What Is Closing Stock?

Closing stock or inventory is the amount that a company still has on its hand at the end of a financial period. This inventory may include products that are getting processed or are produced but not sold. On a broad level, it includes raw material, work in progress, and finished goods—the units of closing stock help in determining the total amount.

However, for a larger business, this is often impossible. Improvements in inventory management software and other technologies are helping curb this problem. Irrespective of the size of the organization, the precise documentation of the cost of acquiring raw materials and the cost of production plays a significant role in closing stock calculation.

Closing Stock Explained

Closing stock represents the value of the inventory remaining at the end of an accounting period, usually a fiscal year. The impact of closing stock is seen predominantly in financial reporting and impacts the balance sheet and income statement of a company.

The closing stock equation is essentially the cost of goods that a business still has in its possession or has not sold yet. It includes various items, right from raw materials to finished products to be distributed. Calculating the value of the total inventory remaining in the possession of the company requires a meticulous approach.

The valuation of closing stock significantly depends on the accounting method. The major types are FIFO (First In, First Out), LIFO (Last In, First Out), or weighted average. The choice of the method heavily depends on the nature of the product and related factors.

The impact of this value not only impacts a company’s balance sheet but also the income statement. It affects the cost of goods sold (COGS), a pivotal figure that has a direct impact on the company’s gross profit.

Therefore, closing stock refers to the financial value of the inventory of a company that remains unsold at the end of a financial year. The application of acquiring raw materials and accounting for production costs play an important role in accurately arriving at the precise value of inventory.

Formula

Below is the formula for closing stock calculation:

Closing Stock Formula (Ending) = Opening Stock + Purchases – Cost of Goods Sold.

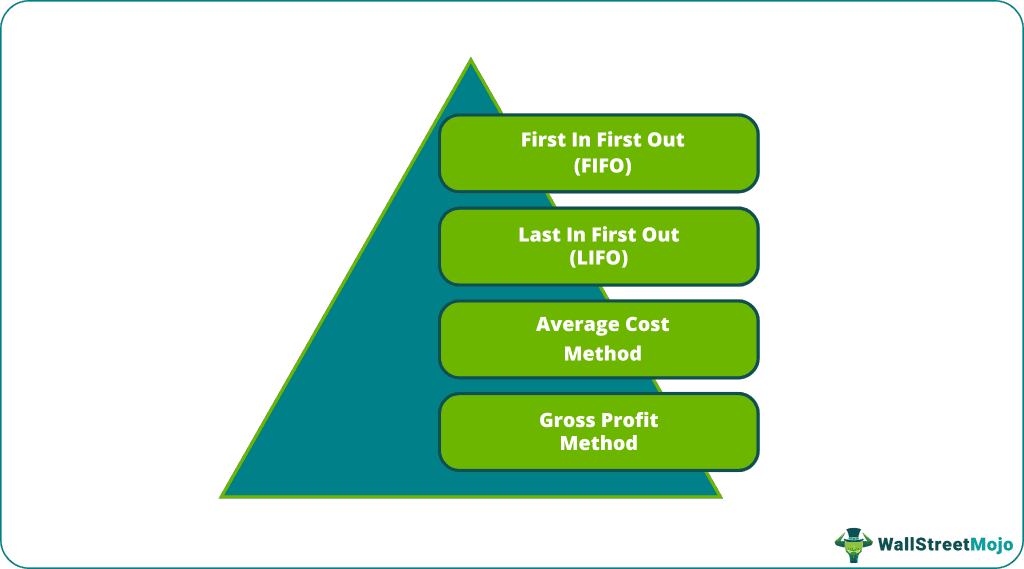

Methods

The method which company decides to use for pricing its closing stock will have a huge impact on its balance sheet and also on the income statement.

The top 4 most common methods to calculate closing stock equations are as follows –

#1 First in first out (FIFO)

FIFO inventory method assumes inventory which is brought first will be sold first, and the latest and the newest inventory is kept unsold. It means that the cost of older inventory is assigned to the cost of goods sold and the cost of the newer inventory is assigned to ending inventory

FIFO Example

- Beginning Inventory – 10 units @ $5 per unit

- Purchase – 140 units @ $6 per unit

- Sale – 100 units @ $5 per unit

Ending inventory – 10 + 140 – 100 = 50

Ending inventory amount ($) – 50 * $6 = $300

#2 Last in first out (LIFO)

LIFO Inventory Method assumes that the last item purchased will be sold off first. This method can be used for products which are not perishable or can be obsolete

LIFO Example

- Beginning Inventory – 10 units @ $5 per unit

- Purchase – 140 units @ $6 per unit

- Sale – 100 units @ $5 per unit

Ending Inventory – 40 + 10 = 50

Ending inventory amount ($) – 40 * $6 + 10 * $5 = $240 + $50 = $290

#3 Average cost method

Under this method, the weighted average cost is calculated for the closing stock. It is calculated as – cost of goods in inventory/total units

Average Cost Example

- Beginning Inventory – 10 units @ $5 per unit

- Purchase – 140 units @ $6 per unit

- Sale – 100 units @ $5 per unit

Weighted average cost per unit – (10 * 5 + 140 * 6)/150 = $5.9

Closing stock amount ($) – 50 * $5.9 = $295

#4 Gross profit method

Gross Profit method is also used to estimate the amount of closing stock.

- Step 1 – Add the cost of beginning inventory. The cost of purchases we will arrive at the cost of goods available for sale.

- Step 2 – Multiply (1 – expected gross profit) with sales to arrive at the cost of goods sold

- Step 3 – Calculate Closing Stock – To arrive at this amount, we will have to subtract the estimated cost of goods in step two from the cost of goods available for sale in step one.

Gross Profit Method Example

- Beginning Inventory – 10 units @ $5 per unit

- Purchase – 140 units @ $6 per unit

- Sale – 100 units @ $5 per unit

- Cost of Goods Available for Sale = 10 x 50 + 140 x 6 = 940

- Expected Profit margin = 40%

Sales = 100 x 5 = 500

Cost of Goods Sold = 500 x (1-40%) = 300

Closing Stock ($) = 940 – 300 = 640

The drawback of this method is that the estimation of gross profit in step 2, base on the historical estimate, which may not necessarily be the case in the future. Also, if there are any inventory losses in that period are higher or lower than the historical rates, it can lead to an inappropriate amount of closing inventory.

Impact of Pricing Method

The method by which a company decides to price its inflation affects its financial position and profits. If the company decides to use LIFO, then the cost of goods sold will be higher (assuming inflation is increasing), which reduces the gross profit and thus reduces the taxes. It is one of the vital reasons company’s prefer LIFO accounting over FIFO. One more valid reason is that on using FIFO, the amount of closing stock in the balance sheet will be higher in comparison to FIFO.

Ratios are also affected by the method in which inventory is used. The current ratio calculated as current assets/ current liabilities will be higher when FIFO is used. Ending stock will increase the number of Current Assets. On the other hand, the inventory turnover ratio calculated as Sales / Average inventory will be lower if FIFO is used.

Difference Between Opening Stock and Closing Stock

Let us understand the differences between closing and opening stock through the comparison below.

Closing Stock

- It refers to the unsold inventory at the end of an accounting period, usually a fiscal year.

- It denotes the inventory that a business has in possession but has not managed to sell by the end of an accounting period.

- The value of closing stock calculation impacts the calculation of COGS as well. Therefore, it has a direct impact on the gross profit in the income statement of a company.

- It is determined by the value of the inventory at the end of the current period while considering the cost of acquisition and production and the type of accounting method chosen by the company.

Opening Stock

- Opening stock is the value of inventory a business has in its possession at the beginning of a specific accounting period.

- It shows the value carried over from the previous accounting period. It serves as the starting point for calculating different financial metrics.

- It impacts the COGS and, therefore, the income statement of the current period as well.

- The calculation is determined primarily by the closing inventory of the previous or preceding period. However, adjustments with respect to quantity of valuation of inventory are made.

Recommended Articles

This article has been a guide to What is Closing Stock? Here we look at its formula, the top 4 methods to calculate closing stock (LIFO, FIFO, Average Cost, Profit Margin) along with its impact on the financial statements. You may learn more about accounting basics from the following articles –