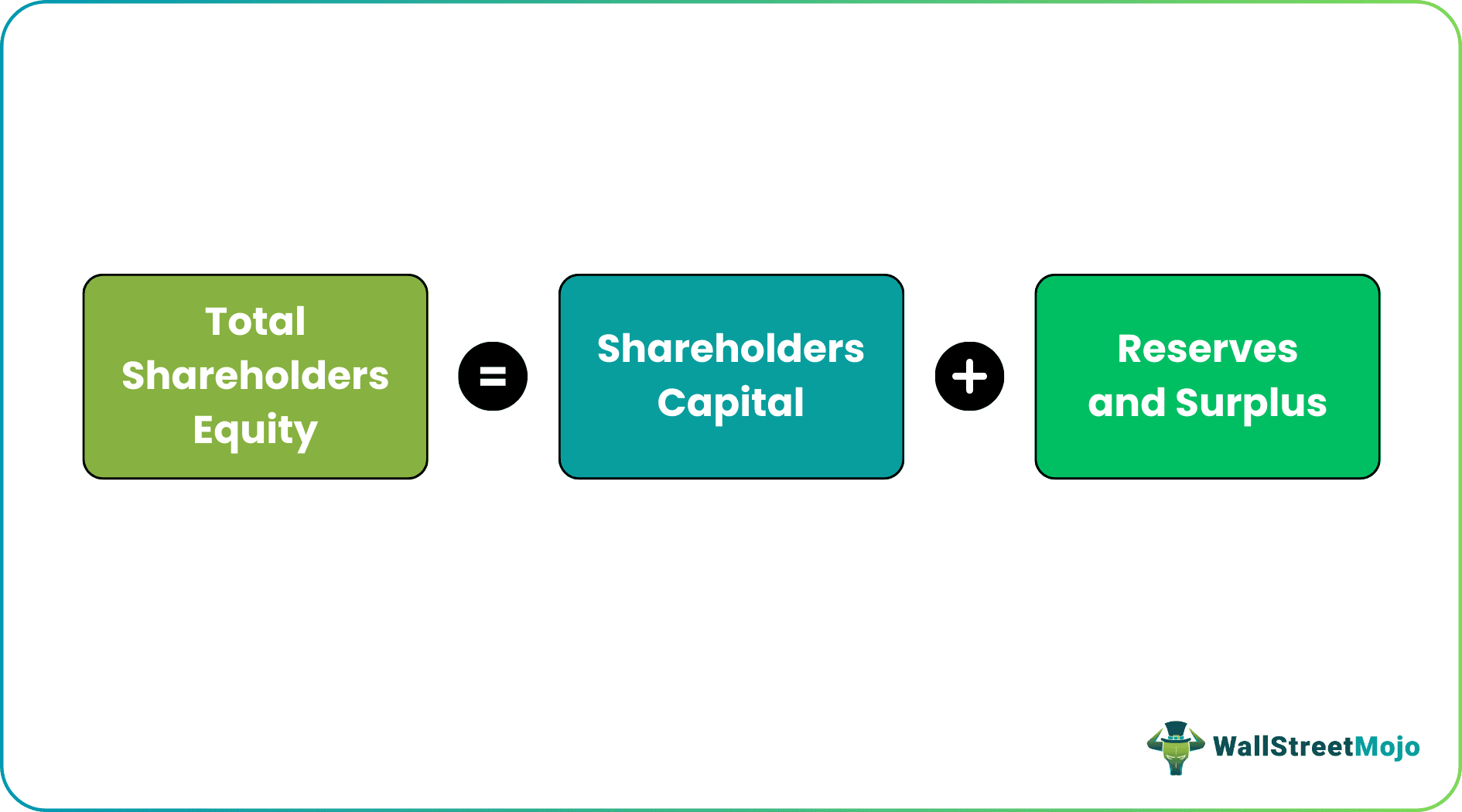

#1 – Shareholders Capital

Shareholders are the real owner of a Company and can be classified into two categories, Preference shareholders and Equity shareholders. Preference Shareholders are given preference during the distribution of profits (get the dividend if there is also a loss). In contrast, Equity shareholders get dividends only when there is a profit. On the other hand, Equity shareholders have voting rights, unlike Preference shareholders. The initial capital or the ‘Seed Financing’ required for the business comes from the Shareholder’s pocket. The total capital amount can be divided into the total number of shareholders based on their capital contributions. The risk-to-reward ratio is allocated as per the capital contribution. For example- Suppose Company A has been funded by three investors, X, Y & Z, with the capital contribution of $2000, $3000, and $5000; the profit would be shared based on 2:3:5.

Reserves & Surplus is another part of the Shareholders’ equity, which deals with the Reserves. If a Company makes constant profits, then the pile of profits at a given time would be termed ‘Reserves and Surplus.’ For example, if a Business unit delivers Net profits after tax (after dividend distributed to shareholders) for the first three years @ $11,000, $80,000, and $95,000. Then the total reserves would be $(11000+80000+95000) or $285,000 after the third Financial Year.

Thus, we can say

#2 – Long-Term Borrowings

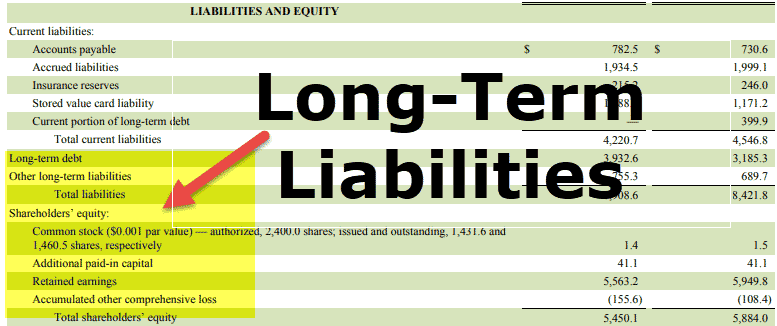

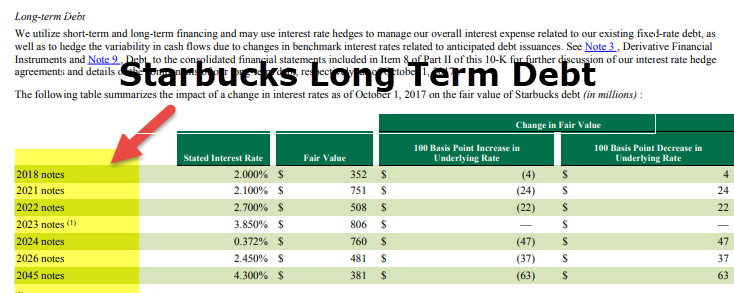

Below is the long-term liability example of Starbucks Debt.

source: Starbucks SEC Filings

Borrowings fall under long term liabilities list and are an integral part of a business; the entire capital cannot be funded only from Shareholder’s capital. Generally, high-capital intensive requires funds at different stages. Thus, to ensure smooth operations, a Business unit takes a loan from a financial institution, bank, individual, or group of individuals. A loan that is repayable after 12 months, along with interest, is known as Long-term borrowing. Types of long-term borrowings are –

- Bonds or Debentures, which bear a specific amount of fixed interests, are generally borrowed from the market bearing a fixed amount of interest repayable by the company. Bondholders are not bothered with the profitability of the company. They are obliged to get the money until the company is declared insolvent.

- Other than Bonds, Borrowings can be made from institutions or Banks (Term as a loan) with a pre-decided date. Failure to pay the loan within the stipulated time, along with interest, could force the company to pay a penalty fee. Thus, a high borrowing amount is generally a bad signal for a company, and it becomes worse if the Business cycle changes.

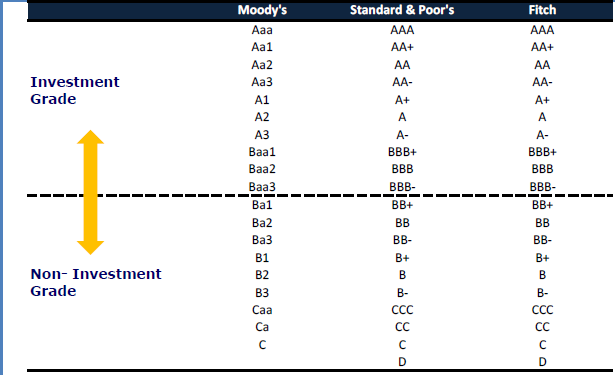

- Bonds are rated by rating agencies like Moody’s, Standard & Poors, and Fitch depending on how safe the bond is – Investment grade or non-investment grade.

#3 – Deferred-Tax Liabilities

Tax liabilities can be terms of the tax a company is obliged to pay in case of profits made. Thus, when a company pays a lesser tax on a particular financial year, the amount should be repaid in the next financial year. Till then, the liability is treated as the deferred tax, which is repayable within the next financial year.

For example, Company HR Ltd. made $20,000 in FY17-18 and paid a tax of $5000 (assuming a 25% tax rate), but later the company realized that the tax slab was 28%. So then, in this case, $600 must be paid along with next year’s tax payment.

#4 – Long-Term Provision

Provisioning a certain amount generally means allocating a certain expense or loss or bad debt concerning the future course of action by the company. The item is treated as a loss until the company accounts for the loss. For example, – Pharmaceutical companies assume certain losses regarding patent rights as all the Research & Development part is related to the approval of the patent of medicines. Similarly, lawsuit charges & Fines from pending investigations come under the same head in the Balance-sheet. For example, if a Bank expects a certain amount of loan, which is most unlikely to recover, then the Loan amount would be treated as ‘Bad Debt.’

Example

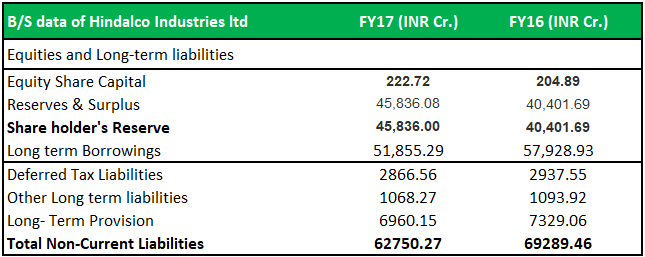

Let us understand the concept of long term liabilities accounting with the help of a suitable example.

The above example shows that the company Hindalco Industries is doing business in Aluminum extracting, and the manufacturing of Aluminum finished products has raised its equity base from INR 204.89 Cr. in FY16 to INR 222.72 Cr. In FY17. The above equity inflow results in a higher equity base, an outcome of the newly issued Equity share.

Because of the company’s profitability, the Reserves amount shot up from INR 40401.69 Cr to INR 45836 Cr. However, the Long-term Debt ratio has reduced from INR 57928.93 Cr. to INR 51855.29 Cr. which is almost 10.5 % from the previous year, and it’s a healthy sign.

Deferred Tax, Other Liabilities on the balance sheet, and Long-term Provision have, however, decreased by 2.4%, 2.23%, and 5.03%, suggesting the operations have improved on a YoY basis.

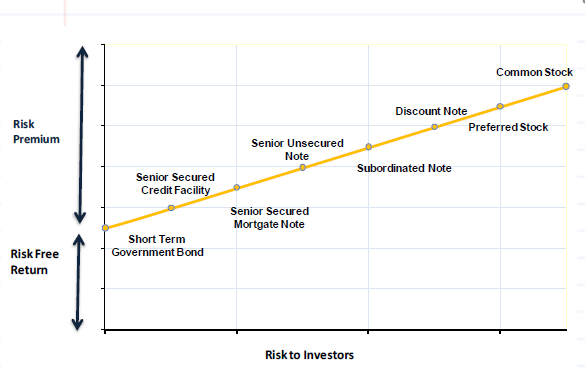

The Risk To Investors Vs Long Term Liabilities

The below graph provides us with the details of how risky these long term liabilities accounting are to the investors.

- The common stock is the riskiest to the investor, whereas short-term bonds are the least risky.

- In between comes the others like senior secured facility, senior secured notes, senior unsecured notes, subordinated notes, discount notes, and preferred stocks.

Importance

- Long-term Liabilities on the balance sheet determine the integrity of the business. If the Debt part becomes more than the equity, then it’s a reason to worry regarding the efficiency of the Business Operations. Such liabilities need to be controlled shortly.

- Higher provisioning of total long term liabilities also indicates higher losses, which are not favorable for the company. Higher expenses cause a shrink in profits. On the other hand, if a company assumes a higher provision than the actual number, then we can term the company as a ‘defensive’ one.

- Equity share capital, along with reserves and debt, determines the company’s cash flow. Purchasing assets, new branches, etc., can be funded from Equity or Debt.

Long-Term Liabilities Video

Long Term Liabilities Vs Current Liabilities

Both are two distinct types of financial obligations that any business has a t a point of time during the reporting period. But there are some important differences between them as follows:

- The total long term liabilities is planned to be met withn a time frame which can extend to more than a year, but the time frame of the latter is ideally less than a year.

- The former is also known as non-current liabilities, but the latter is also known as short-term liabilities.

- The former usually includes long term loans taken for the purpose of heavy investments in projects or for growth and expansion of the company. The latter is usually taken for meeting the day-to-day expenses of the business, like payment of bills, payment of salary, wages, purchase of stationary, etc.

- The former represent the extended form of financial commitments and obligations of the company and its business operations towards its creditors, lenders and investors. But the latter shows a portion of the ongoing operational process of the business.

- The former is from a broader prospect but the latter is from a narrower prospect.

Thus, the above are some important differences between the two topics. It is important to be able to differentiate between both so that the stakeholders can understand the current financial status of the business with clarity and make correct financial decisions.

Recommended Articles

This has been a guide to what are Long-Term Liabilities. We explain the differences with current liabilities along with a list, examples, risk & importance. Here we discuss the list of long-term liabilities, including the long-term debt, shareholders equity, long-term provision, and deferred tax liabilities, along with practical examples. You may also have a look at these articles below to learn more about accounting –