Part of our Accounts Payable & Receivable guide

Bank Reconciliation Examples

Bank reconciliation is done by bank customers, totally their records and their respective bank’s statements. As the bank provides its statement periodically (generally monthly, but sometimes more frequently if requested upon charge), there may be some differences between customers’ books of accounts and those of the bank, which generates the need for reconciliation.

Bank reconciliation examples can be useful for understanding what can be the key factors in various instances that require such reconciliation. There are innumerable reasons which can cause breaks during such reconciliation. We shall see some basic and practical examples of bank reconciliation –

Top 6 Examples of Bank Reconciliation Statement

The following are some bank reconciliation examples to help you understand the topic better.

Example #1

ABC Corp holds an account with Citizens Bank. On December 31st, 2016, the bank closed its records for ABC Corp, having an ending balance of $180,000, while the company closed with $170,000. The company wishes to analyze the difference of $10,000 when they receive the bank’s statement next month.

Analysis

Below are the company’s income/expenses (at a broader level) for December 2016:

| Description | Amount |

|---|---|

| Opening Balance | $150,000 |

| Amount received from clients | $130,000 |

| Expenses paid for client services | ($100,000) |

| Salaries Payable accrued | ($20,000) |

| Cash to be received (accounts receivables) | $10,000 |

| Closing Balance | $170,000 |

Below is the record in Bank’s statements:

| Description | Amount |

|---|---|

| Opening Balance | $150,000 |

| Account Credits | $130,000 |

| Account Debits | ($100,000) |

| Closing Balance | $180,000 |

Hence it is determined that the provisions made for salaries to be paid and accounts receivables cannot be reflected by the bank statements as these are transactions yet to be made.

Example #2

Suppose on March 31st, 2018, Neeta paid her office rent for April 2018, amounting to $2,000. She made the payment by check, which was settled on April 2nd, 2018. When the bank statement was reconciled for March 2018, it was found that the Ending Balance in Neeta’s accounts was $2,000 short compared to that in the bank statement.

Analysis

Neeta made a payment of $2,000 for the office rent on March 31st, which was recorded in her book of accounts in the same month. However, as the payment was such that the actual settlement was made in the next month, the bank could not record that transaction. Hence it was showing a break in reconciliation.

Example #3

Jane made the following transactions in June from her savings bank account:

| Description | Amount |

|---|---|

| Opening Balance | $20,000 |

| Monthly Travel Expenses | ($2,000) |

| Personal Expenses | ($3,000) |

| Investment on Fixed Deposits | ($5,000) |

| Food Expenses | ($1,500) |

| Adhoc income from miscellaneous services | $2,000 |

| Closing Balance | $10,500 |

However, when the bank statement was received, it was found that the Closing Balance was $10,450. Jane wants to analyze the difference between her records and the bank statement.

Analysis

After careful reconciliation was made between the two statements (Jane’s and that of the bank), it was found that $50.00 was charged to Jane as a fee by the bank. Upon further investigation, Jane realized that she had ordered a checkbook and a new Debit Card for her account in June, for which the bank charged her $50.00.

Thus, bank fees can be a major factor that may cause a break between the customer’s and the bank’s books of accounts.

Example #4

John purchases a long-term note from Bank A, which pays semi-annual interest at 4% at the end of every June and December. In June, John closed his book of accounts, with Ending Balance being $35,000. However, when John received his bank statement, it reflected a closing balance of $35,500. Can you guess what can be the reason for such a difference?

Analysis

The difference is clearly due to interest accrued on the note purchased by John. As the interest paid is semi-annual, which is paid out at the end of June and December, the monthly statement for June included this accrued interest. The amount would be calculated based on the Principal on the note.

Example #5

On July 31st, 2018, Mr. Alex George closed his books of savings accounts with an ending balance of $4,500, which was estimated in his bank account. However, when he received the bank statement, to his surprise, he was charged $50.00, and his closing balance was $4,450.

Analysis

Mr. Alex approached his bank, and he was guided by the fact that his account had non-sufficient funds for July. However, after further analysis, he found out that the requirements for the minimum balance in the account had changed during this month, raising it to $5,000. Therefore, due to an insufficient balance in his account, Mr. Alex was charged $50.00.

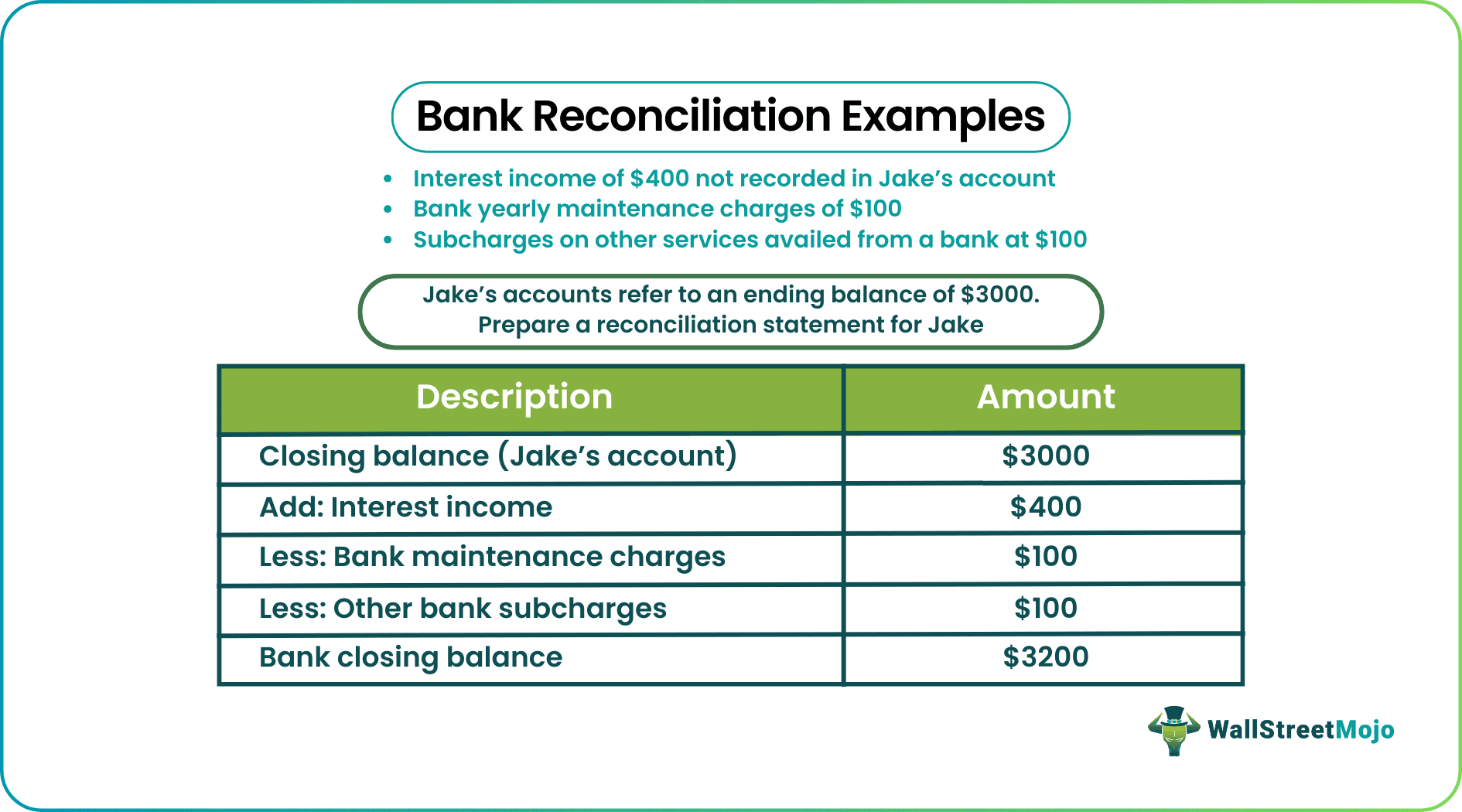

Example #6

Jake received his bank statement, which has the following differences from his accounts:

- Interest income of $400 not recorded in Jake’s accounts

- Bank yearly maintenance charges of $100

- Surcharges on other services availed from a bank at $100

Jake’s accounts refer to an ending balance of $3,000. Prepare a reconciliation statement for Jake.

Solution

A reconciliation statement would include the below:

| Description | Amount |

|---|---|

| Closing Balance (Jake’s Account) | $3,000 |

| Add: Interest Income | $400 |

| Less: Bank maintenance charges | $100 |

| Less: Other bank surcharges | $100 |

| Bank Closing Balance | $3,200 |

The above bank reconciliation examples explain how timing differences, outstanding transactions, bank charges, and accrued interest can affect the reconciliation process in real-world scenarios.

Conclusion

Differences between a bank statement and a company’s accounting records may result in higher or lower ending balances until they are reconciled. As these bank reconciliation examples demonstrate, various factors can create differences between a bank statement and a customer’s accounting records. Nevertheless, bank statements continue to serve as important documents for purposes such as KYC verification, credit assessment, and financial analysis.

Bank statements are generated and maintained by financial institutions, making them reliable records for reconciliation. In contrast, accounting records should be reviewed and reconciled regularly to identify and correct any errors or omissions.

Bank statements also play an important role in financial reporting, auditing, compliance, and decision-making. As official records maintained by financial institutions, they provide a reliable basis for reconciling transactions and assessing an individual’s or organization’s financial position.

Recommended Articles

This has been a guide to what is Bank Reconciliation Examples. Here we provide you with the top 6 examples to prepare a Bank Reconciliation Statement and a detailed explanation. You can learn more about accounting from the following articles –