Part of our General Ledger guide

Reconciliation of Books

As we all know, Books of Accounts are the blueprints of any business. Therefore, maintaining the Books of Accounts is the key to financial management.

However, maintaining books of accounts is not enough. It is also necessary that the accounts should be accurate and complete. There are various checks and controls to ensure this, but one of the most basic and essential ways is “Reconciliation of Books.”

What is Reconciliation?

It is a process that compares two sets of records and analyses the differences between the two sets if any.

These two sets of records can be anything from the entire gamut of Books of Accounts. Generally, one set of the record is a ledger from the company’s Books itself which needs to be reconciled, and the second set of the record is obtained from internal or external sources.

e.g., comparing the bank book (internal source) vis-à-vis the bank statement (external source).

When is Reconciliation Done?

It is generally carried out before the closure of accounts. It is advisable to do it monthly to keep the books up-to-date, but they can also be done on a quarterly or annual basis.

Heavier the volume should be the frequency of reconciliation so that the reconciliation process is smoother.

They should be done annually before the Books are certified by the auditors. Most of the reconciliations are a prerequisite for audit testing purposes. Since the enactment of Sarbanes Oxley (SOX) in 2002, reconciliations have become even more critical as the compliance required has risen to a different level.

What is the period for which reconciliation is done?

One of the critical aspects to take care of while performing reconciliation is that the period for both sets of records should be the same.

In continuation with the example stated above, it is very illogical to compare bank books extracted for 01-Jan-16 to 31-Mar-16 to the bank statement for 01-Jan-16 to 30-Jun-16. There should be a common base for comparison.

Also, an essential thing to consider is that the Opening or Beginning balance should always be equal for both sets of records. In the above case, if the balances on 01-Jan-16 are not identical, this difference should first be rectified rather than the reconciliation for 01-Jan-16 to 31-Mar-16.

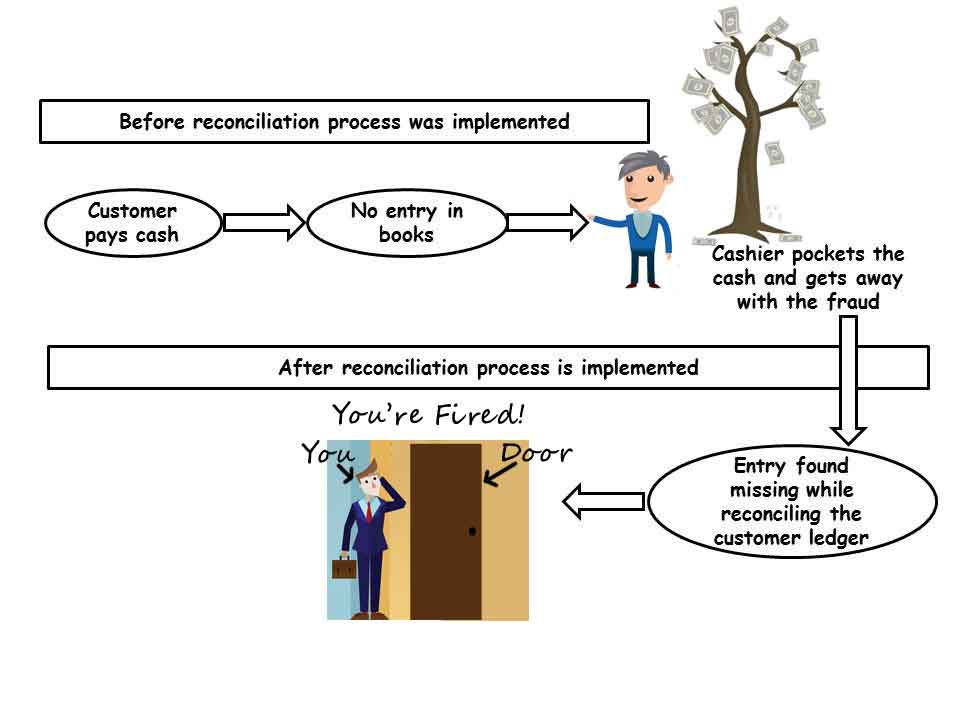

Detect fraud

- It is easy to manipulate books of accounts. One way of detecting fraud is through reconciliation. Let us understand this with an example.

- The cashier of ABC Corporation is committing fraud by not recording cash received from customers. The customer and cash ledgers are unchanged, and he can pocket the cash received.

- A simple way to detect frauds like this is to perform customer ledger reconciliation. When the customer’s ledger in the Books of ABC is compared to ABC’s ledger in the customer’s Books, the balances will not tie, and the fraud will be detected.

Ensure records are complete:

- At times, certain activities affect our books but not be routed through the accounts team and hence, may go undetected.

- A small example is a cheque deposited by a customer directly in the bank account. If the customer does not inform, the bank ledger and the customer ledger will be incomplete, leading to a misrepresentation of facts.

Ensure records are accurate:

- There are chances of human errors in the process of accounting.

- One example of human errors is the incorrect placement of digits, e.g., the Actual value of sales was Rs. 99,736, which was incorrectly recorded as Rs. 97,936.

- These can be found out while reconciling accounts. These are nothing but transposition errors, and in this case, the difference is generally divisible by 9.

Best Practices for the reconciliation process

Some of the best practice which can be adopted so that reconciliation helps achieve its purpose is as follows:

- Companies should set up a Reconciliation Process to be followed internally. It should cover the frequency, key accounts for which reconciliation is to be done, standardized formats, etc. These processes will vary depending on the volume, type of industry, high-risk areas, etc. The policy should regularly be prepared and circulated to the Finance & Accounts team.

- Segregation of duties should be followed. It means that employees recording the entries in the books of accounts should not be a part of the reconciliation process. It will ensure that one rechecks the work done by another.

- The Authority matrix for the maker-checker process should be followed. Different employees should also prepare and check reconciliation statements based on the designation. The executive can prepare the reconciliation statement, and the Manager can check the same.

- The preparer and checker should take proper sign-off so that people feel responsible enough.

- Strict timelines for the completion of reconciliations should be set to detect frauds and take timely actions.

- The scope of the internal audit should also include checking these reconciliation statements.

- The approval process should be set to pass rectification entries (if any are discovered during the reconciliation process) to correct accounts. It will ensure that middle and upper management is updated from time to time.

- Supporting documents (such as Bank statements, Customer ledgers, etc.) should form a part of the Reconciliation Statement on which sign-off is obtained.

What does a reconciliation statement look like?

A reconciliation statement should be as simple as possible. It should include necessary details such as which ledger is being reconciled, the period of reconciliation, when the reconciliation is prepared, who has prepared, checked, approved, etc.

The following is a simple format of the reconciliation statement:

| ABC Co. | |||

| Bank Reconciliation Statement as on 31-Mar-16 | |||

| Bank Account No. 00000xxxxxx | |||

| Balance as per Books of Accounts on 31-Mar-16 | xxx | ||

| Add: | Adjustment 1 | xxx | |

| Adjustment 2 | xxx | ||

| Adjustment 3 | xxx | xxx | |

| Less: | Adjustment 4 | xxx | |

| Adjustment 5 | xxx | xxx | |

| Adjustment 6 | |||

| Balance as per Bank Statement on 31-Mar-16 | xxx | ||

| Prepared By: Accountant | |||

| Checked By: Manager | |||

| Verified By: Finance Controller |

Both sets can be taken as the base, and adjustments should be added or subtracted, thereby arriving at the balancing figure.

In the above format, the Bank book is taken as the base. However, if the Bank Statement is considered the base, all the adjustments will be reversed. The following two cases will help to understand this better:

Case A – Taking the Bank Book as the base

| Balance as per Books of Accounts on 31-Mar-16 | 9,700 | ||

| Add: | Cheques issued but not deposited | 10,000 | |

| Bank Interested credited by Bank | 75 | 10,075 | |

| Less: | Bank Charges not recorded | 175 | 175 |

| Balance as per Bank Statement on 31-Mar-16 | 19,600 |

Case B – Taking the Bank Statement as the base

| Balance as per Bank Statement on 31-Mar-16 | 19,600 | ||

| Add: | Bank Charges not recorded | 175 | 175 |

| Less: | Cheques issued but not deposited | 10,000 | 175 |

| Bank Interested credited by Bank | 75 | 10,075 | |

| Balance as per Books of Accounts on 31-Mar-16 | 9,700 |

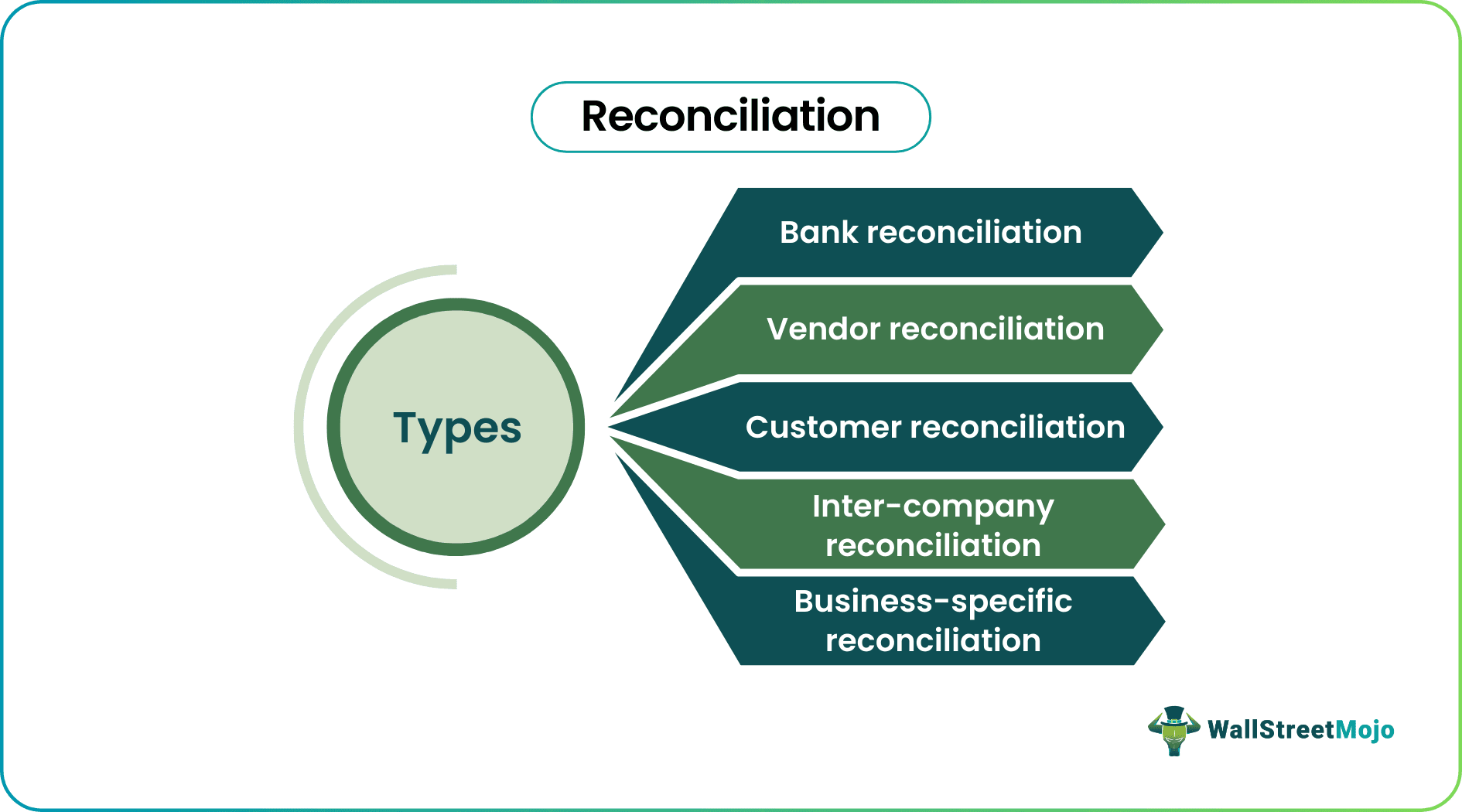

What are the types of reconciliations?

Basic reconciliation statements which are essential and prepared in day-to-day business accounting:

- Bank reconciliation

- Vendor reconciliation

- Customer reconciliation

- Inter-company reconciliation

- Business-specific reconciliation

We will discuss each of these statements in detail:

#1 – Bank reconciliation

A bank reconciliation statement is prepared concerning actual transactions reflected in the bank statement vis-à-vis transactions recorded in our bank book.

Some of the reasons for the difference between the bank book and bank statement are:

- Cheque issued to a vendor but presented at a later date

(At times, some cheques appear in the bank statement, which is very old. They are stale and cannot even be deposited anymore. Therefore, it is better to write them off and keep the Bank Book clear.)

- The amount deposited by a customer directly in our bank account

- Bank interest credited by the bank

- Bank charges debited by the bank

- Bank errors (Although rare, mistakes can happen by data entry errors are also possible by the bank)

All payment and receipt-related activities are tracked through the bank book. Therefore, reconciling it helps to keep it updated.

To make our lives easier, most accounting ERPs have built-in features that help extract the bank reconciliation statement directly.

The basic concept used in these ERPs is recording each transaction’s “bank date.” A bank date is when the transaction is reflected in the bank statement. ERP extracts a report based on the “Document Date” vis-à-vis “Bank Date.”

#2 – Vendor reconciliation

A vendor reconciliation statement is prepared to make sure that the accounting entries passed in the vendor’s books are in line with the accounting entries passed in our books.

Reasons for deviations are as follows:

- The vendor may not book purchase returns booked by us.

- Cheques issued by us may not be reflected in their books. It generally happens when the check is misplaced or lost in transit.

- Goods-in-transit are not recorded by us but recorded by the vendor;

#3 – Customer reconciliation

A customer reconciliation statement is very similar to vendor reconciliation. It is prepared to check if the customer’s books sync with our books. Most corporations treat customer reconciliation as a priority over vendor reconciliation. It is because money is receivable from customers, and it is always better to reconcile so that the payments are not pending because of some issues with accounting entries.

Reasons for deviations are as follows:

- Returns booked by customers are not appearing in our books.

- Taxes deducted by the customer are not accounted for in our books.

- Goods-in-transit is recorded as the sale in our ledger.

- Payments directly transferred to our bank account are not recorded.

A good practice is to perform monthly reconciliations of customers on a rotational basis. So, for example, let us say that a corporation has 100 odd customers, and reconciliations of around 10-15 customer ledgers should be done every month.

Also, once both parties complete and certify the reconciliation, a balance confirmation certificate for the given period can be issued. It will ensure that the opening balances need not be rechecked. It also helps to resolve disputes.

#4 – Inter-company reconciliation

Group companies (Holding, subsidiary, etc.) have to prepare consolidated Books of Accounts. These Books need to eliminate intercompany transactions such as sales from Holding Co. to its Subsidiary Co. For this, it becomes of utmost importance that their Books of Accounts are always in sync and should be reconciled regularly before the consolidation process is done.

#5 – Business specific reconciliation

Every business will have to prepare other reconciliations over and above the basic ones mentioned above. An example of this is the Costs of Goods reconciliation.

This reconciliation will not apply to the service industry as they do not hold inventory. However, it is vital for businesses that have inventory.

What is the cost of goods sold?

Cost of goods sold = Opening Stock + Purchases – Closing Stock

Cost of goods sold = Sale – Profit

Either of the two methods can arrive at the cost of goods. Both need to be the same amount. If not, a reconciliation statement should be prepared to determine the reasons for differences. Also, physical verification of the Closing Stock should be carried out, and the same should be reconciled to the Closing Stock appearing in the Books of Accounts.

Reconciliation of Books Video

Useful tips for MS Excel while performing reconciliations

- A standardized template should be prepared with all essential formulae in Excel. (Format illustrated above can be used)

- In the case of Vendor / Customer reconciliation, Invoice No. acts as a legal field that can be taken as a base for performing the Vlookup function and making the reconciliation process more straightforward. Make sure to do a paste special after using Excel Vlookup Function.

- Filter out debit and credit entries separately and reconcile them individually. Another way to separate entries is to filter them on the type, i.e., Payments, Invoices, Returns, and Other Adjustments. Reconciling these separately and then adding up the differences will prove to be helpful.

Recommended Articles

For more on General Ledger, explore these related articles from our General Ledger guide.