Part of our Accounts Payable & Receivable guide

What Is Reconciliation?

Reconciliation is the practice of matching balances in accounts to find any financial inconsistencies, discrepancies, omissions, and even frauds. Every transaction is recorded in two accounts (debit in one and credit in another) in the books of accounts. Therefore reconciliation at the end of any accounting period includes matching balances and making sure that the debits (credits) from one account for one transaction are the same as the credit (debits) to another account for the same transaction.

Reconciliation can also be done to match balances between internal and external accounts. For example, a company might reconcile bank transactions recorded on its books and those recorded at the bank’s end to figure out mismatches. On a personal level, someone can keep track of their credit card spending and match it with the bank statement to understand the account differences.

Reconciliation Example

- Assuming a company reconciles bank transactions in its books with the bank statement. The company is doing this exercise at the end of the month. It found out that a cheque issued on the 31st of the month had not been debited from its balance at the bank, and the bank deducted certain charges from the balance, which were not recorded in the company’s books.

- Here, the balances in the company’s books and the bank’s book will not match, and entries have to be done/corrected to reflect the right balances in the accounts. The company will recognize the bank charges on its books, and the bank balance will be adjusted to reflect the accurate picture in the accounts.

Process of Reconciliation

The process of general reconciliation is as follows:

- Compare one Account Balance with the Other.

The debits and credits are matched to ensure that the balances match in this first step. For example, when a business pays rent, it debits the rent account and credits the cash or rent payable account. At the reconciliation date, all the debits in rent should match the credits in the cash account and rent payable account related to the rent expense.

- Check Entries in both Accounts

If a mismatch is found in the first step, the accountant needs to check the account transaction by transaction to figure out which entries are causing the mismatch. The differences could mainly arise due to typing errors, debiting instead of crediting accounts, passing entries in the wrong accounts, not recording entries in one account, etc.

- Correct the Incorrect Entries

Once the accountant figures out which entries are causing the mismatch, those entries can then be analyzed and corrected to reflect the right balances.

- Balance the Accounts Again

Once the corrections are done, one needs to check for mismatches in final balances again for a thorough check. As a business can undertake an enormous number of transactions in a period, the reconciliation process is usually not possible manually. It is usually done using accounting software that throws out errors for scrutiny by the accountants.

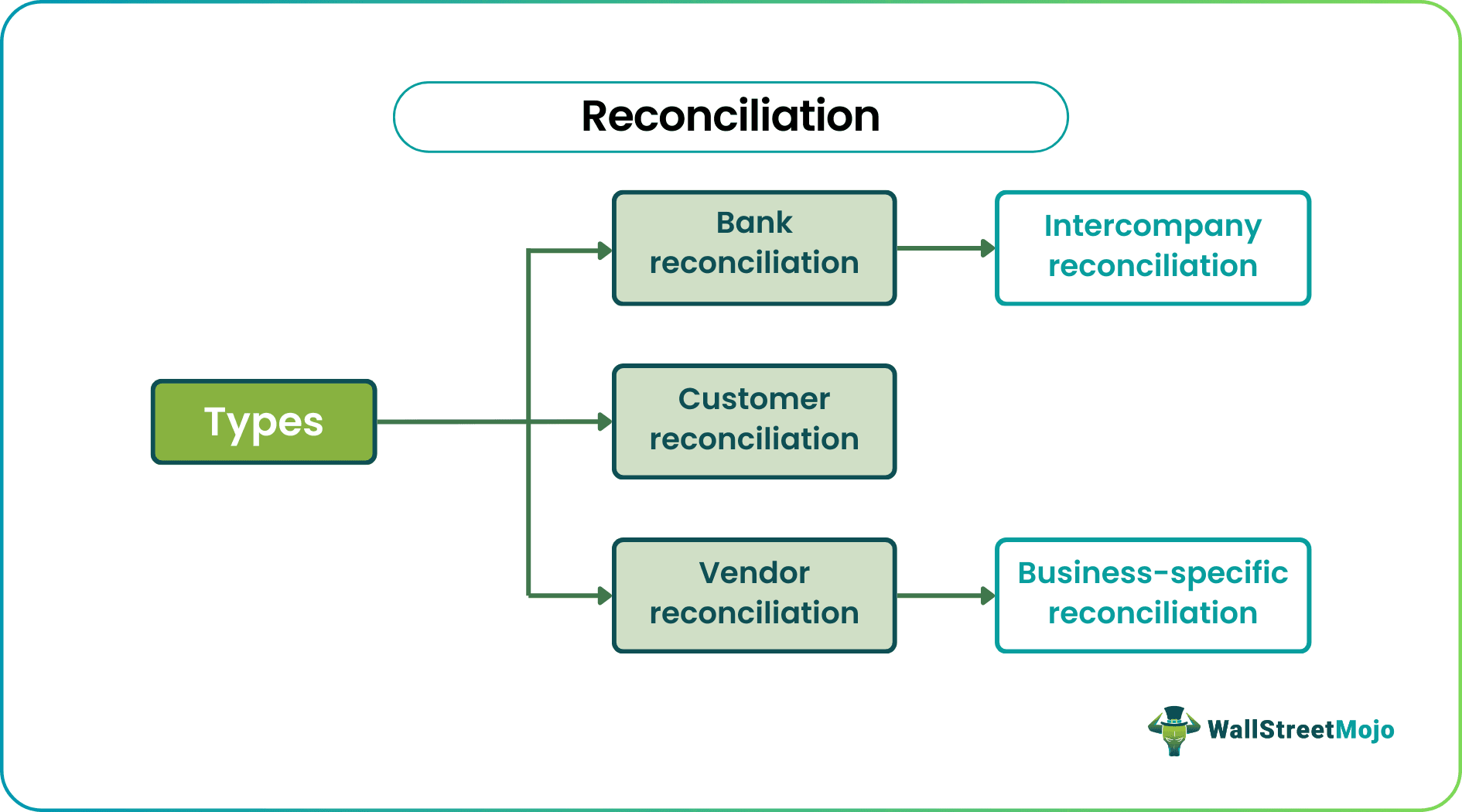

Types of Reconciliation

There are five major types of reconciliation:

- #1 – Bank Reconciliation – Transactions in bank statements are reconciled with recorded cash-related transactions in the company’s books.

- #2 – Customer Reconciliation – Customer balances on the company’s books match with balances in respective customers’ books.

- #3 – Vendor Reconciliation – Vendor balances on the company’s books are matched with the balance of the respective vendors’ books.

- #4 – Intercompany Reconciliation – Balances on the company books towards a subsidiary are reconciled with the balances towards parents in the subsidiary’s books

- #5 – Business-Specific Reconciliation – Reconciliations are specific to the nature of the company’s business activity.

Reconciliation Methods

Reconciliation can be done using two methods as described below:

#1 – Document Review

This is a formal process of reconciliation and is widely followed. Under this method, all the accounts are checked to ensure that the recorded and spent amounts are the same. This method generally uses accounting software and does an exhaustive, detailed review.

#2 – Analytics Review

In this method, balances are looked at individually and compared to what should be based on a specific parameter. The most prominent parameter could be historical trends and activity. For example, while sifting through a list of transactions, an accountant found an expense like rent is recorded to be ten times what it was in the previous years. This will call for closer scrutiny of accounts.

Advantages

- Reconciliation helps find inaccurate accounting entries, including inappropriate treatments of accounting items

- It helps find errors of omission and commission and correct them promptly

- It helps companies avoid negative opinions from the auditors, which is a possibility if they do not get the right answers for mismatches

- It helps the companies remain in sync with the accounting practices mandated by regulatory authorities

- It helps match the transactions from its source

- It helps detect fraud within the company or in the external transactions where the company is involved

- It helps in the completion of the accounting records as it brings in the missing information and supporting documents

- It can help make better-informed business decisions, making the accounts more trustworthy and error-free.

Conclusion

- Businesses rely on the financial information presented to the leaders, so it becomes crucial for that information to be error-free. If presented with error-free information, leaders can make their decision with confidence.

- Reconciliation helps the accounting personnel to weed out any errors from the accounts, which can then be presented to stakeholders for decision making. As stated earlier, reconciliation is a necessary process and must be followed by all the organizations, small and large.

- Organizations need to undertake reconciliation frequently, in a time-bound manner, and ensure that the people doing the reconciliation are not the same people who prepared the accounts in the first place to avoid conflict of interest.

Recommended Articles

This has been a guide to What is Reconciliation & its Definition. Here we discuss the reconciliation types, processes, methods and examples, and advantages. You can learn more about it from the following accounting articles –