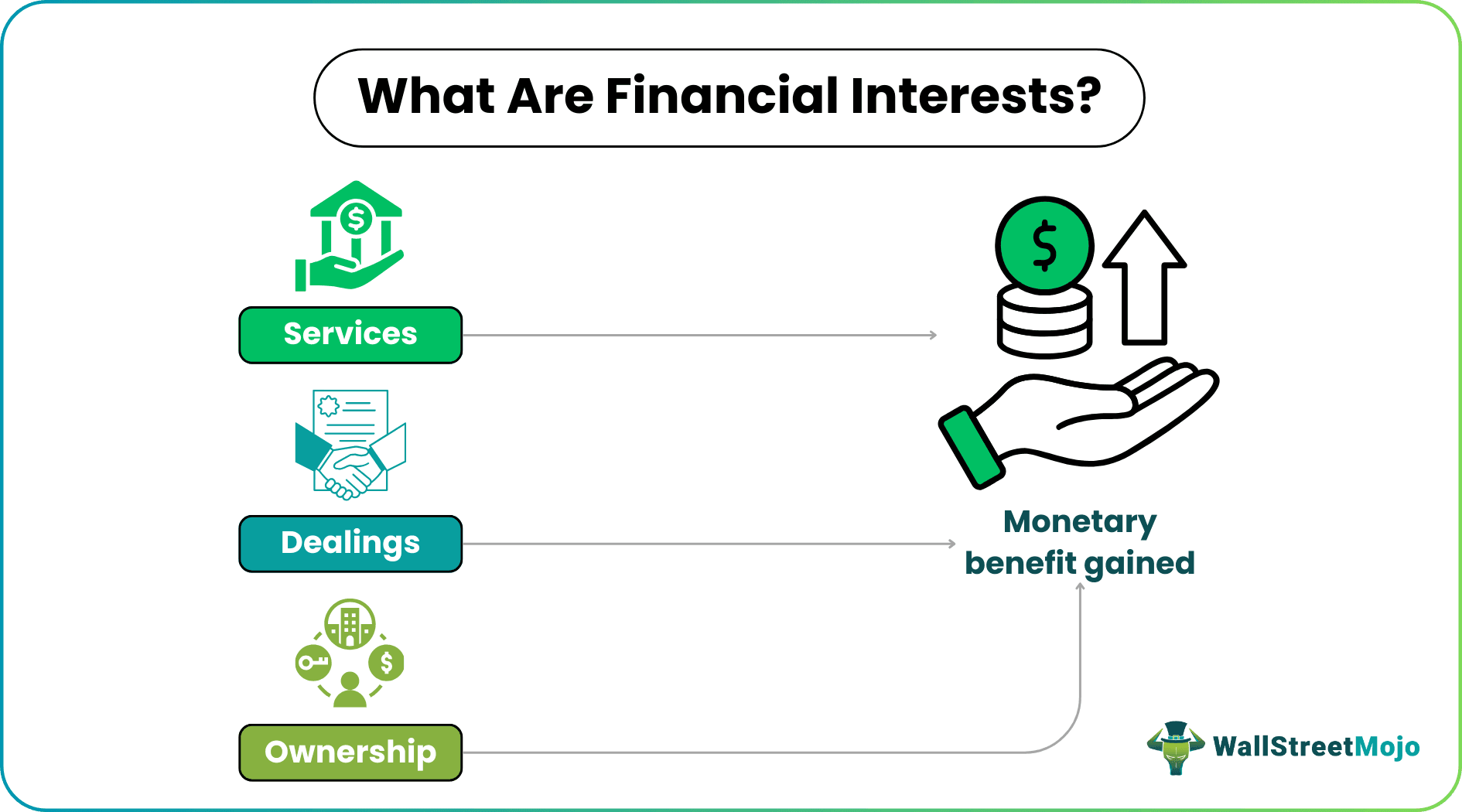

Financial Interest Definition

A financial interest is a monetary gain, or reward realized for providing a certain service, dealings, or ownership. Such benefit can be of a noticeable value for the individual, their family members (spouse or dependent children), or their business entity.

A person is restricted from holding any form of financial interest beyond a specific limit with an entity if they have expertise in the same area. Like an auditor, their family, team, or business entity should not possess a direct or indirect financial interest in an attest client.

- A financial interest is a monetary profit, gain, or benefit derived by an individual, their family, or their firm from providing services, dealings, or ownership.

- It includes profit from commercial dealings, profit on goods sold, shares, gain from intellectual property rights, etc.

- Such a personal benefit held directly or through an intermediary like a trust or estate possesses a significant self-interest threat to the entity.

- The direct interest states that the individual can directly influence the investment decision or control the investment vehicle. While indirect interest is when it cannot control the investment vehicle or affect the investment decision.

Financial Interest Explained

A financial interest can be anything that has a monetary value helped by an individual or a group of people. Such interest can be anything, including salary, profit on stocks, or gain from commercial dealings. Also, such a gain or benefit can be derived through an intermediary such as a trust or estate.

A professional such as a public accountant or an auditor renders services to several business entities. Thus, they are entrusted with the firm’s critical financial information, assets, and money. However, they must follow a certain ethical code of conduct regarding their financial interest in the entity.

A service provider should keep their personal assets separate from the client’s. Hence, an individual rendering any service to an entity cannot use the client firm’s assets or information for personal benefit, whether financial or non-financial. Moreover, such a person should be able to disclose any income, profit, gain, or dividend derived in this context.

According to the International Ethics Standards Board for Accountants, if an auditor, their team member, their family, or their firm possesses any direct or indirect monetary interests with the audit client, it may result in a significant self-interest threat. However, the degree of significance relies upon the following:

- Position or role of the individual having the interest,

- Direct or indirect nature of interest, and

- Financial interest materiality.

Examples

Some examples to understand what is financial interest are discussed below:

Example #1

Suppose Mr. A is a public accountant. The authorities require him to list his spouse’s and firm’s financial interests with his various clients or affiliation in the past 12 months. His Disclosure Statement of Financial Interest states the following:

| Company | Financial Relationship |

|---|---|

| Company A | Major Equity Owner |

| Company B | Royalty Income |

| Company C | Grant |

| Company D | Founder |

In the above example, since Mr. A has a significant financial interest in the company A and D, it may lead to a conflict of interest and termination of his affiliation as a public accountant with these companies.

Example #2

Suppose an auditor has been in a professional relationship with a company for years. Her spouse owns a 57% stake in the client firm. Then such a condition results in a conflict of interest.

Example #3

The dependent daughter of a company’s professional accountant draws a salary from the business without providing any such services.

Example #4

Let’s say an entity’s auditor engages and mediates in the real estate dealing of the firm. Out of such dealing, he makes a gain of $25000.

Example #5

Suppose a public accountant renders accounting services to a business entity. However, an employee of the public accountant’s firm derives royalty income from the audit client.

Direct And Indirect Financial Interest

A person, their family, or their firm is said to have a direct interest in the client firm if:

- Any monetary gain derived directly by influencing an investment decision, or

- Any benefit received through the investment vehicle, estate, or trust over which the beneficial owner has complete control (including the intermediary, which is controlled on a discretionary basis).

The indirect financial interest is acquired when:

- An individual makes a monetary gain while not being in a position to influence the investment decision, or

- A profit derived through an intermediary, I.e., investment vehicle, trust, or estate, which the beneficial owner does not directly control.

Threats

A significant financial interest of a professional accountant, auditor, or any other designated individual with the entity may lead to the following threats:

- Self-interest: influencing the judgment or conduct unethically,

- Self-review: Deliberate effort to manipulate the self-review,

- Advocacy: Compromising the accounting purpose while alleviating the client’s position unreasonably,

- Familiarity: Being sympathetic towards the client while overlooking the facts, or

- Intimidation: Pressure from the management to subside the facts.

The nature of interest determines the degree of self-interest threat it poses to the entity. An auditor must follow ethical conduct while determining their financial interest in the audit client. If an auditor is found to have an unreasonable financial interest in their client, it may result in the termination of their attestation engagement or professional relationship.

Frequently Asked Questions (FAQs)

1.What are the different types of financial interest?

Some of the different kinds of financial interests include:

· Salary or wages

· Profit on shares

· Profit on goods sold

· Gain from intellectual property rights

· Gain from real estate dealings

· Profit on foreign exchange

· Monetary reward from a bank for being their customer

2.What is significant financial interest?

An individual is said to hold significant interests if their total remuneration realized from a publicly traded company in the twelve months before disclosure when added to their equity interest in the company surpasses $5000 as of the date of disclosure.

3.What is a financial conflict of interest?

The financial conflict of interest arises when an individual’s professional judgment or decision in the workplace is driven by their significant financial interest or personal Gain. Moreover, when a person has a financial interest in more than one company, it may also result in a conflict of interest.

Recommended Articles

This has been a guide to Financial Interest and its definition. Here, we explain direct and indirect financial interests, its examples, and threats. You can learn more about it from the following articles –