Part of our General Ledger guide

Credit Balance Meaning

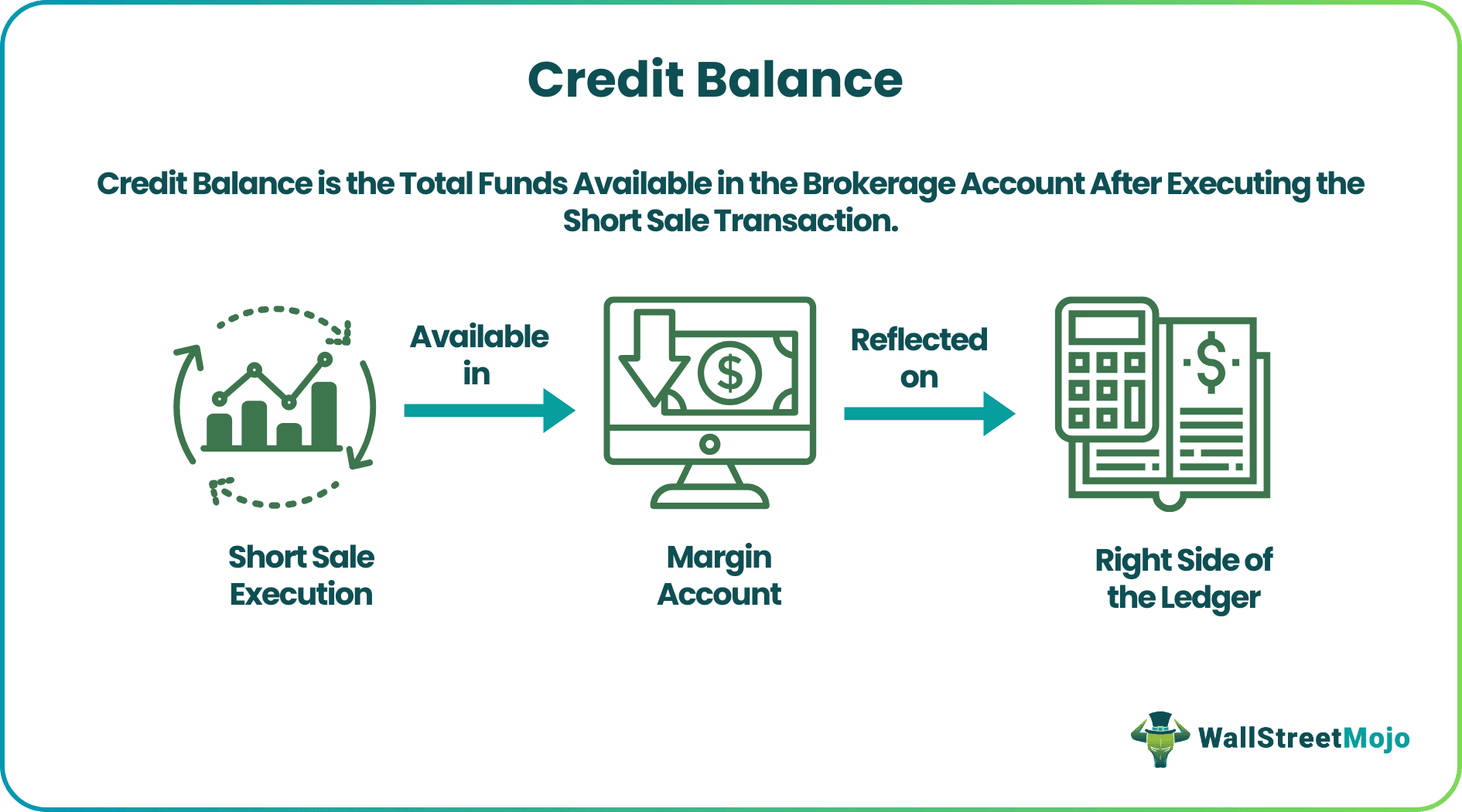

A credit balance is an amount attributed to the margin account following the successful completion of the short sale transaction. It normally assists in counterbalancing the prospective future losses of the firm. A credit surges the equity or liability account on the balance sheet, while a debit raises the expense or asset account.

Credit balance transfer cards aid you in transferring the payable credit card amount to another bank’s credit card for a lesser debt burden. Moreover, the ledger accounts with a credit balance are liabilities, income, contra expense, reserves, capital, and provisions.

- The credit balance is the full amount credited to the cash account after implementing the short sale order.

- The associated general ledger accounts comprise income, reserves, liabilities, provisions, capital, and contra expense.

- It may be negative or positive and is stated on the right side of the accounting book to counterbalance the debit portions.

- This involves the total outstanding amount on the credit card, positive bank balance, amount payable in the margin account after buying securities, and negative balance in the asset account.

Credit Balance Explained

Credit balance or net balance is the final amount (positive or negative) mentioned to the right of the ledger in accounting. In the short sale, the investor sells financial securities in the market and then hopes to re-purchase them at a budget price. The brokerage account with short positions possesses a normal credit balance, that can be refunded, while the one with long positions has a debit balance.

That is to say, the net balance involves:

- Entire amount overdue on the credit card

- Positive bank balance

- Amount outstanding in the margin account after buying securities

- A positive balance in the equity, liability, gain, or revenue account

- Negative balance in the asset account

Moreover, the firm may also request for credit balance refund to get back those extra bucks paid more than the originally owed amount. Generally, net balance demonstrates that the sum of money owed to the organization exceeds the amount it owes.

Examples

Furthermore, let’s consider the below-mentioned normal credit balance examples.

Example#1

To clarify, assume that a firm, ABC Corp. maintains a balance sheet with routinely updated debit and credit details. As mentioned above, the following facts appear on the credit side.

- Trade payables: $2,00,000

- Share capital: $2,000,000

- Security premium: $3,000,000

- Capital reserve: $530,000

- Salary payable: $60,000

- Rent payable: $50,000

- Secured loan: $1,100,000

- Unsecured loan: $1,50,000

In short, here is the typical balanced ledger.

| Ledger name | Debit balance | |

|---|---|---|

| Motor car | $60,000 | |

| Fixed assets | $4,00,000 | |

| Furniture | $5,000,000 | |

| Laptops | $5,50,000 | |

| Cash in hand | $40,000 | |

| Bank balances | $300,000 | |

| Bank overdraft | (-) $3,00,000 | |

| Trade receivables | $575,000 | |

| Security premium | $3,000,000 | |

| Trade payables | $2,00,000 | |

| Capital reserve | $530,000 | |

| Share capital | $2,000,000 | |

| Rent expenses | $2,65,000 | |

| Rent payable | $50,000 | |

| Electricity expenses | $2,00,000 | |

| Salary payable | $60,000 | |

| Secured loan | $1,100,000 | |

| Unsecured loan | $1,50,000 | |

| Total | $7,090,000 | $7,090,000 |

Example#2

Here are the top 10 0% annual percentage rate (APR) credit balance transfer cards listed for May 2022 which certainly help you save on the interest. Moreover, these cards aid in credit card consolidation and let the investors switch to another card with better terms.

- US Bank Visa Platinum Card

- Wells Fargo Reflect Card

- Bank Americard Credit Card

- Citi Double Cash Card

- Citi Diamond Preferred Card

- Chase Slate Edge

- Citi Rewards+ Card

- Citi Simplicity Card

- Navy Federal Credit Union Platinum Credit Card

- Chase Freedom Flex

Credit Balance Accounts

The net balance is related to the following accounts in bookkeeping.

1. Liability Accounts

Please note that these are a group in the account book of a firm exhibiting the amount due. On the debit credit balance sheet, a debit to these accounts means liability cutback while a credit denotes liability increment. It has two major types, i.e., current and non-current liabilities.

They also include bank overdraft, short-term loans, debentures, secured loans, call and put options, deferred tax liabilities, unsecured loans, and swaps in finance.

2. Reserves

It is a fraction of the available profit set aside for a particular reason, like dispersion to shareholders in case of liquidation or business development. Furthermore, reserves or general reserve are of two kinds, namely, revenue reserves and capital reserves.

For example, reserve for dividends equalization, expansion, increased replacement expenses, shares premium, etc.

3. Capital Account

A capital account is the documentation of the funding amount and income from the company, incorporating minority interest accounts. That is to say, the capital account tracks retained earnings throughout one accounting period to another.

Please note that it has two chief subaccounts on the debit credit balance sheet, namely capital transfer and acquisition and disposal of non-produced, non-financial assets. Moreover, the examples encompass partnerships and LLCs, sole proprietorships, and shareholders.

4. Provisions

Please note that it represents the capital allocated by the business to offset predictable future losses or expenditures. This assists in computing the gross taxable income of the enterprise. For example, asset impairments, accruals, depreciation, bad debts, guarantees, provision for income tax, etc.

5. Contra Expense Account

A contra expense account is an account in the ledger that counterbalances another particular expense account and sustains the matching principle of accounting. Its examples include purchase allowances, purchase returns, and purchase discounts for the business transaction.

6. Income

It comprises the revenue and gain accounts certainly implicating the business’s cash from its operating and non-operating ventures. For instance, asset sales, the dividend declared, consulting services, and interest income..

Frequently Asked Questions (FAQs)

What Is a Balance Transfer Credit Card?

The financial organization issues a balance transfer credit card permitting the customers for the overdue balance transfer process to another bank’s credit card. In addition, it aids in diminishing the tax burden by offering low-interest rates on monthly installments.

How To Check Credit Card Balance?

Credit cardholders can check their balance (maybe refunded) through the following methods:

1. Internet Banking

2. Monthly credit card statement

3. Contacting customer care

4. Mobile app

5. ATM, or

6. SMS

The customers may also request for credit balance refund through offline or online portals.

What Is Statement Balance on Credit Card?

Statement balance on a credit card certainly depicts total payments and expenditures made to the account throughout one complete billing cycle. Therefore, paying up lesser than their statement balance will put the account in good standing, though they will incur interest rates. Meanwhile, the customers must prioritize the payment of their statement balance over the current balance.

Recommended Articles

This has been a guide to Credit Balance and its Meaning. Here we explain normal credit balance ledger accounts, balance transfer cards, & the refund process. You can learn more about accounting from the following articles –