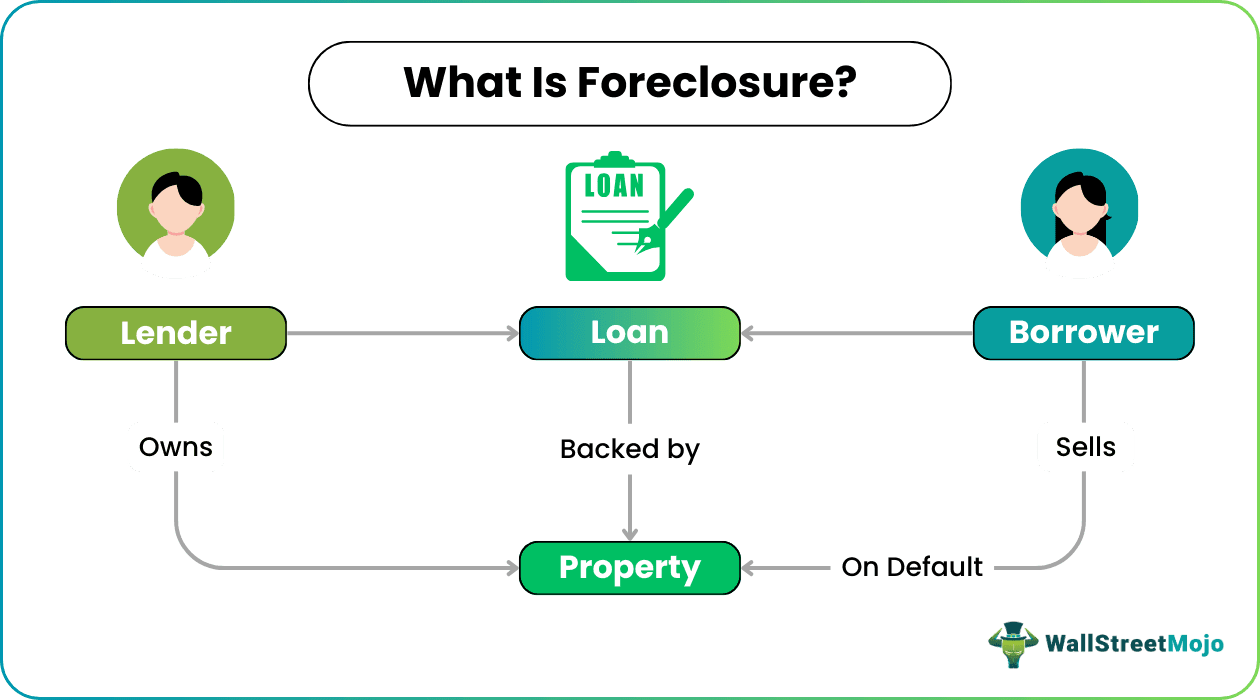

Foreclosure Meaning

Foreclosure is the step that a lender takes when a borrower defaults on loan repayment. The lender takes legal control of the mortgaged property and sells the asset (property) to recover the loan amount.

The process of foreclosure allows lenders to secure their loan amount as they know they have the option to recover their loan by selling a backing property. This process makes lenders engage in a safe deal without any risk involved.

- Foreclosure occurs when a borrower defaults on loan repayment, and the lender takes legal control of the mortgaged property and sells it to recover the outstanding amount.

- There are two types of foreclosure: judicial and non-judicial, and the process may vary depending on the state.

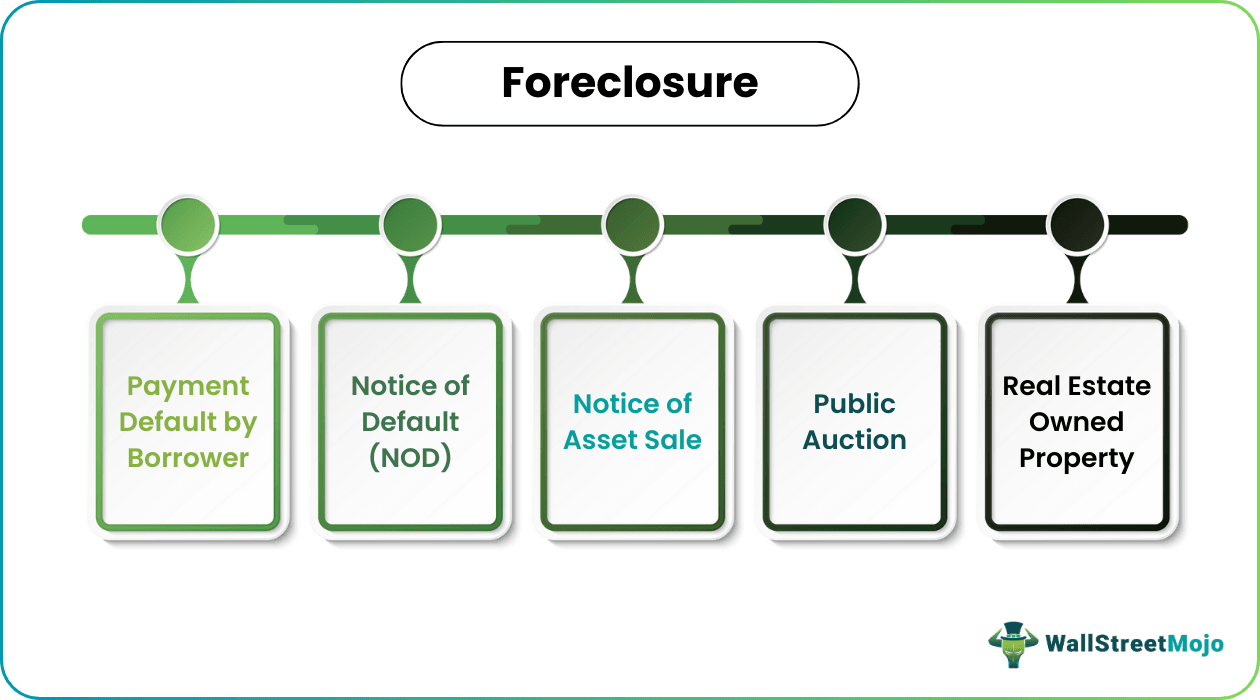

- The foreclosure process typically involves five steps: payment default by the borrower, a notice of default (NOD), a notice of asset sale, a public auction, and real estate-owned property.

- In an emergency, borrowers can request forbearance from the lender to temporarily suspend or reduce payments.

How Does A Foreclosure Work?

Foreclosure on properties allows lenders to have a safe lending setup, whereby they get an option to recover their loan in the event of default at the borrower’s end. The instance of default is normally caused by the non-repayment of the loan, while another reason for default could be the disobeying of the terms and conditions of the mortgage document.

Foreclosure in mortgage is a crucial affair, which follows a specific process. When a borrower misses one mortgage payment, the lender sends a missed payment notification to the borrower. If two consecutive payments are missed, a demand letter is sent. Though the letter signifies a more serious warning, there are chances that the lenders are still ready for settlement. The third missed monthly mortgage payment makes lenders send a notice of default.

Though the foreclosure process varies from state to state, they exhibit five similar characteristics: –

#1 – Payment Default by Borrower

When the borrower misses at least one loan payment, he is put in default criteria. The lender will send a missed payment notice stating that they have missed the payment and even offer 15 days grace period to make the payment. After 15 days, the borrower will be charged a late fee and other penalties. If the borrower misses two to three payments, they will send them a graver demand notice than a missed payment notice.

#2 – Notice of Default (NOD)

When the borrower misses a payment for three to six months, the lender will send a notice of default to the county recorder’s office. A copy of this is also sent to the borrower, who gets 90 days to pay the recent bill and reinstate the loan. This period is called the reinstatement period.

#3 – Notice of Asset Sale

If the borrower still cannot make the payment within 90 days, the lender begins the process of foreclosure. The lender will again send notice to the country recorder’s office about the same with one copy to the borrower and publish legal information in the newspaper for three consecutive weeks before the home gets auctioned. The borrower still has five days before the auction to make the missed payments.

#4 – Public Auction

The lender will estimate an opening bid for the property before the auction. The price is calculated based on the balance of the loan pending and any lien or taxes which are not paid. The property gets sold to the highest bidder. The trust deed is passed on to the property’s new owner, and the borrower now has three days to vacate the property.

#5 – Real Estate Owned Property

If the property is not sold in the auction, it becomes a bank or real estate-owned property. When this takes place, the lender is the property owner, and it will try to get the property sold through a broker or an agent. To make the deal more alluring, the lender may remove some of the lien chargers and other charges, thus giving some form of discount to the interested party for buying the considered property.

The Hargreaves Lansdown provides access to a range of investment products and services for UK investors.

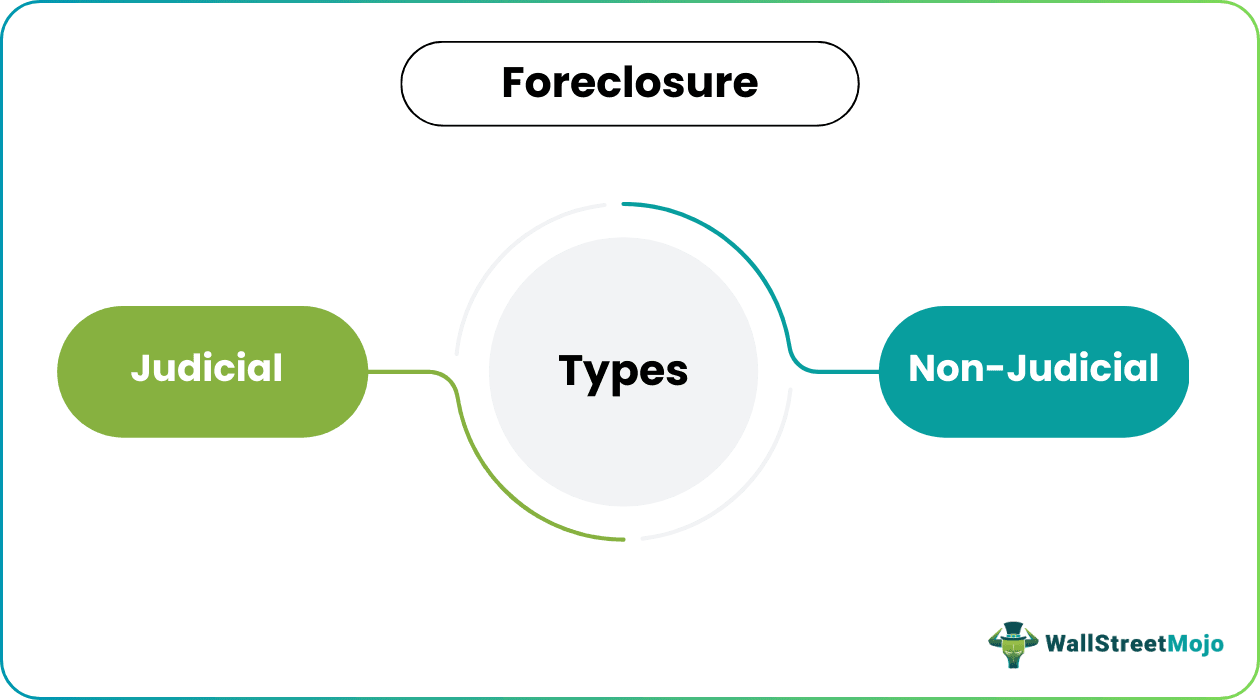

Types

Foreclosures can exist in two forms:

#1 – Judicial

The usual foreclosure happens when a lender informs the borrower of the missed payments. Further, when the borrower fails to revive from default, the lender sues the borrower and files it in the country recorder’s office. Finally, the case is put on public record, and the property gets auctioned after the trial.

#2 – Non-Judicial

Here the lender has full authority to sell the property when the borrower defaults. Here too, the case is recorded in the country recorder’s office, and the borrower gets time to make up for the default failing, which the lender has the right to immediately go for the auction or the sale of the property. Here, the difference is there are no extensive trials or judicial proceedings.

Examples

Let us consider the following examples to understand the foreclosure process:

Example 1

John takes up a loan of $50,000 from Jane, a bank employee. The deal was backed by his old property; hence the latter approved the loan application despite the former having a lesser monthly salary. The borrower missed his payment in one of the months and received the missed payment notice from Jane and made the payment within a couple of days.

A few months later, he missed his repayment for three consecutive months and received a notice of default. Jane finally received the ownership rights over the property and sold it to recover the loan amount.

Example 2

In an auction, the lender generally sets a bid before the auction based on the estimated price, considering the pending loan balance and any lien or taxes that are not paid. This notification is also given in local newspapers and websites for interested buyers to come forward for the auction.

Based on the pre-set bid, auctioneers can bid for prices above it on the auction day. The purpose of the auction is to get the highest possible cost of the property. The person with the highest bid or the amount sufficient for the lender to cover up the loan is considered, and the property gets handed over to the person.

The borrower has three days to vacate the property and hand it over to the new owner. On the other hand, if the lender does not get good bids in the auction, the lender will take over the property and try to sell it in the future through brokers or agents.

How To Stop Or Avoid?

Property holders, though they back their borrowed amount with their property, never want foreclosure. Hence, there are a few ways listed below using which one can avoid or stop foreclosures from happening:

- One most important steps to avoid foreclosure is to prevent missed payments of loans and avoid becoming a defaulter.

- One should take some time from the lender in dire emergencies before coming into trouble with legal action. It is called forbearance.

- If one agrees to never repeat a default, the lender might give the borrower a break and waive the debt forgiveness obligation.

- When the lender spreads out the missed payment amount for a longer duration, it eases the borrower.

- When the lender agrees to change the loan terms or extend the amortization period, this may give some flexibility to the borrower.

Consequences

When foreclosures happen, the consequences can be harsh. A few of them include the following:

- One must let go of their own home, and any equity put forward.

- It brings stress and anxiety because one becomes homeless without knowing where to go next.

- It does a lot of damage to the credit score, and getting a second loan in the future becomes very tough.

- One may owe a deficiency balance even after the foreclosure sale.

- One may lose opportunities for leasing or assistance which may be available further.

- Under the Fannie Mae mortgage process, one will lose the ability to purchase another house for another seven years.

Impact

The implications of foreclosures are as follows:

- It is the credit rating that gets hit drastically.

- Homes get available at a cheaper rate than the actual market price.

- It creates an opportunity for new home buyers to purchase homes with reduced costs.

- Even after foreclosure, the borrower may have to compensate for the deficit in the loan.

- There are problems in employment in certain fields where the candidate’s credit rating is checked.

Advantages

Foreclosures are a plus for lenders. Some of the benefits of the process for the parties involved include:

- When the real estate market falls, many owners will find their house worth a mortgage. In these scenarios, it may be good for owners to reduce their burden and start fresh.

- It is beneficial for new home buyers who find property at cheaper rates.

- It is also a way to save money. When the borrower realizes there is no way to prevent foreclosure, one can stop trying and save the money that was otherwise used for making monthly payments and start over fresh when the foreclosure ends.

Disadvantages

With merits, the process has some demerits as well. Some of them have been listed below:

- The credit rating gets the hardest hit and falls drastically.

- One loses their home, and finding a new home is very difficult in such a crisis.

- It also affects employment where some job credit background of individuals is checked.

- Getting a new loan or mortgage becomes very difficult.

- When foreclosure happens, it increases the tax burden of the borrower. In the eyes of the IRS, the debt is forgiven and considered an income.

Disclosure: This article contains affiliate links. If you sign up through these links, we may earn a small commission at no extra cost to you.

Frequently Asked Questions (FAQs)

1. What is foreclosure vs. preclosure?

Foreclosure involves the lender selling the borrower’s property at a public auction and using the proceeds to repay the outstanding loan amount. On the other hand, preclosure refers to repaying a loan before the due date agreed upon in the loan agreement. This can be done in part or full and can attract some penalties or fees.

2. What is foreclosure vs. repossession?

Foreclosure is a legal process where a lender seizes a borrower’s property, typically a home or a car, due to the borrower’s inability to repay a loan. Repossession, on the other hand, is the process of a creditor taking back an asset used as collateral for a loan. While foreclosure involves selling the property at a public auction, repossession involves the creditor reclaiming the asset and attempting to sell it to recoup the outstanding loan amount.

3. What is foreclosure vs. settlement?

Foreclosure is a legal process where a lender seizes a borrower’s property due to the borrower’s inability to repay a loan. On the other hand, the settlement refers to an agreement between the borrower and the lender to resolve the outstanding debt through a negotiated settlement.

Recommended Articles

This article is a guide to Foreclosure and its Meaning. Here, we explain how it works, how to stop or avoid it along with examples, advantages & disadvantages. You can learn more about corporate finance from the following articles: –