Part of our Banking Products guide

What Is A General Account?

General Account refers to a pool of premiums received from its policyholders in collective investments, which are used not only to meet the company’s operating expenses but also to pay various insurance claims and benefits.

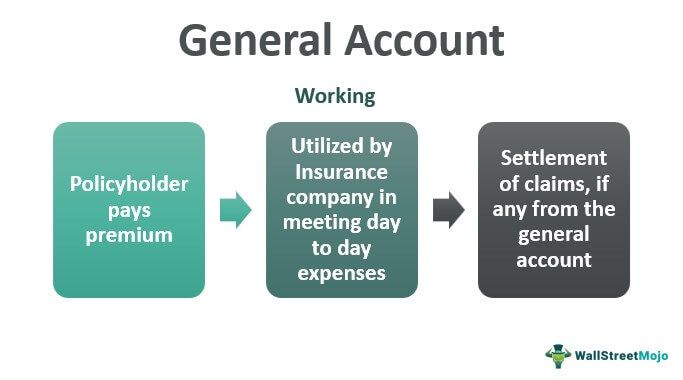

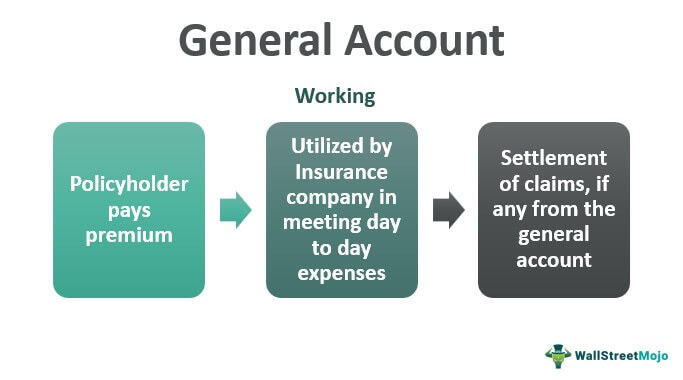

How Does it Work?

It starts when the policyholder purchases a policy from the insurance company. After that, one may use the insurer’s premium in the following manner:

- Day-to-Day expenses say administrative expenses.

- Creation of contingency reserve to meet unexpected and uncertain claims.

- Investments in varying assets to match the return and risk.

All the claims backed by individual/separate assets settle through the general account. If the claims arising from the individual or separate account are insufficient, then the residual would be settled through the general account.

Example of General Account

An insured avails motor insurance from the insurance company for 5 years at prescribed charges per the regulatory norms. After a year, the vehicle got damaged and claimed the damages from the company.

The company availed lawyer and surveyor services to assess the claimant’s claim and rewarded the claim after receiving the surveyor’s assessment report.

They paid the claim out of the premiums received from the several insured over the period. The accumulated fund is the general account and is used to settle non-separate claims.

Investment Strategy

Insurance companies follow either of the two methodologies of investing their general fund balances:

- Managing the funds in-house through creating a separate department that takes care of the invested funds’ risk, returns, dividends, etc.

- Outsourcing the functions to an external vendor, who would charge his management fees and manage the funds.

Many companies prefer the latter due to increased cut-throat competition. Corporations feel that they should focus on their core activities and outsource the non-core functions to the third party, meeting the liabilities of the policyholders as and when they accrue.

The companies also look for their risk appetite as policyholders’ claims can arise anytime, so companies must ensure that their liquidity is at their disposal. As a result, they prefer to invest their general account funds in debt or fixed income investments compared to the companies’ stock.

Debt would ensure the consistent inflow of the funds and would be less risky than investing in the companies’ ownership.

General Account vs Separate Account

| Basis | General Account | Separate Account |

|---|---|---|

| Definition | It is an account where funds of the insurance company are utilized for payment of day-to-day expenses and are not attributable to any specific claim or policyholder. | It is an account held separately from the general pool of assets and used for the purpose for which it has been created. |

| Annuity | Here, funds are invested for fixed annuities. | Here, funds are invested for variable annuities. |

| Risk Involvement | The risk is less, as the investment is in fixed-income securities. | The risk is more, as the investment is in those securities which tend to give variable returns. |

| Creditors Stake | The fund is entitled to the first claim of creditors. | The fund is not entitled to the first claim of creditors as it can’t be used as collateral. |

| Return | It gives you a certainty of the returns as the fund is majorly invested in the fixed income securities of the company. | Uncertainty is more as the fund is invested in the stock market. |

| Loss / Gain of the Stock Market | It is unaffected by the ups or downs of the stock market. | It is affected by the ups or downs of the stock market. |

Conclusion

Unless there is a statutory requirement or insured specific mandate, the premiums received from the policyholders pool in a general fund are applied against meeting day-to-day expenses and invested in the fixed income funds. The company needs to maintain good liquidity in general funds as the claim can arise anytime, unlike separate accounts, where there is a certainty for the tenure of the liability.

Recommended Articles

This article has been a guide to what is the general account and its meaning. Here, we discuss how a general account works, an example, and its differences. You can learn more about accounting from the following articles: –