What Is A Tracker Mortgage?

A tracker mortgage is a variable-rate mortgage linked to the Bank of England base rate. The mortgage interest fluctuates parallel to the base rate but is not the same. Instead, the mortgage interests are slightly above the base rate. It aims to let borrowers take advantage of fluctuating interest rates depending on the base rate and prevailing market conditions.

Since it is dynamic, the borrower will pay a different interest rate installment each month. Its utility is based on the ever-changing Bank of England’s base rate to offer the borrowers an easement in paying off debt. However, it is unpredictable and has drawbacks, and proper research is advisable.

- The tracker mortgage is a variable rate mortgage linked to the Bank of England base rates.

- It differs from the standard variable mortgage, and the interest is slightly above the United Kingdom base rates.

- All tracker interest rates move parallel to the base rates. But the actual interest varies between banks.

- The Barclays Tracker Mortgage and Tracker Mortgage NatWest are common examples.

Tracker Mortgage Explained

The track mortgage offers variable interest rates to borrowers. However, the track mortgage is linked to the Bank of England’s base rate compared to other variable rate mortgages. If the loan is not capped, there is no limit; if the base increases, the mortgage interest also increases. Similarly, if the base rate decreases, mortgage interest also decreases.

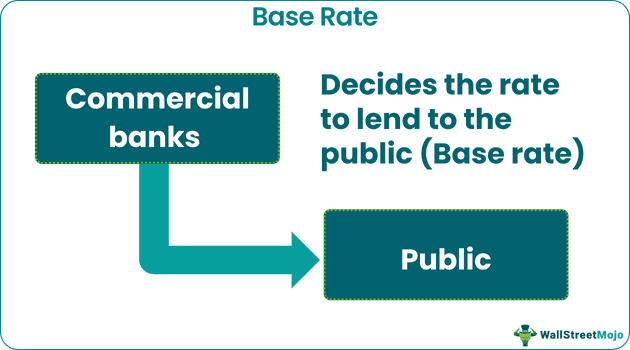

The base rate is the minimum interest rate a commercial bank can offer a borrower. Commercial banks cannot offer loans below the base rate.

Borrowers acquire a mortgage to purchase or refinance a house. The purchased property act as the collateral; if the borrower defaults, they can seize the property. Now, variable interest rates correlate with an underlying benchmark — CIBC prime rate, LIBOR rate, or federal funds rate.

Variable-interest mortgage borrowers repay the loan in monthly installments. The actual amount paid on a particular month depends on the base rate. It is challenging for borrowers to track the change in interest rates. A borrower also has to alter monthly expenses accordingly. Therefore, it is recommended that borrowers must compare various variable interest loans before finalizing. Alternatively, if a borrower is short on time or lacks financial understanding, they can opt for a fixed-interest loan.

To mitigate risks associated with variable interest rates, borrowers can include other repayment options. But this has to be done before signing a loan agreement. Variable-interest mortgages are notorious for scandals and controversies; banks overcharge borrowers and deny tracker rates. Therefore, every borrower must research various loan options and read the loan agreement details before signing.

Examples

Let us look at some tracker mortgage examples.

Example #1

Glenn took a home loan based on a lifetime tracker mortgage. The tracker mortgage interest rate differs from the Bank of England base rate. This is how it works; the movement in mortgage interest rate is parallel to the movement in The Bank of England base rate, but the rates are not the same.

That is, mortgage interest rates are set slightly above the base rate. So, if Glenn’s tracked mortgage is regulated at 0.9% and the base rate is 1.8%, the total interest rate charged from Glenn will be as follows:

- Variable Interest Rate = 1.8% + 0.9%

- Variable Interest Rate = 2.7%

Thus, Glenn was charged an interest rate of 2.7% for the first month.

Then, the base rate plummeted to 1.1%. Thus, for the second month, Glenn will pay the following interest:

- Variable Interest Rate = 1.1% + 0.9%

- Variable Interest Rate = 2%

By the third month, the base rate hikes to 2.7%; Glenn ends up paying the following interests:

- Variable Interest Rate = 2.7% + 0.9%

- Variable Interest Rate = 3.6%

Example #2

In December 2022, The Bank of England increased the interest rates. Borrowers are unhappy; a higher mortgage rate will hit them. In 2022 alone, the Monetary Policy Committee (MPC) hiked the base rate nine times.

There will be a parallel increase in the tracker mortgage rates as well. The Deutsche Bank believes rates could go as high as 4.5% in early 2023.

Pros And Cons

Tracker mortgage pros are as follows:

- Tracker interest rates are directly proportional to the base rate.

- In most cases, the lender’s tracker rate is below the standard variable rate (SVR).

- Lenders cannot hike the rates unless The Bank of England base rates increase. Thus, it is a reliable metric.

- If a cap is introduced, the interest rate will not go beyond a point, even if the base rate keeps increasing.

- Often, variable-rate mortgages allow borrowers to repay early—without a prepayment penalty.

The cons are as follows:

- If the base rate keeps increasing, so will the loan interest rate. Without including a cap, this is a risky proposition.

- Tracking the repayment amount and interest rates becomes tedious for most borrowers. Also, the borrower has to plan other monthly expenses around the ever-changing installment.

- If the borrower wants to opt out of variable interest rates, they have to pay a hefty switch fee (to switch from one type of mortgage to another).

Difference Between Tracker Mortgages And Variable Rate Mortgages

The difference between tracker mortgages and variable rate mortgages are as follows:

- Tracker mortgages are linked to Bank of England base rates. In contrast, variable rate mortgages are not linked to any such tracker or index.

- The tracker interest rate will always be above the UK base rate. On the contrary, variable rate mortgages are standardized but fluctuate due to other market factors.

- Tracker mortgages reflect the United Kingdom base rate, whereas discounted variable rate mortgages offer discounts on set percentages.

Tracker Mortgage vs Fixed Rate Mortgage

Now, let us look at tracker mortgages vs fixed-rate mortgages to distinguish between the two.

- A variable rate mortgage is linked to the Bank of England’s base rate. In contrast, fixed-interest mortgages are not linked to any index. Every bank offers a different fixed rate to its customers.

- Variable-rate mortgages are dynamic and frequently change before the completion of the loan term. In contrast, the fixed-rate mortgage does not fluctuate—it remains the same throughout the loan tenure.

- Borrowers who opt for variable-rate mortgages end up paying an increased or decreased loan installment every month. This is not the case with fixed-rate mortgages.

- Borrowers who opt for variable-rate mortgages must plan their expenses around the base rate changes. Financial planning is easier with fixed-rate mortgages.

Frequently Asked Questions (FAQs)

What’s the difference between fixed and tracker mortgage?

With a fixed-rate mortgage, users make the same payment each month for the life of the loan, which is how a tracker mortgage differs. On the other hand, the SVR interest rates are subject to alteration at the lender’s discretion. As a result, a tracker mortgage is typically more affordable and predictable.

Can someone get out of a tracker mortgage?

One of the key advantages of variable-rate mortgages is that it offers penalty-free early repayment options. Some variable-interest loans even allow switching without fees. Thus, borrowers can complete the lump sum or opt for an alternative repayment structure. Every mortgage has a specific condition; borrowers must review the loan agreement carefully before signing.

What is the tracker mortgage rate in Ireland?

In 2022, it was 1.2 above the base rate. For example, if the ECB rates are around 2.4%, Ireland’s variable rate mortgage rate will be 3.6%. But this will change based on prevailing market conditions.

Recommended Articles

This has been a guide to what is a Tracker Mortgage. We compare it with fixed-rate and variable-rate mortgages and explain its examples and pros and cons. You can learn more about it from the following articles –