Part of our Banking and Financial Institutions guide

What Is A Bank Run?

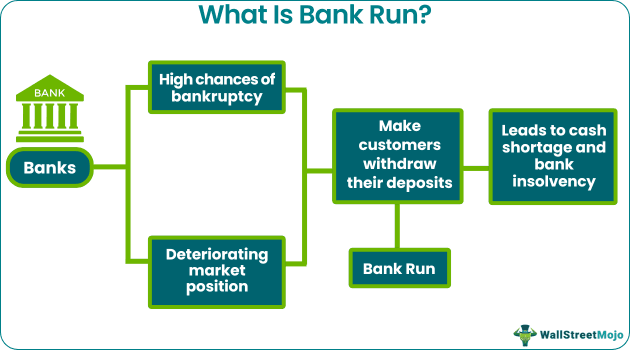

A bank run occurs when a bank or other financial institution runs out of funds due to depositors withdrawing all of their money for fear of losing it. Investors do so if they learn about the banks’ struggle to stay afloat in the market and their increased possibilities of going bankrupt.

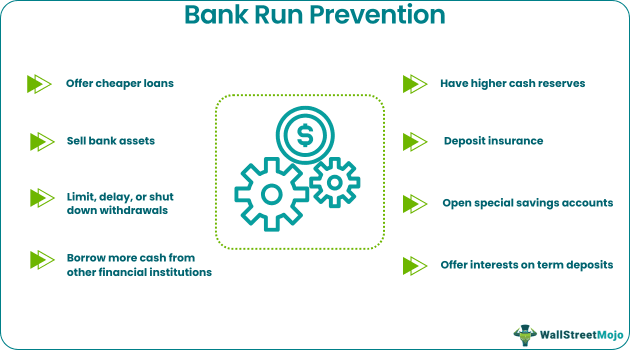

Banks only keep a small amount of cash on hand due to security reasons. So, they do not have enough tangible money to meet withdrawal demands. As a result, when more people request withdrawals from their accounts, banks run out of funds and risk defaulting or going bankrupt. Banks can prevent it by offering loans, selling assets, and limiting withdrawals.

- A bank run meaning describes a situation when a bank or financial institution runs out of funds due to depositors withdrawing all of their money out of fear of losing it.

- Consumers do so after knowing about the banks’ struggle to stay afloat in the market due to fractional cash reserve and their high chances of going bankrupt.

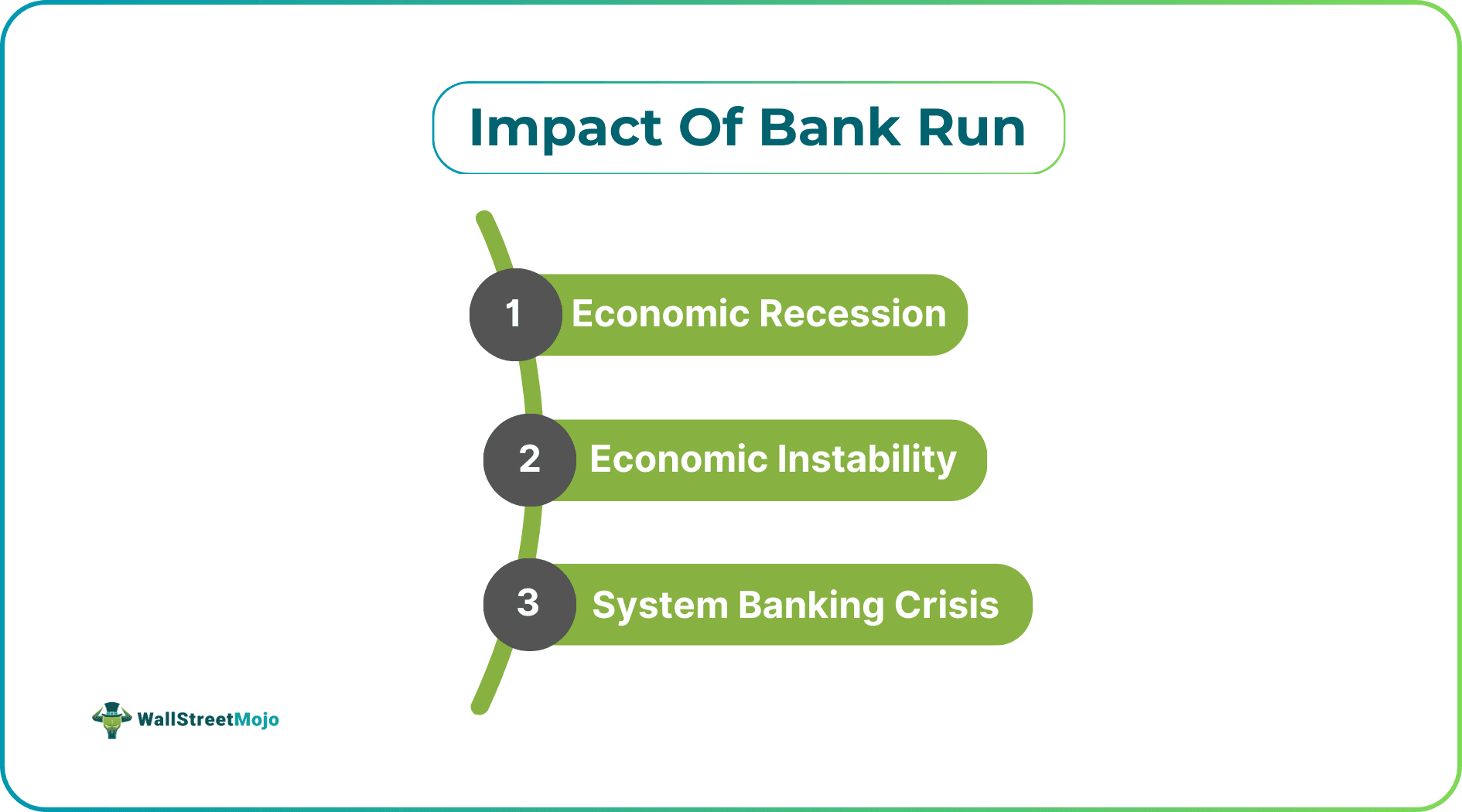

- When numerous banks face the same problem simultaneously, panic sets in, culminating in an economic downturn, economic instability, and a systemic banking crisis.

- It can be avoided by banks providing loans, selling assets, limiting withdrawals, and borrowing more capital from other financial institutions.

Bank Run Explained

Bank run has been a common occurrence both in the past and present. Whether it is the U.K.’s Northern Rock bank run or India’s ICICI bank on the run, customers have proven how they can make or break any financial institution over security concerns. Banks continue to run smoothly as long as their customers feel secure. The game progressively ends as soon as people question banking or financial institutions. This negative investor sentiment influences depositors, resulting in more withdrawals and bank failure.

People put their extra cash in the bank to ensure that they have a certain amount of money saved for when they need it. Financial institutions use these deposits to offer loans and mortgages to borrowers.

Investors feel insecure if they are unsure about the stability of entities whom they are entrusting with their money. As a result, they quickly begin withdrawing the deposited funds out of fear. They either keep the cash or deposit it in another bank or invest it in securities or precious metals. When a few consumers request withdrawals, it has little impact on the institution. However, if many customers request their funds simultaneously, the banks will suffer.

What Causes Bank Run?

One of the major factors contributing to the bank run is the spread of the fear of losing out on their deposited cash. It makes customers act immediately without even verifying the news.

Fractional reserve banking entails a bank keeping only a portion of the money deposited on the premises. As a result, when numerous consumers withdraw their funds simultaneously, they lose the available physical money. It leads to a significant cash shortage, which pushes the bank into insolvency.

When multiple banks confront the same situation simultaneously, bank panic ensues, resulting in economic recession, economic instability, and a systemic banking crisis.

How To Prevent Bank Run?

Some of the common practices adopted by banks and financial institutions to prevent bank runs are as follows:

- Selling assets to increase cash availability inside the facility

- Imposing withdrawal limitations or prohibiting withdrawals entirely

- Borrowing more money from other banks, financial institutions, or the central bank

Besides these, the government may step in to prevent banks from defaulting in various ways, such as:

- Setting higher cash reserve requirements

- Bailing out of banks

- Implementing oversight and regulation

- Introducing deposit insurance schemes

History Of Bank Run

Many incidents in history reveal that banks were compelled to stop operating due to consumer insecurity, for example:

Great Depression Of 1929

The Great Depression started with the United States stock market crash in October 1929 due to the overconfidence of banks and investors. Following the most stable financial period of the 1920s, banks started giving bank credits without any strict criteria. They offered loans even to those with poor credit scores. The general public began borrowing money from banks and spending on stocks without any limits due to the economic growth worldwide.

At the same time, industry productivity began to deteriorate, resulting in job losses. As a result, depositors withdrew their money from banks and held actual cash, resulting in a drop in consumer investment and spending. All of this resulted in fear among banks and the general public. Eventually, banks liquidated debts and sold assets to accommodate the withdrawal demands.

Agricultural Overproduction

This scenario significantly impacted share prices, causing the U.S. financial market to slow and fall. As a result, GDP plummeted, and the U.S. economy was devastated. Fearful of the banks’ default, the public began withdrawing their cash, resulting in the bank run of 1929.

Deposit Insurance

The Federal Deposit Insurance Corporation (FDIC) came into existence in 1933 following these incidents. Its purpose was to keep track of, control, and secure the public’s money through deposit insurance. In addition, it aided commercial banks in dealing with the cash crisis while also preserving public trust in the banking system.

The deposit insurance scheme protected depositors’ hard-earned money, helping them trust entities after the Great Depression. In the event of bank failure, the FDIC transitioned the deposits in the savings accounts to a different bank or auctioned the bank’s assets to make sure the physical money of the customers could be returned.

Examples Of Bank Run

Let us understand the concept better with the following bank run examples:

Example #1

Stella learned that Bank A, where she maintained a savings account, gave loans to people with poor credit scores. Out of the panic created, she noticed that many customers were withdrawing their deposits and relocating them to other financial organizations. But Stella was aware of how the Federal Reserve has already safeguarded the funds of its consumers through insurance plans.

As a result, she did not make any move despite hearing how unstable her bank was becoming every day. In addition, she made sure that the people she knew were aware of the government’s protection measures for bank deposits.

Example #2

Besides the Great Depression of 1929, the bank run 2008 was another worldwide financial disaster. It was the stock market crash of 2008, which was reminiscent of the Great Depression.

Banks began extending home loans to persons with bad credit and inability to repay during this period. This economic crisis in 2008 resulted in a housing bubble, which was quite comparable to the 1929 asset bubble.

Frequently Asked Questions (FAQs)

Frequently Asked Questions

What is meant by bank run?

u003cpu003eThe term u0022bank runu0022 refers to a circumstance in which banks run out of funds due to depositors withdrawing all of their money for fear of losing it. When numerous customers withdraw the same amount simultaneously, banks, which store only a fraction of the total deposited amount on the premises, begin to lose their accessible physical money. It leads to a significant loss of cash, putting banks at risk of going bankrupt.u003c/pu003e

Is a bank run possible today?

u003cpu003eNo, the establishment of the Federal Deposit Insurance Corporation (FDIC) in 1933 and other regulatory measures after the Great Depression ensured the security of bank deposits. It introduced an insurance scheme for banks to protect their clients’ hard-earned money. In a bank failure, the FDIC transfers savings account deposits to another bank or auctions the bank’s assets to ensure that customers’ tangible money is restored.u003c/pu003e

What measures do banks adopt to take control over bank runs?

u003cpu003eHere is a list of means that the banks use to prevent such a situation:u003cbr/u003e- Lengthening the withdrawal time or shutting down the processu003cbr/u003e- Setting cash reserve requirementsu003cbr/u003e- Insuring depositsu003cbr/u003e- Borrowing money from other financial institutionsu003cbr/u003e- Opening special savings accounts to exchange paper money with consumer holdings at a fixed rate of interestu003cbr/u003e- Offering interest on term depositsu003c/pu003e

Recommended Articles

This has been a guide to what is a Bank Run and its definition. Here we explain how the bank run works, its history, causes, prevention, and examples. You can learn more from the following articles –