Part of our Banking Ratios & Metrics guide

Bank Reserve Meaning

Bank Reserves refer to the minimum liquidity reserves that every bank must maintain to make sure they never run out of cash if the customer demands the withdrawal of the deposits kept with the bank. The bank reserve ratio might be different for banks from different countries based on their central bank’s regulations.

This reserve is a mandate for banks to ensure that they never have to turn down a customer wanting to make a withdrawal. If such a situation occurs, there might be panic among customers, and trust in the bank’s integrity might take a beating. Central banks also use this ratio to regulate the cash flow in the economy.

- Bank reserve refers to the amount of funds a bank must hold in addition to meeting withdrawals and other obligations.

- Bank reserves are essential because they help ensure that banks have enough funds to meet the demands of their customers and maintain financial stability.

- Central banks set reserve requirements and may vary based on factors such as the size of the bank and the level of risk in the economy.

These reserves can be categorized as required reserves or excess reserves.

How Does Bank Reserve Work?

Bank reserve is a ratio of the cash balance a bank is required to maintain to facilitate withdrawals and other cash requirements. The US Federal Bank Reserve is used to facilitate policies at a macro level whereas, reserve ratios for commercial banks accommodate the cash flow at a micro level or at a customer level.

Bank reserves are the minimum amount of funds held by the banks in cash or vault to ensure regulatory compliance with the federal reserve bank. The key purpose is to regulate the banking procedure and ensure that banks will not go short of funds if any demand liability arises.

The central bank of the country can reduce or increase the reserve ratio as per the state of the economy. For instance, they can reduce the reserve rates for banks to provide more loans, and in situations such as the pandemic where the Federal Reserve initiated a zero reserve to ensure no cash withdrawal was denied to customers in dire situations.

Nevertheless, banks would not want to hold excess cash in their reserves as money sitting idle in vaults would mean no returns on the excess cash. Therefore, banks usually do not maintain cash balances significantly beyond the minimum required percentage.

Classification

Bank reserve ratio can be classified into the required reserve and the excess reserve.

#1 – Required Reserve

The required reserve is the minimum fund banks must hold to meet their deposit liabilities. The Fed has the authority to make changes in the required reserve ratio percentage from time to time.

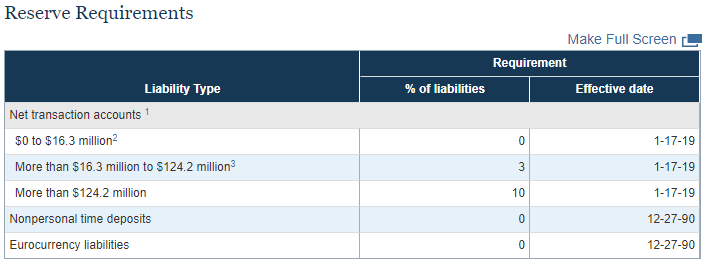

The Fed has updated its required reserve target ratio, which is applicable from January 17, 2019. The updated limits are as follows

(Source: federalreserve.gov)

As per the latest requirements, all the banks having deposit liabilities valuing more than the US $ 16.30 million but less than the US $ 124.20 million must keep 3% of deposits as a required reserve. The banks with deposit liabilities of more than US $ 124.20 million must maintain a required reserve equal to 10% of deposit values.

Further, while calculating the required reserve, the banks consider the net transaction accounts, which means they do not consider the funds due from other banks or transactions that are still outstanding.

#2 – Excess Reserve

The excess reserve is the cash required to keep in the vault over the minimum required reserve. Usually, the banks keep the excess reserve balance at lower levels and lend out the money instead of keeping it in vaults. This is mainly because banks can earn higher returns by lending the funds as compared to the rate of interest offered by the Fed. In the past, the incentives to maintain the excess reserve balances were very low or near zero. However, the excess reserve balance can pile up during crisis scenario financial crisis that happened in 2008, the Fed reduced the reserve target ratios to the lowest possible ceiling in order to stimulate the lending and to initiate economic recovery. However, in 2008, even after the lowest reserve requirements, the banks were not ready to lend due to a high volume of bad debts, and they want to utilize the available cash realized from the reserve holding toward the writing off the bad debts.

During the 2008 crisis, the aggregate of the excess reserves of all the banks shot up to US $ 1.25 trillion (as reported in the Federal Reserve Statistical Release H.3), and the liability side of the Fed’s Balance Sheet increased due to increased reserve balances.

- Instead of allowing the banks to use the funds to write off the bad debt, the fed made a change in its policy in October 2008 and started paying interest on the reserve funds. The interest rate offered was fluctuating with the monetary policy. This unconventional move allowed the Fed to take control of the money market securities and short term interest rates.

Interest Rate

The US Federal bank reserve and the Reserve for other banks are updated every single day for the perusal of banks. This affects every customer of the bank as these interest percentages have an impact on the interest rates levied on loans, maintenance charges, and so on.

The Fed determines the interest rate on required reserves (IORR) and the Interest rate on Excess reserves (IOER). These interest rates get updated each business day at 4:30 pm EST with the interest rate for the next business day.

The latest published interest rate is as follows:

(Source: federalreserve.gov)

Impact of Inflation

During inflation, the demand for goods and services surpasses the available supply at current prices. This demand-supply gap leads to an increase in prices and causes inflation. To deal with the scenario, the Fed begins to pay higher interest on the excess reserve, which affects the lending growth as a guard against inflationary pressure.

When the Fed raises the interest rate on excess reserves, the banks become more willing to keep the cash in the vault instead of lending it out, which affects the purchasing power of the consumers and hence the recovery beings to establish equilibrium.

However, when the economy goes through the problem of deflation (i.e., when the supply of the goods and services produced is higher than the demand), the fed reduces the interest rate almost to zero. The reduced bank reserve ratio encourages the lending process resulting in an increase in the purchasing power of the end users.

Frequently Asked Questions ( FAQs)

Frequently Asked Questions

1. What is the purpose of bank reserves?

<p>The purpose of bank reserves is to ensure that banks have enough funds to meet the demands of their customers and maintain financial stability. Reserve requirements help banks meet their obligations and avoid bank runs and other financial crises.</p>

2. How are bank reserve requirements determined?

<p>Central banks, such as the Federal Reserve in the United States, determine reserve requirements. The requirements may vary based on factors such as the size of the bank and the level of risk in the economy. In addition, central banks may adjust reserve requirements to help manage inflation and other economic concerns.</p>

3. When do bank reserves increase?

<p>Bank reserve increases for various reasons, including open market operations by central banks, deposit inflows, borrowing from the major banks, and decreased loans. Therefore, an increase in these reserves indicates that the banks have more funds available for lending and may be in a stronger financial position.</p>

Recommended Articles

This has been a guide to Bank Reserve and its meaning. Here we discuss its classification, impact on inflation, and its interest rates in detail. You can learn more about finance from the following articles –