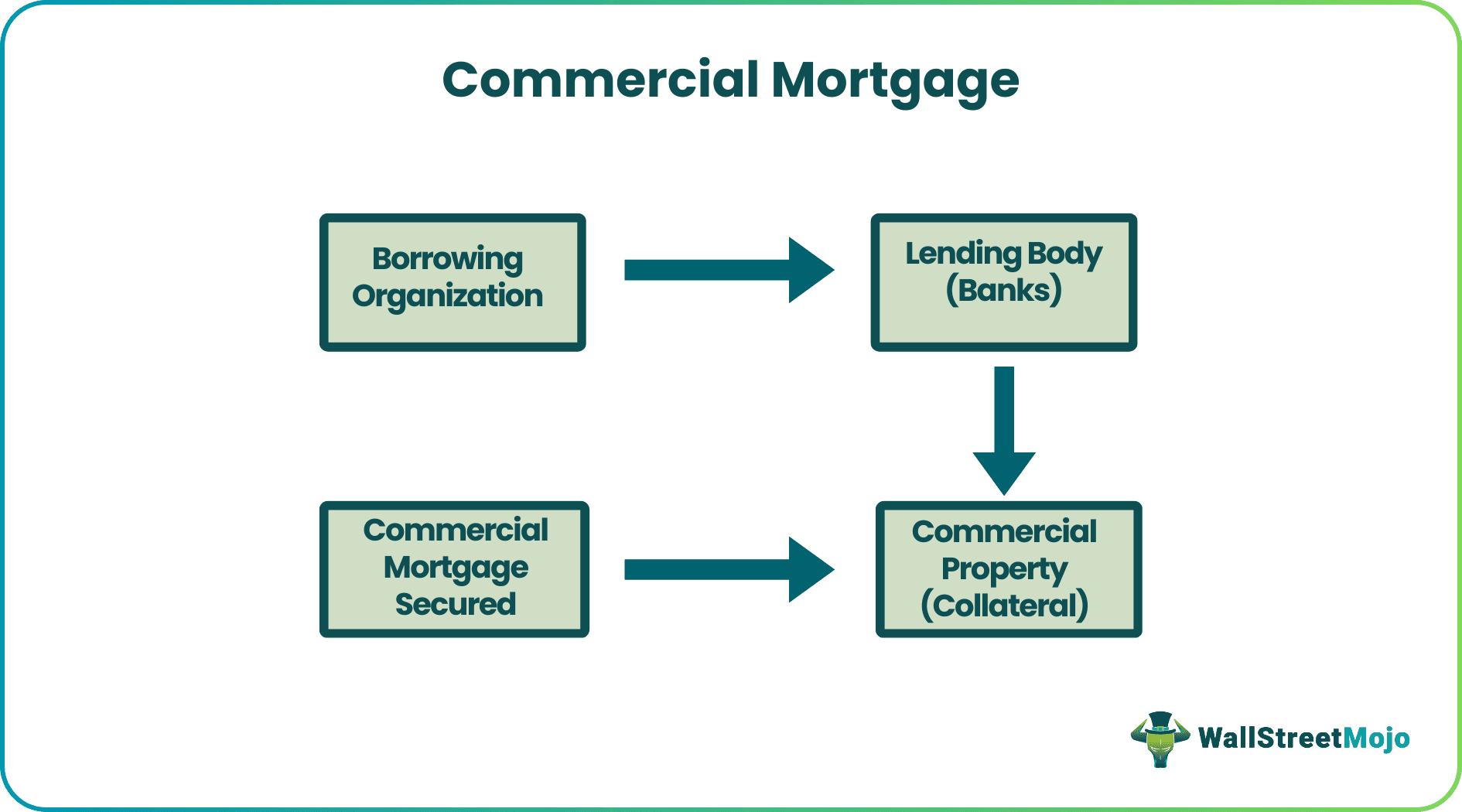

What Is Commercial Mortgage?

A commercial mortgage is a loan usually secured by a commercial property like an industrial warehouse, office building, shopping center, or apartment complex. The receipts from the loan are usually used to acquire, replenish, or refinance a commercial property. The financing of such loans is not carried out through personal money but from business operations or rental income.

Commercial mortgage rates are highly influenced by the risk the lender bears, the market condition, and the borrowing request. In addition, it often has a floating interest rate which means the interest is variable due to the above factors. Banks, traditional financial institutions, insurance companies, and large pension funds offer these loans.

- A commercial mortgage is a loan offered to business entities, usually for replenishing, redeveloping, rebuilding their existing premises, or acquiring a new property.

- The business’ profitability, creditworthiness, actions to tackle debts, and other financial commitments play a significant role in sanctioning the loan.

- Moreover, future projections or plans are mentioned along with the application to give the lender an idea of the enterprise’s plans.

- A typical repayment schedule comprises the repayment of the interest with a combination of amortization periods that the borrowing entity is subjected to follow.

Commercial Mortgage Explained

A commercial or business mortgage is a loan secured by a commercial property. It is usually derived to refinance or refurbish a business property. While some organizations acquire a business mortgage to own the property where the business activities are carried out, other investors acquire such a loan to purchase a property to rent out or lease to another entity.

Before funding a business mortgage, the lenders do their due diligence through an extensive financial review of the property and its owner. In addition, many underwriting and appraisals are raised before the deal is closed.

In 2013, $3.1 trillion of commercial and other mortgages were outstanding in the United States. Banks, state-backed enterprises, and life insurance companies held the most outstanding mortgages.

How To Get Commercial Mortgage?

Securing a commercial or a business mortgage is more challenging than securing a residential mortgage because of the sheer paperwork and scrutiny it is put through before sanctioning. A business can apply for such a mortgage directly to the bank or insurance company or through an adept commercial mortgage broker.

Apart from the commercial mortgage rates in terms of interest and other fees, the borrower has to put forth a deposit of around 20-40%, which is way higher than that of a residential mortgage that follows a 5% deposit cut-off.

Moreover, these loans range between five to twenty years, with an amortization period longer than the loan’s term. In this case, the borrower pays monthly installments along with interest for the term period, followed by a final payment of the amount of the loan, often referred to as a balloon payment.

Apart from the usual checks in terms of affordability and credit check, the lender checks the business’s profitability and action to manage debts and commitments that already exist within the organization.

To provide sufficient data for the lender to conduct the necessary background checks on the business, they may have to submit two to three months of bank account statements, address, and identity proof. Additionally, the organization can provide a business forecast for the perusal of the lender to understand the plan of action that the decision-makers have for the organization.

These steps may vary from case to case, but typically, an applicant would follow these steps:

- The online commercial mortgage form is filled

- Relevant and important information regarding the business is submitted

- Valuation of the property is drawn out for the property the organization wants to buy

- Wait while the lender and their team carry out their due diligence before approving

- Once approved, a formal commercial mortgage loan offer is sent across.

Examples

Let us understand the ebbs and flows of this concept better through the examples below:

Example #1

Elite Corporation Inc. acquired a business loan for $10 million from ABC Bank to fund acquiring a new office building to accommodate the increasing workforce. The loan term was five years with an interest of 5%. They paid the interest of 5% every year for five years for $4,294.57 every month. After five years, they made a balloon payment of $734,629.91 and settled the remaining amount from the loan.

Example #2

Vornado Realty Trust acquired a $542 million loan to redevelop their 350 Park Avenue office campus by replacing their existing premises with a 1,500-foot tower. The loan was initiated in 2016 and will be due in 2027.

In 2022, Vornado requested a special servicing after rumors of the default of this loan surfaced. The property was valued at $710 at the time of the loan’s origination.

Commercial Mortgage vs Residential Mortgage

Despite the basics of requirements and lender bodies being the same, there are differences at all levels of securing the deal, tenure, and other factors. Let us take a look at the table below to understand the dissimilarities between the two:

| Basis | Commercial Mortgage | Residential Mortgage |

|---|---|---|

| Borrowers | Business enterprises like developers, funds, and trusts secure commercial or business mortgages. | Residential mortgages are offered to individual borrowers. |

| Time Frame | Loan term ranges from five (or less) to twenty years, and an amortization period longer than the term of the loan. | The usual term ranges between twenty-five to thirty years. However, shorter periods are also offered by different lenders. |

| Deposit (Down Payment) | The initial deposit is usually between 20%-40%. | It is usually around 5% of the loan amount. |

| Qualification | Profitability of the business, current plans to tackle existing debt and commitments, and plans for the business play a pivotal role in the loan being sanctioned. | The borrower’s income and affordability are the main factors that lenders tend to consider before sanctioning a loan. |

| Interest | The interest rates can be fixed or variable, depending on the lender. However, an amortization period is levied, usually longer than the term of the loan. | A fixed interest rate is levied on the tenure of the loan, which the borrower pays in installments every month with interest. |

Frequently Asked Questions (FAQs)

Frequently Asked Questions

1. How much deposit for commercial mortgage?

<p>The deposit amount depends on various factors but is commonly between 20%-40% of the total mortgage amount. Of course, the rate can be greater or lower than this based on circumstances. Usually, it is decided based on the risks the lender perceives to bear on the commercial mortgage loan.</p>

2. How long is a commercial mortgage?

<p>The commercial loan time frame ranges from five to twenty years. Moreover, the amortization period is usually drawn out beyond the loan’s term period. For example, a commercial mortgage broker might draw a commercial loan for six years with an amortization period of 20 years.</p>

3. How to become a commercial mortgage broker?

<p>To become a commercial mortgage broker, one has to secure a degree in finance, economics, or business. Additionally, employers prefer candidates with experience in either the lending industry or real estate, post which to attain the license; one has to take an exam with the National Mortgage Licensure System (MNLS).</p>

4. What are commercial mortgage backed securities?

<p>Commercial mortgage-backed securities (CMBS) are bonds issued against commercial property. They provide liquidity for both commercial lenders and real estate investors. In case of a default, the loan in a CMBS acts as collateral to the investors.</p>

Recommended Articles

This article has been a guide to what is Commercial Mortgage. Here, we explain how to get it, its examples, and a comparison with a residential mortgage. You can learn more about it from the following articles –