What Is A Wraparound Mortgage?

Wraparound mortgage in real estate or commonly called wrap, is a secondary loan facility provided by banks where a person can borrow money and buy property. It wraps around the original mortgage and provides an alternative facility to individuals who cannot access traditional loans.

A seller receives a promissory note for the amount due in a wraparound mortgage contract. It is quite a convenient system for the seller. In addition, there are fewer requirements needed in a wraparound mortgage agreement. However, there are more chances of breaches from the other party.

- Wraparound mortgages, or wraps, are secondary financing where the seller authorizes loan facility to buyers who cannot access traditional mortgages.

- The seller issues these mortgages to buyers, who then pay a down payment to them. The former then uses this amount to repay their original loan.

- The concept prevailed in the late 1970s and the initial 1980s in the United States. It usually occurs during the inflationary phase.

- If parties fail to comply with the agreement, the lender can foreclose, sell the property and recover the amount.

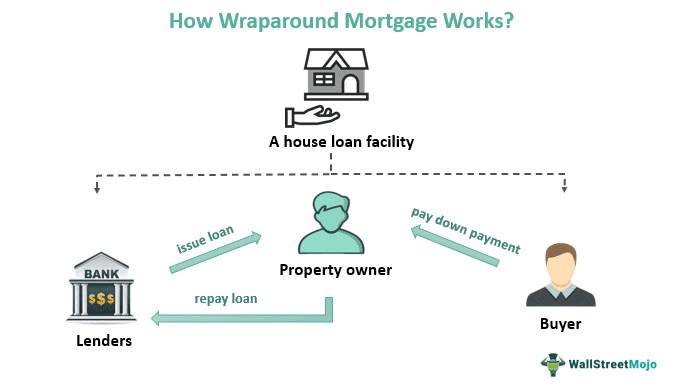

How Does Wraparound Mortgage Work?

A wraparound mortgage is a financing (loan) given to a borrower who cannot access traditional loan facilities. Instead, it wraps as a cover around the original mortgage. Thus, the borrower can take up this mortgage as a secondary facility to the traditional loan. It usually occurs in the real estate sector.

The wraparound mortgage concept dates back to the late 1970s and early 1980s when interest rates shot high. At that moment, the loan rates were 15-20% higher than earlier. Thus, to sell the properties, there was an urgency of creativity. This situation also occurs during inflation, when banks refuse to issue loans. During that phase, these mortgages are pumped into the market.

However, the working of wraparound mortgages concept still differs from others. While an individual still has a pending loan on the house brought, they can buy this mortgage to repay it to the banks. It means they will first collect the down payment from the buyer. Then, later, use the same amount to repay the owed.

If the property seller needs to avail of this mortgage, they must check whether their original loan is “assumable.” In other words, the outstanding loan amount is transferable from the original borrower to the buyer. If it qualifies the condition, the parties need to follow certain steps:

- Permission from the lender (loan provider) is necessary before the Seller issues a mortgage.

- Once the parties agree to the wraparound mortgage agreement, they will sign the promissory note.

- This agreement will include the loan amount, interest rate, down payment, and other details.

- The mortgage remains, while the title might get transferred once the payment is made.

- As the buyer pays the down payment, the seller uses the same amount to repay the lender.

Certain assumable loans include the Federal Housing Administration (FHA), Veterans Affairs, and the U.S. (United States) Department of Agriculture (UDA). However, conventional mortgages are discarded from this facility.

Examples

Let us look at the examples of the wraparound mortgage in real estate to comprehend the concept better:

Example #1

Suppose Cleve owns a new home in Manhattan, New York. He had taken a loan of $1 million from a renowned bank to purchase it. However, it was becoming difficult for him to repay the amount to them. As a result, Cleve thought to sell the house to Mark for $2.3 million. In addition, both entered into a wraparound mortgage contract. According to the deal, the latter will issue a down payment of $3000 till the full house value is paid. Cleve will then use the amount to pay back to the bank. In short, he tries to rotate the payments beneficially.

Example #2

On May 24, 2021, Texas amended new provisions about the wraparound mortgages. Per the new rules, they will consider various protection rights for the buyers and sellers. Others include the prohibition of the Seller who is not registered or licensed.

Pros And Cons

Wraparound mortgages are a very useful tool for both buyers and sellers. While banks refuse to issue loans, the sellers (a person selling property) can issue these mortgages. As a result, buyers can easily access this facility. Besides, there is less documentation needed. On full payment, the buyer gets the title of the property.

Although it is an advantage for them, it has similar disadvantages to the buyers. Even if they access this loan facility, the Seller has a good chance of charging a high interest rate. As a result, the Seller can make huge profits from the buyer. In addition, there are chances of default or breach by both parties.

| Pros | Cons |

| Fewer requirements and documents. | High-interest rates. |

| Huge profits for the seller. | Higher chances of contract breaches. |

| Easy repayment of the loan. | Foreclosure risk. |

| More flexible arrangements for the buyer. |

Wraparound Mortgage vs Subject To

Although wraparound and subject to the mortgage are closely related, they have vast differences. The Seller issues the former to the property buyer so they can use the amount to repay their original loan. A rotation of money from the buyer to the lender (banks). However, in the case of the subject of loans, it is different. Here, the buyer will pay directly to the bank. Thus, the intermediary of the Seller disappears. As a result, all the outstanding due is transferred to the buyer.

| Basis | Wraparound Mortgage | Subject To |

|---|---|---|

| Meaning | It refers to a loan facility where buyers can borrow funds to buy house property. | Subject to is a facility where the current owner will continue making outstanding payments to the lender. |

| Purpose | To provide a separate loan to those who cannot qualify for traditional mortgages. | To pay the remaining amount owed back. |

| Who pays? | The buyer pays the seller (property owner). | Here, the buyer pays the lender (like banks). |

Frequently Asked Questions (FAQs)

Which transaction would create a wraparound mortgage?

These mortgages usually occur in transactions when the seller cannot repay the original loan the lender took (bank). In this situation, they can ask the lender to issue a mortgage to repay their existing loan.

What are the alternatives available for wraparound mortgages?

Other alternatives to these mortgages are given below. Let us look at them:

● Improving the existing financial or credit score.

● Seeking affordable loan options like FHA (Federal Housing Administration) or others issued by the government.

● Checking out different down payment assistance programs.

Who holds the title in a wraparound mortgage?

The title remains with the latter unless the buyer makes full repayment to the seller (property owner). Once the payment completes, the buyer gets the property title and related rights.

What is the difference between a second mortgage and a wraparound mortgage?

While both serve almost the same purpose, there is a slight difference between them. A wraparound mortgage is a secondary loan facility given to the seller. They can secure a deal with a buyer and use the down payment amount to the lender. However, the second mortgage is an addition made to the original loan.

Recommended Articles

This has been a guide to what is a Wraparound Mortgage. Here, we explain its examples, pros and cons, and compare it with the subject to. You can learn more about accounting from the following articles –