Part of our Retirement Planning guide

Accumulation Phase Meaning

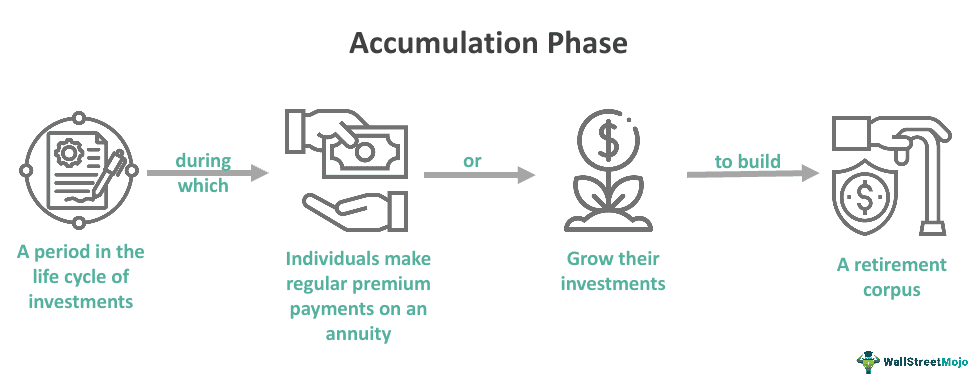

The accumulation phase is the time in the investments’ life cycle when investors or individuals build up their investment or annuity’s value. This phase is crucial as the sooner people enter this phase, the more they can save for their retirement.

This is the second stage or phase of the investing process, and it comes prior to the distribution base, in which individuals begin utilizing the accumulated funds. Considering that people choose to forego immediate consumption to get a substantial payout in the future, the time value of money and delayed gratification are two fundamental principles at work.

- The accumulation phase refers to a duration in which individuals increase their savings and build their investment portfolio value to have substantial funds for retirement.

- The four phases of the investment life cycle are planning, accumulation, distribution, and legacy. The accumulation period is the longest among these phases. Moreover, generally, it has a fixed duration.

- Persons grow their savings and investments during the accumulation phase of the investment cycle based on the planning period. They utilize those savings and investments during the distribution phase.

- The accumulation period’s length depends on when one starts saving and plans to retire.

Accumulation Phase Explained

The accumulation phase refers to a period during which individuals make contributions to investments regularly or pay premiums on any insurance product, for example, an annuity. They intend to utilize the annuity for retirement purposes. After the payments on an annuity start, the contract enters the annuitization phase. One must enter this phase as early as possible to build a substantial retirement corpus.

As the name suggests, the money in individuals’ accounts or their investment capital’s value accumulates over time until they are ready to utilize it. One must note that the accumulation period‘s length might be already mentioned at the time of account creation. Alternatively, it can depend on when they choose to withdraw money from the account on the basis of their retirement timeline.

In a deferred unity context, this phase refers to the duration in which annuitants contribute to an annuity and increases the annuity account’s value. Usually, the annuitization phase follows the period for a certain duration, which usually lasts their lifetime.

There are three stages of the investment life cycle besides the accumulation phase. Let us look at them serially.

- Planning Phase: This phase lays the foundations for comprehending options available to an investor with regard to investment options, security selection, goal-setting, budgeting, and security selection according to an individual’s requirements. In this phase, individuals identify their investment requirements.

- Accumulation Phase: This stage is the longest period of an investment’s life cycle. Investors in the accumulation phase execute the plan prepared in the planning phase.

- Distribution Phase: Individuals enter this phase when they retire. Alternatively, one may trigger it when approaching retirement.

- Legacy Phase: In this stage, sophisticated investors try to fulfill their retirement goals and achieve their legacy by concentrating more on the second phase.

Examples

Let us look at a few accumulation phase examples to understand the concept better.

Example #1

Suppose an individual named David starts saving at the age of 24. The accumulation phase can be roughly 35-40 years long. The duration will depend on when he wants to retire. Usually, people take retirement around the age of 60 to 65, and considering an average life expectancy of 85-90 years in the majority of the developed nations, the distribution phase is about 25-30 years. David can be in a decent financial position by investing his money judiciously during the accumulation period to get a substantial payout when the phase is over.

Example #2

Suppose Sam, who is 35 years old, has to pay a fixed sum every month on an annuity for a predetermined duration of 25 years (until he is 60) to ensure a fixed income stream following his retirement. He is making this payment during the accumulation phase. After retirement, he’ll trigger the distribution period, during which he will receive a fixed income guaranteed by the annuity.

Importance

Individuals who know their current and future consumption requirements can largely benefit from the accumulation phase of the investment life cycle as they increase their investments’ value to a level that can be extremely valuable when their earnings fall. It is evident from many individuals’ lives that income tends to be higher prior to their retirement. Following retirement, consumption levels are above their income levels.

The majority of the people who begin investing in the early stages of their lives effectively use time during the accumulation stage. This makes it possible for them to build a larger retirement corpus than persons who enter the accumulation phase of investments’ life cycle later on in their lives. This fact emphasizes the importance of starting to invest as early as possible and making it possible to increase investments’ value by depending upon the accumulation of compound interest.

The annuitization or distribution phase might be predictable in terms of length and could fail to capture the consumption estimates correctly. However, typically, the accumulation phase comes with a fixed period. Moreover, it does not vary that much for average individual investors.

Accumulation vs Distribution Phase

Understanding the accumulation and distribution phase can be difficult for individuals unfamiliar with the concept of the investment life cycle. That said, one can understand their meaning clearly by knowing how they differ. In that regard, individuals must look at their distinct features.

| Accumulation Phase | Distribution Phase |

|---|---|

| It is the second phase of an investment’s life cycle. | The distribution phase is the third phase of an investment’s life cycle. |

| Investors in the accumulation phase implement the plan they prepared in the planning phase. This period involves individuals working and growing their retirement corpus through savings and investment. | During this phase, individuals utilize the funds utilized |

| One enters this phase after the planning phase. | Individuals trigger this phase upon retirement or in the years that lead to retirement. |

Accumulation vs Pension Phase

The concepts of the accumulation and pension phases can be confusing for a person who is new to the world of investments. That said, individuals can clearly comprehend their meaning and purpose and avoid confusion by learning about their key differences. So, let us find out how they differ.

| Accumulation Phase | Pension Phase |

|---|---|

| It is part of an investment’s life cycle. | The pension phase is not a part of the investment life cycle. |

| One enters this phase when they are working and growing their savings and investments. | Individuals enter this phase when they are already retired or fulfill a condition of release and begin withdrawing their super. |

Frequently Asked Questions (FAQs)

1.How long can you keep super in the accumulation phase?

During this stage, individuals and their employers put funds into the account and accumulate or increase the money via investments. People remain in this phase until they reach a certain employment status or an age that satisfies the condition of release for the super funds.

2.What to do in the accumulation phase?

Let us look at some things investors in the accumulation phase must do.

1. Spend an amount that is lower than their income.

2. Ensure that the cost of investment is low.

3. Start investing or saving early and raise the amount of savings over time.

4. Build a diversified investment portfolio.

5. Plan ahead to minimize tax liability.

3.What is the maximum super in the accumulation phase?

It refers to the maximum amount individuals can transfer to all their pension accounts. The maximum limit may change. Hence, one must know the current limit before transferring funds.

Recommended Articles

This has been a guide to what is Accumulation Phase. We compare it with the distribution and pension phases, & explain its example and importance. You can learn more about it from the following articles –