What Are Subprime Loans?

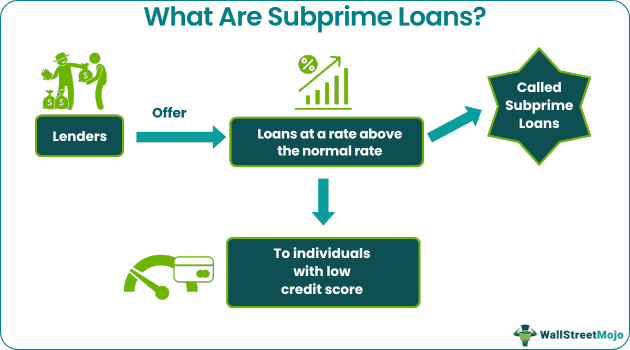

Subprime loans refer to the finances that lenders offer at a rate above the normal market rate to those who are ineligible for a conventional or prime loan. Though these finances come at a higher rate, people prefer them to serve their basic or advanced financial needs.

Subprime loans help borrowers with poor credit scores obtain loans. These loan applications are approved based on the eligibility of borrowers to repay and not on the credit score they possess. In short, the criteria for getting these finances approved are quite lenient.

- Subprime loans are loans given to entities and individuals by the bank, usually on a rate of interest much higher than the market. These loans involve a significant amount of risk with respect to their repayment terms.

- These financings do not consider the credit scores of loan seekers for approving the amount. Instead, they rely on their present ability to repay the amount.

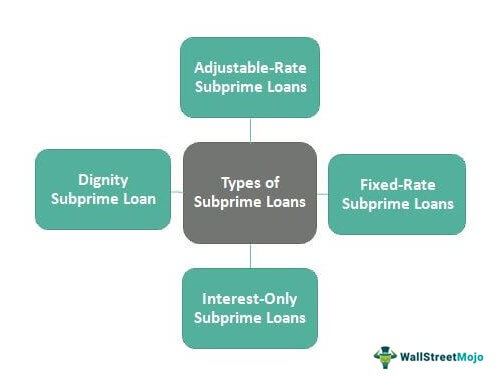

- Adjustable-rate, fixed-rate, interest-only, and dignity loans are some of the types of subprime loans.

- Although these loans support those who cannot get a prime loan because of a low credit score, certain income demands are included in this.

How Do Subprime Loans Work?

Subprime loans offer financial support to those who cannot opt for traditional loan options available in the market. This is because conventional loans have specific criteria that loan seekers cannot easily fulfill. Hence, they have to look for alternatives that offer finances on less strict terms. This is what makes loan seekers apply for these subprime options to fulfill their financial requirements, whether it is buying a house or a car.

Before 1980, the United States did not offer subprime lending options to borrowers, given the restrictions on the interest rates as put forth by the applicable state laws. However, the authorities introduced the Depository Institutions Deregulation and Monetary Control Act (DIDMCA) in the same year. It lifted all restrictions on interest-rate caps, allowing lenders to offer finances at a higher rate to loan applicants with a risky profile. The provision helped many meet their financial requirements despite having a below-average credit score.

As the borrowers do not have good credit scores, they are likely to default. Hence, the rate is higher than the prime finances, given the risks involved. However, the subprime lending option helps them have monetary support to meet their requirements when all other sources of finance prove to be of no use. The provision of lenient financing convinces borrowers to pay interest rates above the normal market rate.

Types

The subprime loans definition is better understood when their types are explored. These financing options are classified into four categories – adjustable-rate loans, fixed-rate loans, interest-only loans, and dignity loans.

#1 – Adjustable-rate loans

These are loans with a fixed interest rate primarily but have a probability of being influenced by the floating rate at a later stage. For example, a 2/28 loan has a fixed interest rate for the first two years, but the rate becomes variable after that. The applicable floating rate depends on different indices. In general, after the first few periods of a flat interest rate, the interest rate may increase gradually. In this type of loan, there is generally an additional option for the borrower, wherein they can increase their credit score before the end of the flat rate period.

#2 – Fixed-rate loans

Here, the rate of interest is fixed but high. This loan usually has a longer repayment period, between 40 and 50 years. The long-term repayment model helps borrowers with a low monthly payment to repay the loans conveniently. However, the interest rates will be higher than most other loans.

#3 – Interest-only loans

This is a loan type in which the borrowers have the opportunity to divide the payment of interest amount and the principal amount into different periods. Initially, there is a five, seven, or ten-year period in which the borrower requires paying the interest amount. Once this period gets over, they have to start paying back the principal amount of the loan. The borrower may pay the principal amount during the initial period, but that’s not mandatory. It is useful for those who have fluctuating earnings.

#4 – Dignity loans

In this type of loan, borrowers pay a small down payment, which is almost 10% of the principal amount of the loan. After the down payment, they pay the installments at a higher interest rate for a specified period. If the payments are made correctly during this period, the loan balance is calculated again, decreasing the interest rate to the prime rates applicable at that point in time.

Subprime Loans Crisis

The subprime loans crisis originated in the United States, affecting the global economy between 2007 and 2010. The rising house prices imposed restrictions on people who wanted to purchase residential property. Hence, there was an attempt to expand the mortgage credit sector wherein lenders began offering home loans to random loan seekers with little or no attention to their financial capabilities or credit scores. This is what led to the subprime loans 2008 crisis.

While people from the low-income group took advantage of the credit options offered by the Federal Housing Administration (FHA), many had limited credit alternatives. They preferred taking properties on rent to stay. The mortgage foreclosures were low, and the economy was stable. In the early 2000s, the home loan criteria became quite lenient. As a result, high-risk loans became available to home seekers. The lenders funded the finances from the pool of investors who invested in the scheme.

As the lenders made the home loans randomly available to whoever came in, the defaults rapidly rose. As the lenders did not get the payment back, they could not pay returns to the investors, who, too, ran short of funds at one point. It adversely impacted the entire cycle of investment and reinvestment. While it all started in the US, the effects spread worldwide, affecting the global economy.

Subprime Loans vs Prime Loans

Prime and subprime loans differ in many ways. Here are some of the differences between them:

| Category | Subprime Loans | Prime Loans |

|---|---|---|

| Interest rate | Higher than the normal rate | Lower than subprime finances |

| Lent to | People ineligible for conventional loans | Whoever satisfies the eligibility criteria |

| Risk Involved | Riskier | Less risky |

| Fees included | High down payments and origination fees may be required | No such requirements |

| Credit scores | Not important | Important |

Frequently Asked Questions (FAQs)

Are subprime loans illegal?

These loans were not allowed in the United States until the introduction of the Depository Institutions Deregulation and Monetary Control Act (DIDMCA) in 1980. This act allowed lenders to offer loans at a rate higher than the currently effective market rate. It was then that the lending institutions started offering these loans. Thus, subprime loans are completely legal.

Do subprime loans still exist?

Yes, these loans are still available. Lending institutions still offer these high-risk finances for homeowners with low credit scores.

Do subprime loans hurt your credit score?

These loans can hurt one’s credit score if the person defaults on making the required repayment. However, the good thing is that the same loan helps one build a credit score by making timely payments.

Recommended Articles

This has been a guide to what are Subprime Loans. Here, we explain how do they work, their types, the crisis of 2008, and their differences with prime loans. You may learn more from the following articles –