Table Of Contents

What is Interest-Only Mortgage?

Interest-only mortgages are a type of loan in which the borrower initially makes payments consisting of just the interest amount for a specified period of time. Once the interest-only period ends, borrowers begin making payments on the principal amount as well or choose to refinance.

Depending on how the loan is set up, the period of interest-only payment could typically last for the first 5 to 10 years or the whole of the term in some cases.

Table of contents

- What is Interest-Only Mortgage?

- Interest-only mortgages are a type of loan in which the borrowers do not immediately pay back the principal amount and only pay for interests accrued on the borrowed sum for a specified period of time. The interest-only period typically lasts for 5-10 years.

- Having lower monthly payments in the initial phase (due to just paying interest) buys a homeowner time to arrange for repayment finances.

- The monthly payments shoot up substantially post the interest-only period, requiring the borrower to pay both principal and interest amounts as happens in a conventional mortgage loan. Some lenders of interest only-mortgage charge higher interest rates post the initial phase.

- These loans can be useful for some, but since later on, the payment amount goes up, individuals should be financially prepared when going for them.

How Does Interest-Only Mortgages Work?

- Mortgages have two primary components which are principal and interest. The principal is the amount of money you are borrowing, whereas the interest is the fee you pay to the lender for allowing you to borrow the loan. In traditional types of mortgages, such as FHA loans and conventional loans, you will be required to pay some of the principal amount plus interest on top of it in your monthly payments.

- Sometimes, homebuyers are certain to acquire a bonus or consolidated amount from a will in the future after a specified period of time. Such buyers sometimes opt for an interest-only mortgage, giving them time to acquire their consolidated sum before the payment of the principal amount gets due.

- With interest-only kind, the borrower will only have to pay interest on the mortgage for a specific amount of time, usually 5 to 10 years. During the interest-only period, you can choose to make additional payments towards the principal, lowering the loan amount. Interest-only loan keeps your monthly payments low for the first few years, and then they will begin to increase as the period ends.

- The interest rate varies as per the loan's nature, which can either be a fixed-rate loan or an adjustable-rate mortgage (ARM). In a fixed-rate mortgage, the amount of interest paid does not change, it will be fixed. With adjustable-rate mortgages, the interest rate is typically fixed for an amount of time, and then the rate will alter based on the present market value. Depending on the type of loan, the rates of interest-only mortgage will be set.

- Some of the best lenders of interest-only mortgage are New American Funding, Guaranteed Rate and Wells Fargo. Normally for a conventional mortgage loan, a minimum credit score of 620 is required. To avail interest-only credit, the credit score in many cases requires to be over 620 as there is a greater risk of default with such loans.

How to Calculate Interest-Only Mortgages?

The calculations will consist of two parts - during the interest-only phase and after. As the name implies, you will start by only paying the interest amount on loan during the interest-only phase. The interest rate will either be a fixed-rate or an adjustable-rate during that period. In fixed-rate, the payments shouldn’t change.

Many lenders opt for the loan type of adjustable-rate mortgage for an interest-only mortgage. This ensures that they reap higher interest earnings with the changing market conditions. The mortgage structure may change post the interest-only phase depending on the structure of the loan.

Keep in mind that your payments will increase significantly after the initial phase is over without contributing towards the principal redemption during this time. You will have to pay interest on top of the principal that now needs to be paid off in a shorter time. Using a mortgage calculator, you can determine the monthly payment for the remaining amount.

Interest-only loans are typically structured as ratios. For example, a 7/1 loan ratio means the first seven years will be interest-only, and after that period, the interest rate adjusts once a year. There are plenty of interest-only mortgage calculators worldwide that can help you compute the amount of due interest and principal amount. In the interest-only mortgage calculators, you will need to enter the loan details and the prevailing annual interest rate.

Example

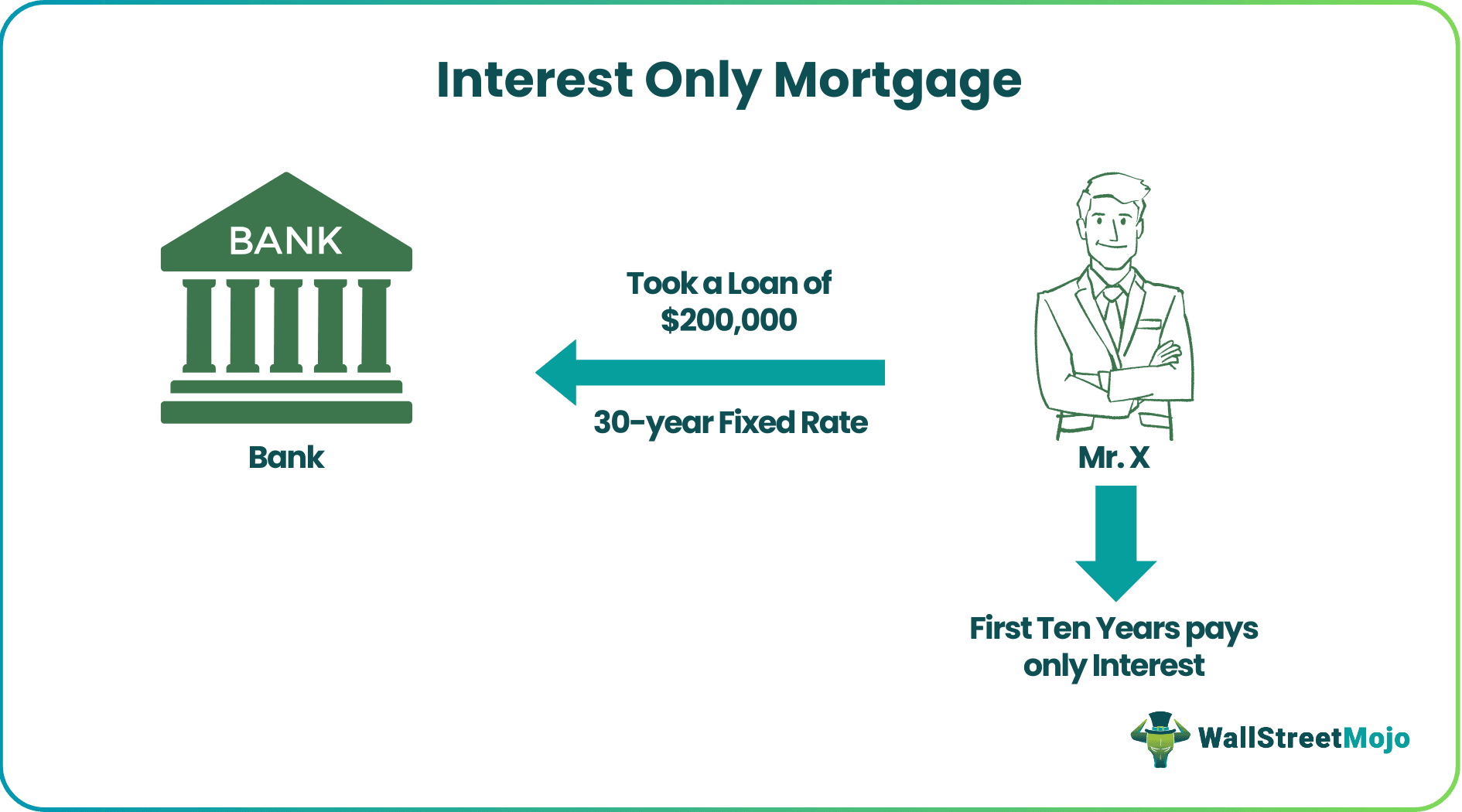

Let’s say you are looking to buy a $250,000 house and afford to put $50,000 down towards it. So, you go to the bank looking for a $200,000 loan. The loan is a 30 year fixed rate, with the first ten years being interest only at an interest rate of 3.2%. This means that for the first ten years, you will be paying $533 a month towards the loan in interest only.

After the first ten years, the monthly payments will go over $1,200, assuming the same interest rate. That’s more than double the amount you were paying during the initial interest-only period. The significant increase is due to pushing the principal payments back. Some borrowers opt for a lump-sum payment or a balloon payment route to repay the whole principal amount in one go. They can save themselves from the hassle of the increased amount of monthly payments post the interest-only phase.

Pros and Cons

There are advantages and disadvantages you should consider with interest-only mortgages. These include:

Pros

- With mortgage payments typically being one of the most significant expenses for many people, going with interest-only loan can help keep payments low. This can allow individuals to pay off debt (student loans, medical expenses, high-interest credit cards) that might need more immediate attention.

- During the interest-only phase, if your interest rate is low, you can potentially invest the money you would be paying towards the principal in other investments that will yield a higher return in future.

- Mortgage interest is tax-deductible (for loans less than $750,000), so payments will be deductible during this period.

- Interest rates are typically low during the initial phase.

Cons

- After the initial interest-only period, your payment will increase significantly, catching some people off guard if they are not prepared at the time.

- You are also not building equity in the house as you are just paying interest, not contributing towards the principal.

- Although during the initial period interest rates are low, you will typically encounter higher interest rates afterwards because they become adjustable. Not only will you be paying the principal, but you will most likely have a higher interest rate as well.

- The value of your home can decline, leaving you owing more money than what the house is worth. This can make things difficult when trying to refinance the mortgage before the initial phase is up.

- In some instances, the borrower may owe a big lump sum of money once the interest-only period is complete. At times, they require a substantial down payment.

- Interest-only contracts are often stringent, often dissuading the consumers from taking them, especially with the fear of exploitation. As per a study, allowing more flexibility in the contract led to an increase in the consumption of interest-only financial plans in Denmark.

- Borrowers must qualify for these types of loans, and in some instances, it may be tough to pass the qualifications: higher credit scores, asset ownership, and a high income to debt ratio.

Recommended Articles

This has been a guide to what is interest-only Mortgage and its meaning. Here we discuss how to calculate interest-only mortgage and how it works along with Pros & Cons. You may learn more about financing from the following articles -