What Is An Assumable Mortgage?

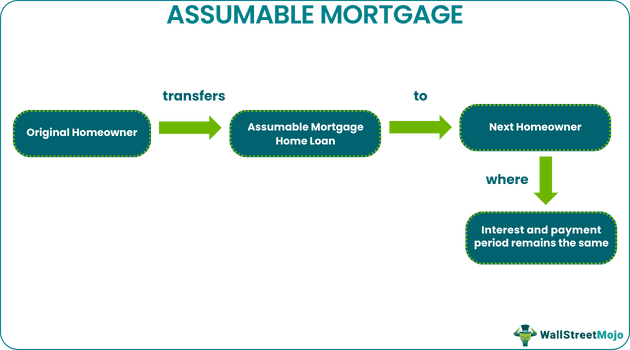

An assumable mortgage is a mortgage type where the obligation can be transferred from one individual to another during the transaction of a property. This mortgage type helps a buyer purchase a property with lower interest rates when the current market interest rates have increased.

Assumable mortgage loans permit a buyer to purchase a home and take over the seller’s mortgage loan. As a result, the interest rate the buyer pays on the mortgage loan is the interest at which the seller initially took the home mortgage loan. However, it comes with strict rules and restrictions. For example, the seller must qualify the lender’s credit and income requirements to qualify for this loan.

- An assumable mortgage is a loan type where the debt liability can be transferred from one individual to another. In this mortgage type, the buyer can purchase a house from the seller by acquiring the seller’s mortgage loan, where the interest and repayment time stays the same.

- Assuming a mortgage benefits the buyers in a scenario where the market interest rates have risen over time.

- It allows the buyer to purchase a property at the interest rate at which the seller initially took the mortgage loan, which is often less than the current market interest rate.

How Does An Assumable Mortgage Work?

An assumable mortgage allows the transfer of mortgage loan liability from a seller to a buyer. For example, in assumable mortgage loans, a buyer can purchase a house from a seller while taking over his mortgage loan under his name. This will free the seller from their debt, and the new homeowner will assume the seller’s mortgage loan. However, the interest rates and repayment period remain the same.

This mortgage loan allows a buyer to repay the mortgage loan at the interest rate at which the seller initially took the loan. This loan type is beneficial when the prevailing market interest rates have increased over the years. Assuming a mortgage allows the buyers to repay the loan at a significantly reduced interest rate, which they would not get in the current market.

However, this mortgage loan comes with several rules and restrictions. First, the lender’s approval is necessary for assuming a mortgage. The buyer must meet the lender’s income and credit requirements, failing which, the lender will not release the seller from their continuing mortgage liability.

The Hargreaves Lansdown provides access to a range of investment products and services for UK investors.

Types

The assumable mortgage types are as follows:

#1 – FHA Loans

FHA loans are loans that the Federal Housing Association guarantees. The loans originating on or after December 15, 1989, require the creditor to approve the assumption sale to a buyer eligible to meet the lender’s credit requirements.

#2 – VA Loans

The Department of Veterans Affairs guarantees these loans. Generally, the borrowers must be veterans, active-duty service members, or qualified surviving spouses to avail of this loan. However, the buyer does not necessarily need to be affiliated with the military. All the VA loans are assumable, although they come with specific rules and eligibility requirements.

#3 – USDA Loans

The Department of Agriculture guarantees USDA loans. They are assumable with the same rates and terms or with new rates and terms.

Examples

Let us understand this concept with the following examples:

Example #1

Suppose Brown bought a property worth $1 million in 2010. He opted for an assumable mortgage with an interest of 5%. In 2020, he decided to sell the house for $2 million. The prevailing interest rate in the market in 2020 was 8%. Green purchased the property from Mr. Brown at $2 million and transferred the mortgage loan. He had to pay a 5% interest rate for the property, which was significantly less than the ongoing market interest rate of 8%. This is an assumable mortgage example.

Example #2

Carrington Mortgage Services, a financial institution based in California in the United States, witnessed a window of opportunity in the mortgage market. Assumable mortgages have become popular in recent years when the market interest rates are surging. However, it has strict rules and restrictions, making it a rare alternative for financing home loans.

Lenders, mortgage services, and other financial institutions are trying to make this mortgage type more accessible. Still, the government must update some policies to make this lending process more accessible and feasible. This is another assumable mortgage example. Meanwhile, other lending specialists in California like 5 Star Loans focus on different financing solutions, offering title loans for cars, boats, and motorcycles to serve diverse borrowing needs in the state.

Pros And Cons

The benefits of assumable mortgage to sellers are as follows:

- Selling a home with this mortgage is easier if the interest rates have increased over the years. For example, if a homeowner purchases a property with a 5% interest rate and sells it after five years, the interest rate will remain the same, whereas a new home loan will have an increased interest rate. This difference in the interest rates makes the property with this mortgage more desirable in the market.

- The original homeowners might get a higher price on their property due to the reduced interest. Since the interest on their property will always be lesser than the prevailing home loan interest rates, the buyers can save more on this property type. As a result, the sellers might get higher property prices if they negotiate.

The benefits of assumable mortgage to buyers are as follows:

- The buyers can purchase a property with this mortgage with a lesser interest rate than the current market rate, which would not have been possible otherwise. As a result, they can save money by paying less interest on the loan.

The disadvantages of assumable mortgage are as follows:

- Assuming a mortgage may require the buyer to pay a significant amount as a down payment. It may not be possible for the buyer to spend a considerable amount as a down payment.

- One of the significant disadvantages of assumable mortgages is that there are strict income and credit requirements for this loan type. The buyer may not be eligible to meet the lender’s income and credit requirements for assuming a mortgage, due to which the lender will not release the seller from their ongoing liability.

Assumable Mortgage vs Non-Assumable Mortgage

The differences are as follows:

- Assumable Mortgage: This loan type transfers the mortgage from one owner to another. In this, the buyer assumes the mortgage liability from the seller. After the purchase, the seller has no obligations on the debt.

- Non-assumable Mortgage: This loan type does not allow the buyer to assume the mortgage from the seller. Some mortgages come with non-assumable clauses which restrict the sellers from transferring the mortgage liability to the buyers. All the standard loans and mortgages are non-assumable.

Disclosure: This article contains affiliate links. If you sign up through these links, we may earn a small commission at no extra cost to you.

Frequently Asked Questions (FAQs)

1.How to find assumable mortgage homes for sale?

There are several ways to find these mortgage homes for sale, and they are as follows:

· Various online listings and websites provide leads to properties with this mortgage type.

· Real estate agents can help one find homes with this mortgage type.

· One can search for lenders who provide products with this mortgage. Several credit unions, banks, and other financial institutions specialize in this loan.

2.How do I know if I have an assumable mortgage?

To know if a property has this mortgage type, one must look for an assumption clause in the mortgage contracts. This provision allows the loan transfer from one individual to another. The buyer may also contact the seller to ask if there is a provision to finance the property through this loan.

3.How to take over an assumable mortgage?

One must contact the current homeowner to take over this mortgage and convey their intentions. If both parties agree, they can approve the loan transfer. Both parties must review all the legal documents necessary for the mortgage transfer. Then the lender can initiate the transfer process. Furthermore, homeowners can take the help of an attorney to ensure that the transfer process is seamless and hassle-free.

Recommended Articles

This has been a guide to what is Assumable Mortgage. We explain its pros, cons, examples, differences with non-assumable mortgage, and types. You can learn more about it from the following articles –

Recommended Articles

Continue with these closely related articles from the same guide.