Part of our Revenue Recognition guide

Accrued Revenue Meaning

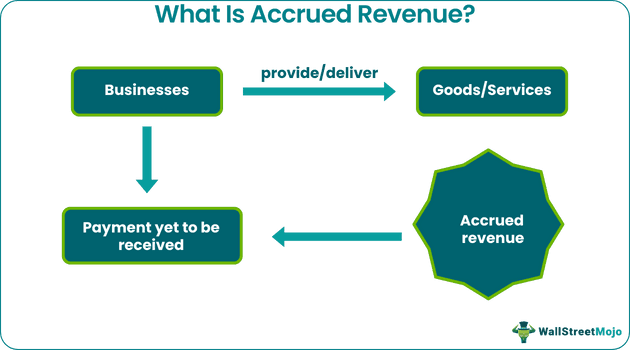

Accrued revenues are the revenue that the company has earned in the normal course of business after selling the goods or after providing services to a third party, though the payment has not been received.

Though the money is yet to be received for the goods and services provided, the businesses know that they would receive it at a later date as their service is already delivered. Hence, the cash inflow here is almost guaranteed, This makes the accrued revenue be considered an asset on the balance sheet of the company.

Accrued Revenue Explained

Accrued revenue is a part of the sale recognized by the seller but not yet billed to the customer. This concept is mostly used in businesses where revenue recognition is delayed for an unreasonable longer period.

It is common in industries where billings to customers are delayed for several months until a designated milestone is reached (in terms of percentage completion) or until the end of the project. However, it is much less commonly used in manufacturing businesses, where invoices are usually issued as soon as products are shipped.

Video Explanation of Accrued Revenue

Examples

Let us consider the accrued revenue examples with a detailed case study below.

Example 1

XYZ International is having a consulting project with one of its large clients, under which the agreement delineates two milestones for billing, after each of which the client owes $60,000 to XYZ as the agreement is such that it only allows for billing at the end of the project for $120,000. Therefore, XYZ must create below is the accrued revenue journal entry to record reaching the first milestone:

| Debit | Credit | |

|---|---|---|

| Accrued Billing | 60,000 | |

| Consulting Revenue | 60,000 |

At the end of another two months, XYZ completes the second milestone and bills the client for $120,000. XYZ records the following is the journal entry to reverse the initial accrual and, after that, records the second entry for the $120,000 invoice:

| Debit | Credit | |

|---|---|---|

| Consulting Revenue | 60,000 | |

| Accrued Billing | 60,000 |

| Debit | Credit | |

|---|---|---|

| Account Receivable | 120,000 | |

| Consulting Revenue | 120,000 |

Debit balances related to accrued billings are recorded on the balance sheet, while the consulting revenue change account appears in the income statement.

The reverse of deferred revenue, i.e., accrued service revenue, can also arise when customers pay in advance but the seller has not provided services or shipped goods. In that case, the seller initially records a liability for the received payment and later realizes the sales related to the same when the transaction is completed.

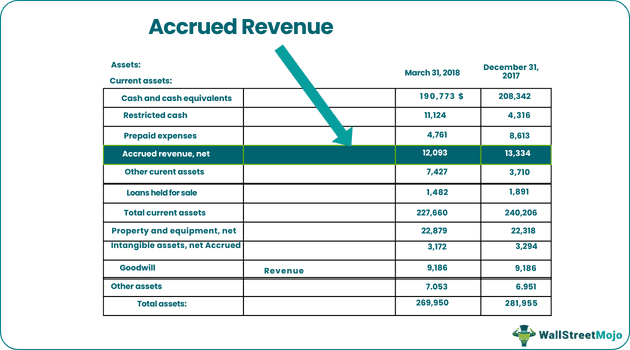

Example 2

To check how the accrued revenue journal entry is made, let us have a look at the example below:

Redfin Corporation reported such accrued revenue of $12.09 million in the March’18 quarter and $13.3 million in the December’17 quarter.

How to Record?

Accrued revenue is shown as an asset on the balance sheet, but it’s not always as valuable an asset as liquid cash. It takes effort related to billing and collection from the customer to convert it into cash. Having large amounts of accrued revenue can adversely impact the working capital cycle. It can be a sign that a company isn’t efficient in getting its customers to pay for its services.

This concept is required to match revenues with expenses properly. The absence of accrued revenue may present excessively low initial revenue and low-profit levels for a business, which does not indicate the true picture of the entity. Also, not using such accrued revenue may result in lumpier revenue and profit recognition as revenues are only recorded when invoices are issued, typically after longer intervals.

Accrued Revenue Vs Deferred Revenue

The difference between accrued and deferred or unearned revenues are listed below:

| Category | Accrued Revenue | Deferred Revenue |

|---|---|---|

| Definition | Goods and services have been provided, but payment is yet to be received | Payment is received, but goods and services are yet to be provided |

| Included as | Included in the accounts receivables listings | Not recognized as revenues in the income statement, but categorized as deposits |

| Status | Earned but not received | Not considered real revenues as they don’t affect income or loss recorded |

| Recorded | Qualifies as asset | Entered as a liability on the balance sheet |

| Entry | Debit entry or increase interest receivable, and credit entry or increase interest revenue as recorded in the income statement. | Debit or increase cash, and credit or increase a deposit |

Recommended Articles

This article has been a guide to Accrued Revenue & its meaning. Here we explain vs deferred revenue & how to record it along with examples to show its journal entry. You may have a look at these recommended articles below to learn more about accounting –