Part of our Banking Services and Operations guide

What Is Bank Identification Number (BIN)?

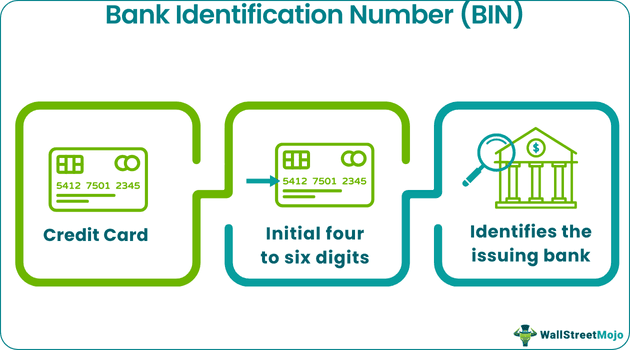

A Bank Identification Number (BIN) refers to a payment card’s initial four to six digits and it identifies the issuing financial institution of that card. The primary purpose of a Bank Identification Number (BIN) is to identify and categorize financial institutions and payment card types.

Moreover, it aids a point-of-sale terminal in authorizing transactions upon swipe of a card. BIN helps users locate the issuer and its industry. The American Bankers Association manages the BIN. Its use has been helpful in lending trust, smoothness, and speed to online transactions. Furthermore, it secures online transactions, identifies stolen or fraudulent cards, and prevents identity theft.

- A Bank Identification Number (BIN) comprises the initial 4-6 digits on a payment card, identifying the issuing bank while detecting fraud and preventing identity theft.

- To find the BIN details of a payment card by conducting BIN database research, punching the first six digits, checking and matching the results, verifying the information, and remaining updated

- It can be protected against fraud by employing strong measures like robust passwords, two-factor authentication, secure site usage, phishing awareness, vigilant card monitoring, and prompt bank reporting.

- The importance of this number includes card issuer verification, fraud prevention, heightened protection, streamlined payment processing, and regulatory compliance.

How Does A Bank Identification Number Work?

A Bank Identification Number is a unique numeric code embedded within a payment card’s first six or four digits. The American National Standards Institute (ANSI) gave the concept back in the 1970s concerning the six-digit code in credit cards. The International Organization for Standardization (ISO) & ANSI contributed to developing it fully. Thus, the six digits of BIN give the following information:

| 1st digit | Industry identifier |

| 2nd,3rd,4th,5th, & 6th digits | Card-issuing institution identifier |

It begins when a cardholder starts a transaction at a merchant counter by swiping their card. The merchant extracts the BIN number and identifies the industry and the card issuer. Hence, it immediately knows whether to accept the card or not. Plus, it also gets to know the exact payment gateway for the transaction to happen.

Moreover, all this happens in an automated manner in a blink of a second. Furthermore, the merchant immediately contacts the issuing bank for card validity and debit of the amount from the account. The transaction is authorized and completed if the bank or the institution issuing the card validates it. Hence, if the transaction is approved, the payment system processes it, deducting the purchase amount from the cardholder’s account or extending credit.

During this time, it also verifies the card’s authenticity to prevent fraud. Besides, the merchant can also detect any fraudulent number coding related to scam activity on the card. Thus, BIN has enabled accurate, faster, smoother, and secure card and online transactions. It has also expanded transactions to a global level using payment cards. Hence, the BIN also provides the card issuer’s location or country of origin.

BIN has become an integral part of electronic payments globally. It has safeguarded the accounts of customers without fail.

How To Find?

One can utilize the following steps to find the BIN details of a payment card:

- Conduct BIN database research: First, conduct a bank identification number search for online BIN to get a bank identification number list of different banks. One can take the help of these databases – BankBinList, Bindb, and BINbase. Then, try to access these databases through the authorized provider.

- Observation: Then, closely look at the number printed on the payment card. Note down the first six digits of the card representing the BIN.

- Punch the first six digits: Enter the card’s six in the BIN database search option. Check and match the results. After that, thoroughly check the results containing the matching BIN numbers. Focus on the accurately matched result, which details card issuer details. Details like bank or institution name, card type, card category, issuer category, and country of origin or location will be available at the user’s disposal.

- Verification: Once one gets the exact information and details of a card, it must be cross-verified from other sources. One may directly contact the card issuer to confirm the search results.

- Remain updated: One must regularly check the database of BINs as they change over time.

Hence, the BIN is sensitive information that helps identify the issuing bank, and it is a critical component of payment card security and transaction processing.

Examples

Let us use a few examples to understand the topic.

Example # 1

Let’s say Jason is a merchant running an online store. In his store, a customer is about to complete a purchase using their credit card. As they enter their card details on his website, Jason notices the first six digits of the card number, which he identifies as the Bank Identification Number (BIN). The BIN reveals that a renowned bank issued the card in this hypothetical scenario.

With this information, he efficiently routes the transaction to the appropriate payment processor associated with that bank, ensuring his customers a seamless and secure payment experience. Furthermore, the BIN aids in fraud prevention efforts, allowing him to cross-reference the card’s details with known patterns of fraudulent activity associated with specific BIN ranges.

Example # 2

Let’s say Karen is a fraud analyst at a credit card company in the US. She has been alerted to suspicious transactions involving a particular BIN. Upon further investigation, she discovered that multiple cardholders with identical BINs quickly made large purchases from various online electronics retailers. Hence, the BIN is traced back to a smaller regional bank. Furthermore, her extended team promptly contacted this bank, which confirmed that several of their customers had reported unauthorized transactions.

Therefore, with this BIN information, she quickly isolates the issue, blocks the affected cards, and collaborates with law enforcement to apprehend the individuals responsible for the fraud. Therefore, this example illustrates how this data can be instrumental in detecting and mitigating fraudulent activities and safeguarding cardholders and financial institutions.

How To Protect BIN Against Fraud?

Protecting Bank Identification Numbers (BINs) against fraud is crucial to maintaining the security of payment card transactions and safeguarding the financial interests of cardholders and institutions. Here are some strategies and best practices for protecting BINs against fraud:

- Using strong security measures: Cardholders must use a solid password for the card and enable two-factor authentication for online transactions.

- Enter card details on secure websites: Card details must be entered on a secure webpage using an SSL certificate. Also, the website must be the authentic website of the merchant, the bank, or the card issuer.

- Be aware of scams and phishing: All phishing emails and SMS must never be opened. Also, any link contained therein must not be clicked. Any phone call or caller asking for card details must never be trusted or blocked immediately.

- Regular monitoring of cards: One must constantly monitor their payment cards to check for any fraudulent activity.

- Secure Transmission: Ensure BIN data transmitted between systems is encrypted using secure protocols (e.g., HTTPS) to prevent interception during transit.

- Third-Party Vendors: If one uses third-party vendors for payment processing or card-related services, ensure they adhere to strict security practices and comply with industry standards.

- Customer Education: Educate cardholders about best practices for protecting their cards and PINs. Encourage them to monitor their account statements for suspicious activity.

- Reporting to the bank: Any phishing call, email, or SMS asking for card details or suspicious transactions must be reported immediately to the card issuer.

Importance

It has become pertinent in the financial domain to use BIN. Hence, let us know its importance as noted below:

- Card issuer verification: It helps identify and verify the card issuer, allowing them to confirm the genuineness of the transaction by the payee.

- Fraud detection and prevention: By knowing the information contained in BIN, merchants and financial institutions prevent fraud.

- Increased protection: BIN acts as an additional layer of protection for cards. It facilitates smoother, faster, and safer transactions.

- Knowing card types and features: Merchants and retailer can tailor their business according to the card type and sector of the card issuer.

- Streamlining of payment processing: Through its ability to grant genuineness, valid card issuer, and authentic transactions, it facilitates the payment process.

- Improved customer experience: Due to the extra security layer offered by BIN, customers have improved payment and shopping experience using their cards.

- Reward points: Some card issuers allow the usage of BIN numbers for getting rewards while using them for shopping.

- Risk Management: Financial institutions and payment processors use BIN data to assess risk associated with particular cards or regions, allowing them to adjust their risk management strategies accordingly.

Hence, customers can now use it without fearing domestic or international transactions. Businesses can now trade globally with confidence and safety.

Frequently Asked Questions (FAQs)

Frequently Asked Questions

1.How is a BIN used in credit card transactions?

<p>The BIN serves the purpose of identifying the originating bank or financial institution during a credit card transaction. Hence, this aids in verifying the card’s authenticity, determining whether it is a debit or credit card, and pinpointing the geographic region associated with the issuing bank.</p>

2.Can BINs be used to identify the cardholder’s personal information?

<p>No, BINs do not reveal personal information about cardholders. Instead, they solely encompass information regarding the card type, origin, and the issuing bank or financial institution. The BIN, in its essence, remains detached from any personal data linkage.</p>

3.Can BINs change over time?

<p>Certainly, BINs have the potential to change over time due to factors such as banks merging, acquiring competitors, or introducing new cards. Merchants and payment processors must refresh their BIN databases regularly to ensure the precise handling of credit card transactions.</p>

Recommended Articles

This has been a guide to what is Bank Identification Number. Here, we explain its importance, how to find it and protect it against fraud, and examples. You can learn more about it from the following articles –