What Are Non-Performing Assets (NPA)?

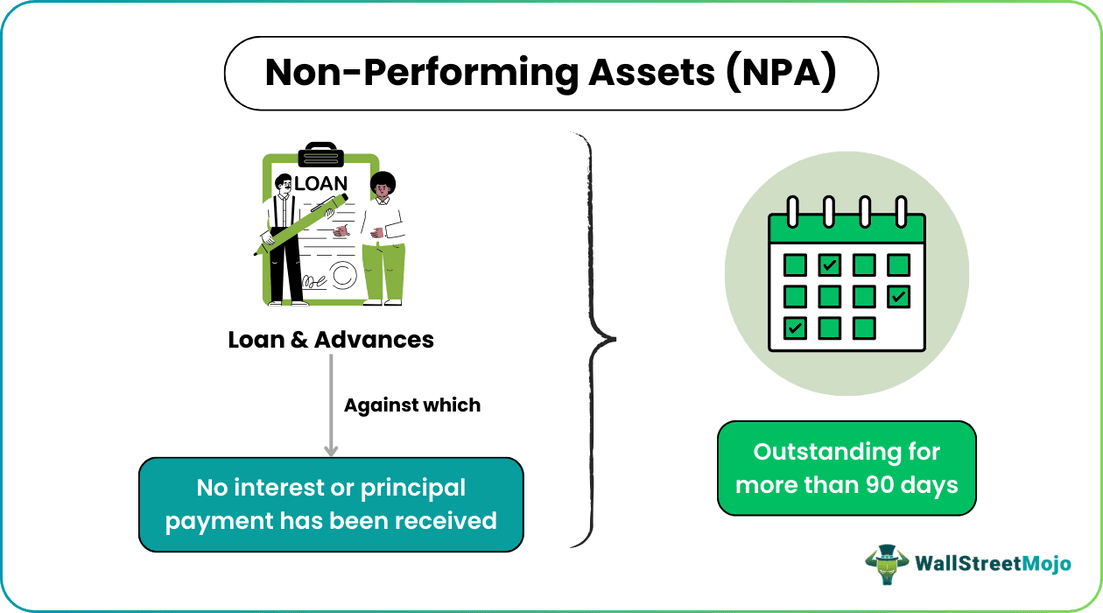

Non-performing assets (NPA) refer to the classification of loans and advances in the books of a lender (usually banks) in which there is no payment of interest and principal has been received and is “past due.” In most cases, debt has been classified as NPAs where the loan payments have been outstanding for more than 90 days.

NPA is generally classified on the bank’s balance sheet, and the percentage of NPA out of the total advances becomes a vital ratio for the banks to check before making the results public. More than 90 days where payment is due to the banks’ loans and advances move to NPA.

- NPA or non-performing assets refers to outstanding loans and advances in which the borrower fails to pay principal and interest payments to the lender for more than 90 days. In such cases, the lender considers the loan ‘in default’ and classifies it as an NPA in the balance sheet of the financial year.

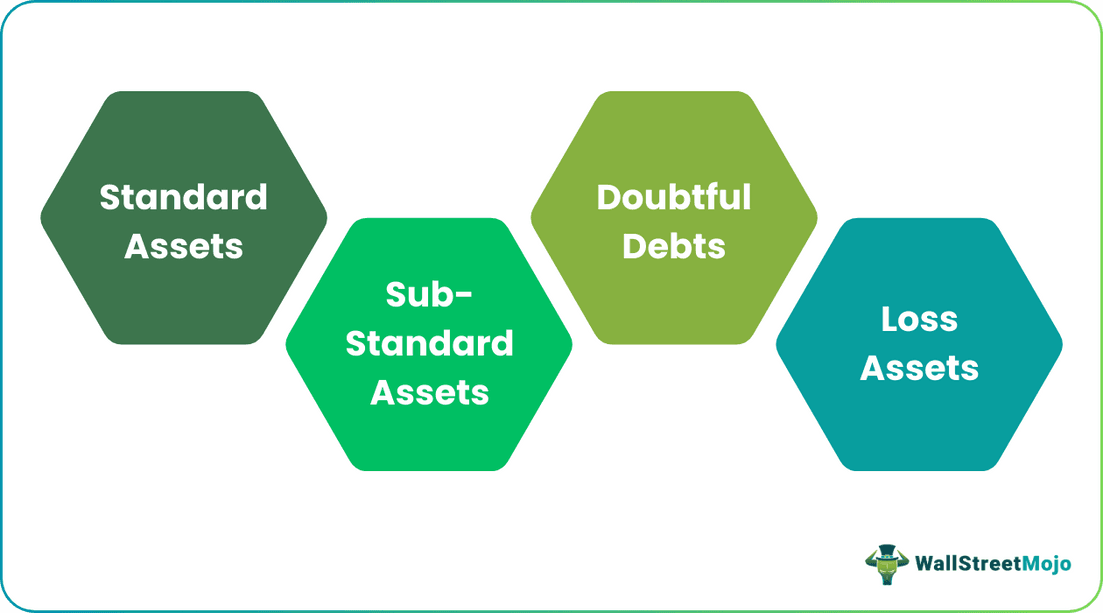

- Banks classify non-performing assets (NPA) into four groups: Standard Assets, Sub-Standard Assets, Doubtful Debts, and Loss Assets.

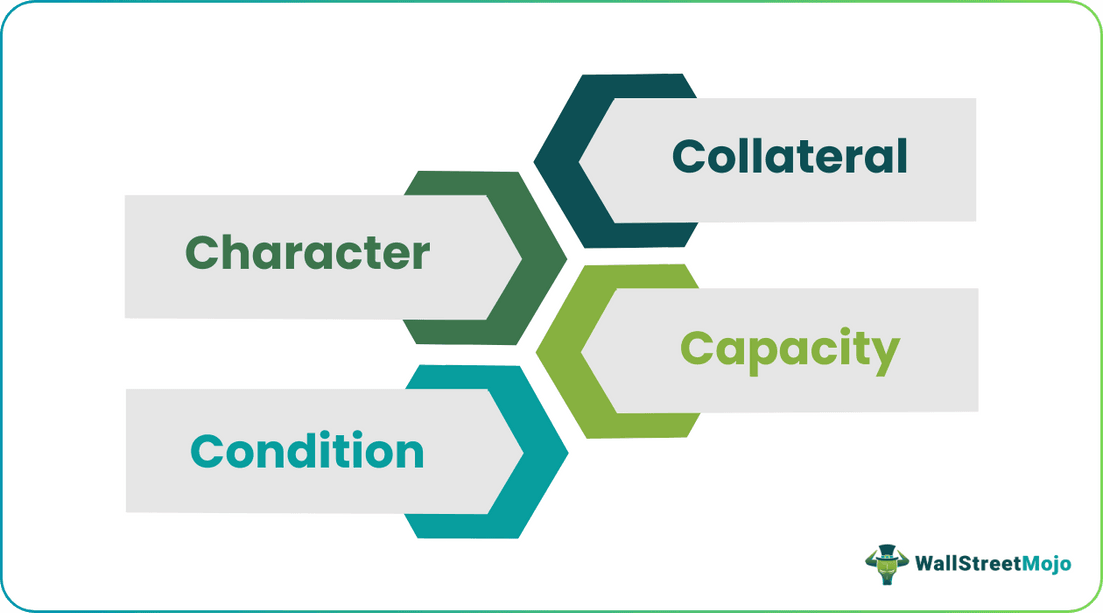

- Before making any loan advances, banks must remember the 4 C’s: Character, Collateral, Capacity, and Condition. Big credit firms analyze any company in the 4 C parameter.

- Banks must check the NPA percentage before publicizing the results.

Non-Performing Assets (NPA) Explained

The non-performing assets are those loans and advances that are given out by financial institutions which are not able to generate revenue in the form of interest and ultimately not collectable by the issuer. The borrower may be an individual of a corporate and the loan amount may vary depending on the purpose. But such loans become a liability in the balance sheet of the issuer because they add to their losses.

They are a result of lack of proper analysis and evaluation of borrowers while sanctioning loans, economic downturn, sudden natural disaster, unforeseen or man-made instability in political or economic situation, interest rate fluctuations etc.

In the term sheet/sanction letter, the period of default under which the loan will be classified as non-performing assets are generally mentioned.

As noted above, Bank of America has an NPA of around $4,170 million accrued for 90 days or more.

It is necessary for every financial institution, engaged in the practice of lending money to maintain a systematic method of risk assessment and detailed evaluation of credit worthiness of the borrower so that the the risk of NPA can be controlled. The lending practices should be sounds and stable with proper transparency so that the far reaching negative impact of such losses can be minimised and the financial system of the economy remains strong.

The Hargreaves Lansdown provides access to a range of investment products and services for UK investors.

Types

For any financial institution:

#1 – Term Loans

A term loan, i.e., a plain vanilla debt facility, is treated as an NPA when the principal or the interest installment of the loan has been due for more than 90 days.

#2 – Cash Credit and Overdraft

Cash credit or a remaining overdraft past due for more than 90 days can be treated as an NPA.

#3 – Agricultural Advances

One of the categories of non-performing assets are agricultural advances that have been past due for more than two crop seasons for short crop duration or one crop duration for long duration crops.

There could be other types of NPAs, including residential mortgages, home equity loans, credit card loans, non-credit card outstandings, and direct and indirect consumer loans.

For Banks

Banks classify the categories of non-performing assets (NPA) into the following type four groups: –

#1 – Standard Assets

Standard assets are those assets that have remained NPA for 12 months or less than 12 months, and the risk of the asset is normal

#2 – Sub- Standard Assets

For more than 12 months, NPA has been classified under sub-standard assets because such advances possess more than normal risk, and the borrower’s creditworthiness is weak. Such advances possess more than normal risk, and the borrower’s creditworthiness is quite weak. As a result, banks are generally ready to take some haircuts on the loan amounts categorized under this. For more than 12 months, NPA has been classified under sub-standard assets. Banks are generally ready to take some haircut on the loan amounts, which are categorized under this asset class.

#3 – Doubtful Debts

For a period exceeding 18 months, non-performing assets come under doubtful debts. Doubtful debts themselves mean that the bank is highly doubtful of the recovery of its advances. The collection of these advances is highly uncertain, and there is the slightest probability of recovering the loan amount from the party. Such advances can put the bank’s liquidity and reputation in jeopardy.

#4 – Loss Assets

The final classification of non-performing assets in banking sector is loss assets. This loan is identified either by the bank itself or an external auditor or internal auditor as that loan where amount collection is impossible, and the bank has to dent its balance sheet. The bank, in this case, has to write off the entire loan amount outstanding or need to make a provision for the total amount which needs to be written off in the future.

Non-Performing Assets (NPA) Explained in Video

Causes

Some common causes of the such assets are as given below:

- Lack of risk assessment – Sometimes, financial institutions do not make proper assessment of the risk involved in lending to a particular borrower, be it an individual or a corporate. They are in a hurry to issue loan which is their main source of return. This may result in NPA.

- Economic slowdown – The economy of a country may face a sudden slowdown due to natural or man-made reasons. This makes loan repayment difficult for borrowers due to fall in income sources, financial stress or inflation.

- Industry downturn – Any specific industry or sector may face downturn due to which there is fall in employment and a negative effect in the overall economy, resulting in inability of borrowers to repay loans.

- Change in interest rates – Due to sudden rise in rates, the loans become expensive. The borrower may find it hard to repay them at increased interest since now the installment amount has increased, resulting in non-performing assets in banking sector.

- Changes in rules – Any regulatory change may affect the borrower’s power to repay or the lender’s ability to collect dues. Thus, any legal process related to bankruptcy or insolvency may lead to NPA.

- Problem in management – If there are problems in either the financial institution who are lending or the borrower company, where management is not strong and skilled enough to handle loan related matters, especially planning and budgeting for loan issue and repayment, it can result in NPA.

Example

In order to understand the concept of non-performing assets let us take the example of the company XYZ has taken a loan of $100 million from the bank ADCB and needs to pay $10,000 of interest every month for five years. If the borrower defaults on the payment for three consecutive months, i.e., 90 days, the bank needs to classify the loan as a non-performing asset on their balance sheet for that financial year.

Guidelines

Following are the things banks need to bear in mind before making loan advances: –

#1 – Character

The borrower’s character needs to be judged, and the willingness of the company to repay debt needs to be evaluated at that time. In addition, they should also consider the management, history, revenue pipelines, stock performance, and media coverage of the company.

#2 – Collateral

In the concept of non-performing assets, the value of the collateral pledged needs to be assessed, and proper valuation of the property/asset should be done, keeping the loan to value ratio in mind.

#3 – Capacity

The capacity of the banker to analyze the company’s financials and the future revenue projections. Also, existing lenders on the company’s balance sheet need to be adequately studied to get the right collateral before providing advances.

#4 – Condition

Lastly, the overall environment and the market and industry conditions should be considered. In addition, a bank should consider external and internal factors that can affect the business in the future.

Big Credit analysis firms judge any company in the 4C parameter.

The banks are the backbone of an economy that needs to strive in a dynamic and challenging environment. Hence, choosing the right clients and business partners will make the economy sustainable and save the world from another 2008 global financial crisis. Furthermore, a proper strategy and restrictions should be implemented for banks to limit credit to only deserving corporations in non-performing assets.

Impact

As a reputed financial institutions, it is necessary to understand and identify the impact of the concept of non-performing assets, in various areas of the economy.

- Profits – Such assets have a direct impact on the profit earning capacity of the institutions, because since the money lent out is not received on time, the main source of revenue is absent. Moreover, a huge amount of fund is blocked which counld have been used for more productive purposes.

- Capital erosion – Every financial institution, which are involved in lending business, has to set aside some funds as provisions to meet any contingency like inability to collect loans. Now if the loans cannot be collected, such funds need to be used to compensate for the losses because now the loans which were previously assets, have now become a liability, leading to capital erosion.

- Lack of liquidity – The loans are a source of revenue for the financial institutions. If they do not perform the function of generating revenue in the form of interest then there is a lack of liquidity in the business which hinders the progress and daily operation. This affects the financial condition because there is less of cash inflow, and fall in asset value.

- Fall in lending capacity – Due to the above point, it is unable to meet its most important function of lending since it has less of liquidity. The funds lent out are not coming back into the business along with extra amount of interest which helps it to run the business in a sustainable manner.

- Economic slowdown – This is a very crucial aspect off the economy. The financial system is its backbone. It plays an important role in creating employment, channelizing resources and promoting economic growth and prosperity. NPAs affect this process leading to lack of funds which hinders economic activity, leading to fall in investment, demand and consumption. This in turn lead to lack of employment and an overall slowdown in in the economy.

- Investors lose faith – It is a common fact that the investors will get attracted towards sectors or industries that are flourishing and helping actively in economic development. If this is absent, investors lose faith and confidence, and do not invest their money in such areas. Thus, the money does not flow freely in the economy, hampering an all round development.

- Damage in reputation -The financial institution that has a huge amount of NPA in its balance sheet is obviously the one which lacks the ability to manage its business and resources in an optimum manner. This creates a negative image of the institution in the market.

Thus, the above points clearly show how such assets that not not produce any value affect both the institution and the country as a whole.

Non-Performing Asset Vs Performing Asset

Both the above terms are related to the fianncil sector whose main business is to lend money to borrowers and earn revenue in the form of interest and reinvest it in the market to maintain sustainability of the business. But let us understand the differences between them.

- The list of non-performing assets arise due to default on loan repayment but the latter is a situation where the loans are repaid on time without any delay or penalty.

- The former is a high risk situation whereas the latter is a situation which helsp in minimising risk and maintaining continuity of business.

- The former indicates financial distress whereas the latter indicates a good financial health.

- The former leads to deterioration of the image, business, profitability and sustainability of the financial institution but the opposite is the case with the latter.

- If the list of non-performing assets continues on a long term basis, it will lead to economic slowdown, lack of investment and hinder growth of the economy. The opposite is the latter, which helps promoting economic growth and development.

Thus, the above points clearly identify the differences between them.

Disclosure: This article contains affiliate links. If you sign up through these links, we may earn a small commission at no extra cost to you.

Frequently Asked Questions (FAQs)

What are the causes of the non-performing assets?

In banking terms, the various causes for the non-performing of assets are –

Inappropriate credit appraisal

Receivables poor recovery

Low-grade loan management policy

Non-success of business

Inactive judicial system

Industrial downturn

Unfavorable exchange rates

What are the examples of non-performing assets?

Overdraft, cash credit facilities, and agricultural loans are non-performing assets.

What are the non-performing assets of the company?

The company’s non-performing assets are cash and cash equivalents, accounts receivable, marketable securities, and trademarks.

What is the difference between performing and non-performing assets?

Performing assets refer to the assets that maintain the cash flow to the lender/investor. In contrast, non-performing assets are those that are unable to make the payment within 90 days.

Recommended Articles

This article has been a guide to what are Non-Performing Assets (NPA). We explain the types with example, guidelines, causes & differences with performing assets. You may also take a look at the below useful articles:-