Part of our Mergers & Acquisitions guide

What is a Show Stopper in M&A?

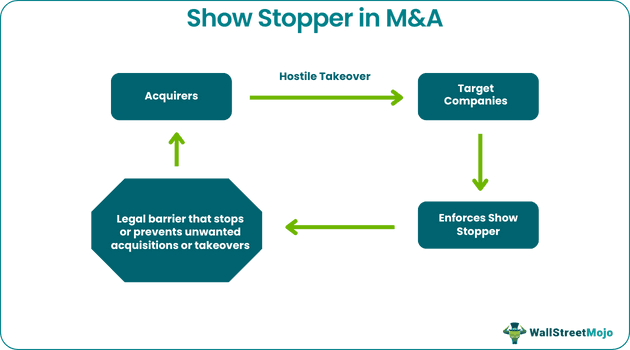

Show Stopper in M&A refers to the legal methods framed to help individuals and firms prevent or stop a takeover. In the process, the target companies, which are the most desirable acquisition targets, implement ways in which the acquirers or acquisition companies lose interest in them and drop their idea of a takeover

Acquisition or takeover is a process that can either be friendly with the consent of the board of directors of the target company or unfriendly, which is against the company’s will. Therefore, the concept of a show stopper in M&A is relevant only when the acquisition in the process is an unwanted affair.

- Show Stopper in M&A is a legal, ethical, and operational barrier adopted and implemented to prevent hostile or unfriendly takeovers.

- It is different from any killer bees defense strategy, which also comprises non-ethical ways of preventing unwilling takeovers.

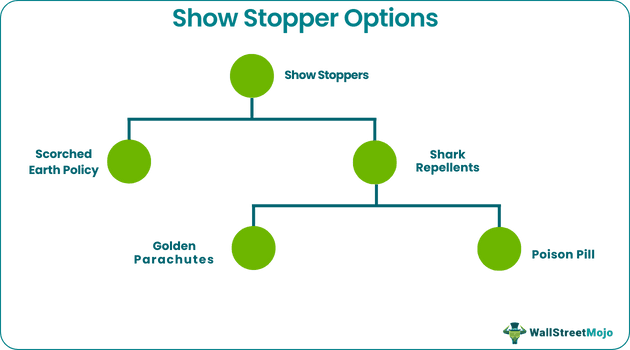

- Some of the widely used show stopper options applied in M&A are Scorched Earth Policy and Shark Repellents, which are inclusive of the former as well as Golden Parachute and Poison Pill.

- Sometimes, these show-stopping strategies backfire, making target companies lose their market value completely.

How Do Show Stoppers Work in M&A?

Show Stopper in M&A is applicable for stopping or preventing a hostile takeover. A mergers and acquisitions (M&A) process could be friendly or unfriendly, depending on how willing a firm is to be taken over. It is different from any killer bees defense strategy, a non-ethical way of preventing unfriendly takeovers.

As the name suggests, show stoppers are similar to any method or strategy that could be adopted to ensure a task or motive is not accomplished. These either restrict or put a complete full stop to the progress or evil motives of the other party, desiring to take over a firm at any cost, no matter if the latter does it willingly or unwillingly.

In the process, entities consider laws or regulations that make the possibility of a hostile takeover impossible or unnecessarily expensive. It could be in a legislative act or a court order. For instance, a target firm may convince the state legislators to pass or tweak anti-takeover laws to prevent a hostile takeover.

Strategies & Methods

When it comes to putting ethical restrictions on hostile takeovers, here are two most widely used show stopper options in M&A:

A. Scorched Earth Policy

The term has a military origin and is considered a last-ditch effort before either succumbing to the takeover or winding up the business. This option includes tactics for making the target company less attractive to the hostile bidders.

The companies utilize their liberty and sell their valuable assets to make themselves a less desirable acquisition target. They involve in deals promising to settle all debts together as soon as the takeover occurs. In addition, they borrow lots of money at higher interest voluntarily. As a result, the acquirers lose interest in the companies and call off the takeover plans.

B. Shark Repellents

These mark management’s continuous or periodic efforts for locking out hostile takeover attempts. It involves making certain amendments to the bylaws in favor of the target company when the takeover attempt is made public. The prospective takeover may or may not favor the shareholders, and one must analyze efforts on a case-to-case basis.

A shark repellent method is inclusive of Scorched Earth Policy and other widely used measures, which include:

#1 – Golden Parachutes

It involves including a provision within the executive’s contract, which will offer them substantially large compensation if a successful takeover attempts. It could be cash and stock, making it costly and less attractive to acquire the firm.

The Golden Parachutes clause predominantly protects the senior management under threat of termination if a takeover materializes. However, executives may deliberately use the clause to make it attractive for the acquirer to pursue the acquisition with a promise of massive financial compensation.

#2 – Poison Pill

Poison Pill indicates an event that significantly raises the cost of acquisitions and creates large disincentives to prevent such attempts. The target companies either take a large sum of debt, affecting the financial statements and making the firm unprofitable and overleveraged, or create employee stock ownership plans (ESOPs) which get activated only when the takeover is finalized. However, firms should be careful while implementing this strategy as it can give rise to high costs and is not necessarily in the long-term interests of the stakeholders.

Show Stopper in M&A Examples

Let us consider the following show stopper in M&A examples to understand the concept better:

Example #1

Company A attempted a hostile takeover of Company B. The former offered shares to the latter’s public shareholders at $5 per share, then traded at $2 per share on the New York Stock Exchange.

Mary, the target company’s employee, suggested a luring offer for all shareholders, i.e., a special cumulative dividend in convertible preferred stock. Accordingly, company B’s shareholders applied the flip-over strategy and purchased shares in Company A. This strategy proved successful. Firm A initiated a negotiation with firm B, given the significant shareholder ownership on both sides.

Example #2

A high-profile American investor named Ronald Perelman showed consistent interest in taking over Gillette post the acquisition of Revlon Corporation. Perelman seemed to plan a tender offer for Gillette, countered, and paid $558 million to Revlon. The latter agreed not to make any tender offer to Gillette stockholders. To make this plan effective, Gillette further paid $1.75 million to investment banking institution Drexel Burnham Lambert. In return, the investment banker ensured not to participate in any takeover involving Gillette for three years.

Limitations

Such sandbagging measures also have drawbacks and can also backfire. While making efforts to appear less attractive to the acquiring company, the target companies lose their value in the market. In some cases, the firms cannot recover the same market status again despite trying their best.

Frequently Asked Questions (FAQs)

What is a show stopper in M&A?

It refers to legal or operational barriers that help target companies prevent hostile takeovers. The target companies, in the process, make themselves appear less attractive to ensure the acquirers lose interest in them.

How effective is a show stopper in M&A?

The show stopper options, when implemented, are effective in preventing hostile takeovers. However, at the same time, these strategies make the target companies lose their market position because of sandbagging measures adopted to appear less desirable.

What are the types of Poison Pill strategies?

The poison pill strategy can either be flip-in or flip-over. In the flip-in process, the existing shareholders can buy the target companies’ shares at high discounts. On the contrary, under the flip-over strategy, the target companies’ shareholders are encouraged to buy more and more shares of the acquiring company at a discount.

Recommended Articles

This article is a guide to What is a Show Stopper in M&A and its options. We also explain its effectiveness despite its limitations along with popular examples. You may also have a look at our suggested articles: –