Reconciling Account Meaning

Reconciling an Account is a process that is followed to make sure that the account’s closing balance is correct. The general accounting rule is to pass the journal entries first, then prepare individual ledgers. The accounting ledgers reflect an ending balance tallied by the reconciliation of the accounts with other statements and documentation.

These conciliation entries are entered by companies to prevent errors in the balance sheet and check for fraud or clerical errors in the accounting process. Once the scrutiny of these accounting documents is completed, necessary corrective entries relating to reconciling accounts receivables or payables are passed to ensure the balances are correct at the time of closing.

Reconciling Account Explained

Reconciling account refers to the corrective entries passed to ensure the closing balance of accounts are free of any clerical errors and any chances of fraud are eliminated. In the double entry system of bookkeeping, each transaction must be passed both on debit and credit side.

It is not limited for companies. In fact, individuals can reconcile their own bills and credit card statements. Once they have checked their accounts for any discrepancies, they can pass a reconciling accounts payable to ensure they have the correct balance in their personal books of accounts.

Reconciling accounts is extremely important for businesses as it helps to create trust in the balances reflected by each account. Proper reconciliation is always advised. Storage of all essential documentation is vital in case of reconciliation. However, it is vital to understand that the documentation process or the structure of the document must remain consistent to ensure no double entries or inconsistencies in recording them occur. Despite the fact that there is no particular prescribed method for reconciliation, the Generally Accepted Accounting Principles (GAAP) requires a double-entry form of accounting. It basically means that an entry is passed both in the debit and credit account to ensure it is balanced.

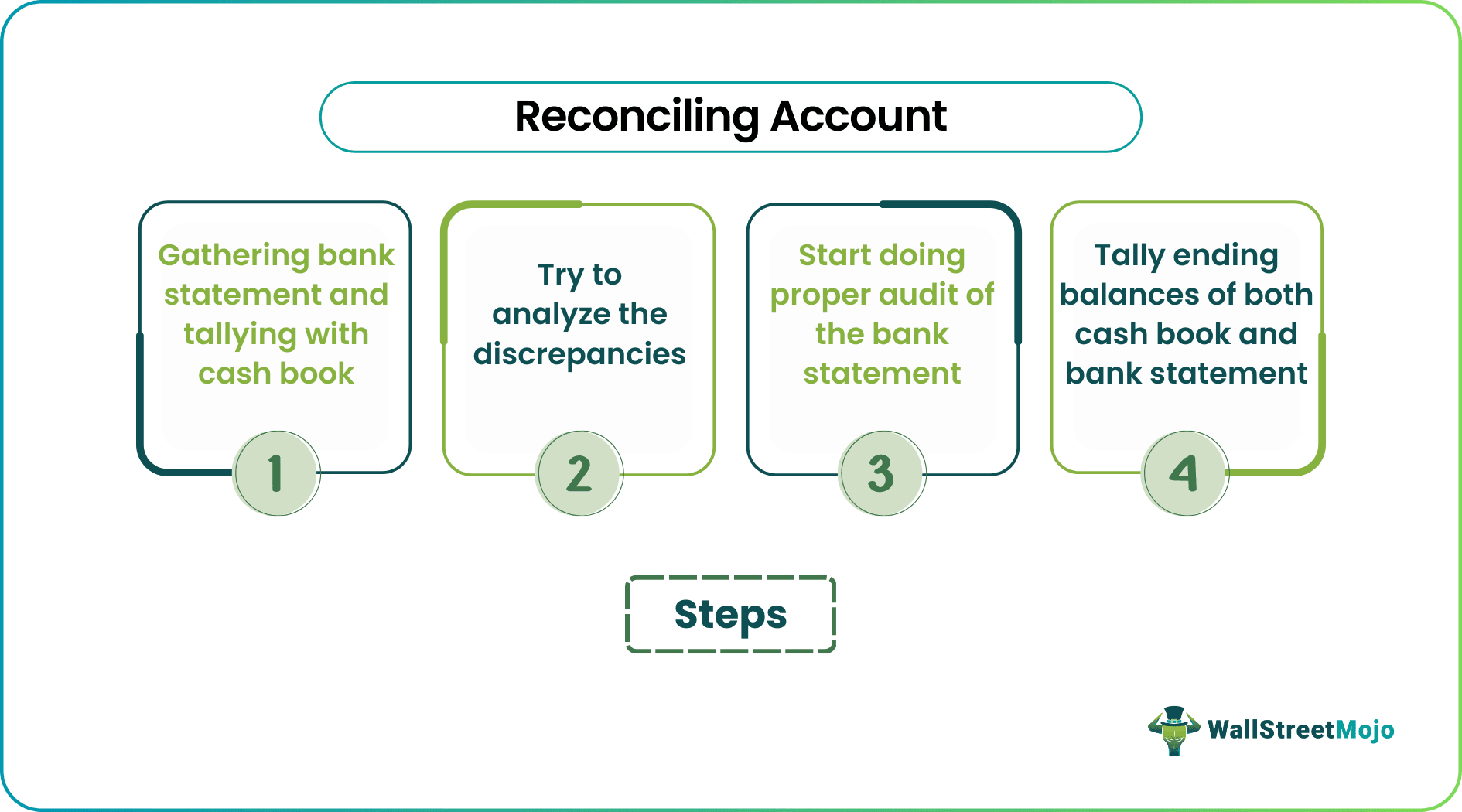

Steps

Let us understand the steps involved in passing a reconciling account payable or receivable account through the step-by-step guide provided below.

Step #1 – Gathering Bank Statement and Tallying with Cash Book

Cash Book is the internal record keeping that all businesses maintain to keep a record of all the monetary transactions. Therefore, it would be best if you started tallying both accounts. If you see that there is any transaction that is present in the Bank Statement but it is not there in the cash book, then highlight that transaction. See if all the transactions have a confirming receipt, such as an Invoice. The ending balance of cash book and bank statement should match.

Step #2 – Now Try to Analyze the Discrepancies

Go through all the discrepancies that arrived, and if they are valid, then add them to separate books. If you see that the bank statement shows a lesser balance than the Cash Book, try to find the reasons. It could be that the bank has deducted certain current account charges, ATM withdrawal charges, etc. If those charges are not included in the cash book, then include them. If you have received interest from a bank due to capital and that interest is not reflected in your cash book, then include that interest.

Step #3 – Start Doing Proper Audit of the Bank Statement

At times, the bank may wrongly charge you with some fee. Hence, this kind of error should be communicated to the bank immediately, and a proper note should be maintained. Proper follow-ups should be maintained with the bank until and unless the error resolves.

Step #4 – Tally Ending Balances of Both Cash Book and Bank Statement

It is the most crucial step. The final balances of the Cashbook and Bank Statement should tally as all necessary adjustments are already made. After this, a bank reconciliation statement is formulated, explaining the reason for the discrepancy between the two books.

Types

Reconciling can be done on any account. Every ledger accounts should be reconciled from source to make the balance trustworthy. Once the irregularities are detected, they must be treated with the corresponding reconciling account receivable or payable.

#1 – Bank Reconciliation

It is where you reconcile the internal cash book with the bank statement to make sure that the cash transactions are correctly recorded without errors.

#2 – Creditors Account Reconciliation

All the transactions under Accounts Payable are systematically tallied with statements received from creditors, and the final balance is tallied.

#3 – Debtors Account Reconciliation

All the debtors’ statements are tallied with accounts receivable, and discrepancies are resolved.

How to Reconcile?

As mentioned before, there is no standard operating protocols in this regard. However, let us discuss the two major ways accountants follow to ensure the balances are corrected for errors or potential frauds through the explanation below.

#1 – Documentation Review

This method is very popular. Here each recorded transaction is tallied by proper documentation. Say you are reconciling Accounts Payable, then each transaction will be tallied by appropriate invoices, which will check whether the transactions are correct. Missing transactions are also identified this way, i.e., if there is an invoice, and it is not recorded in the books.

#2 – Analytical Review

This method is more of an estimation. Account balances of prior periods are checked, and an estimate is done for the current year. If the account balance is not reflecting as per prediction, then further analysis is done. It is helpful when reconciling depreciation accounts. Depreciation is more or less the same each year. So if any movement is observed compared to the previous year, then the analysis is done.

Example

Let us understand the concept with the help of an example that shall give us a practical overview of the concept and its related factors.

Mr. X is preparing its balance sheet and is doing the reconciliation of each account. He is currently working on Accounts payable. How will he reconcile it?

Solution

The accounts payable account consists of all the pending payments for Mr. X. So whatever Mr. X bought on credit will reflect in this account. Say there are five entries in this account. The total balance of the account is $10,000. So Mr. X owes $10,000 to his suppliers. As Mr. X is maintaining an account for Accounts Payable, thus the suppliers are also maintaining an Accounts Receivable account.

Mr. X will ask for the final customized bill from each supplier and check whether the amount adds up to $10,000. If there is any discrepancy, that the supplier has added extra payment, then Mr. X should immediately contact them and get it fixed. So once the reconciliation is done. Then the balance of Accounts payable can be trusted.

Importance

Let us understand why passing reconciling account payable or receivable entries might help a company to maintain a foolproof documentation of its accounts through the points below.

- Every business maintains internal accounts. Hence, after the end of the period, the balances of the accounts portray a picture. Say the Accounts receivable account shows that $5,000 is receivable.

- If the company has not done reconciliation, they may start operating, thinking they will receive $5,000. At the same time, reconciliation found that the correct amount is $3,000.

- Therefore, reconciliation helps to eradicate uncertainty. Once reconciliation is done, the account balances can be trusted.

Recommended Articles

This article has been a guide to Reconciling Account and its meaning. Here we explain its examples, steps, importance, and how to reconcile an account in detail. You may refer to the following articles to learn more about finance –