Part of our Banking Ratios & Metrics guide

Bank Capital Meaning

Bank Capital, also known as the bank’s net worth, is the difference between a bank’s assets and liabilities. It primarily acts as a reserve against unexpected losses and protects the creditors in case of bank liquidation. The bank’s assets are cash, government securities, and loans offered by banks that earn interest (Eg. Mortgage, letter of credit). The bank’s liabilities are any loans/ debt obtained by the bank.

Regulatory authorities look at bank capital ratio, especially the tier 1 metric as a symbol of the core strength of the bank in terms of its finance based on international standards set and regulated by the Basel Committee on Banking Supervision. This also gives creditors an idea of the bank’s assets if the bank were to be liquidated today.

Bank Capital Explained

Bank Capital plays a key role in banking operations. The risk element is always present in banking operations; at any time, losses can happen. To protect the banks from insolvency and public deposits, the banks maintain capital to protect themselves against uncertainties and losses.

The amount of capital a bank needs depends upon its operations and its associated risks; more the risk, more the capital. It is also used for the expansion of banks and other operational purposes. Without proper capital, the bank may even go bankrupt. Therefore, it needs to be maintained at proper levels, and it should fall below the limits set by law.

Maintaining an adequate level of capital is vital for banks. It not only safeguards the interests of depositors but also ensures the bank’s ability to continue lending and conducting its operations even in adverse economic conditions. Regulators set minimum capital requirements that banks must meet to operate safely and mitigate systemic risks.

Bank capital management gives them a buffer against loan defaults, economic downturns, and unexpected losses, allowing banks to absorb these shocks without resorting to government bailouts or risking insolvency. It also serves as a measure of a bank’s financial health, as a bank with higher capital ratios is generally considered more resilient and less risky to its stakeholders.

Requirements

Bank capital ratio requirements are regulations imposed by financial authorities to ensure banks maintain a minimum level of capital relative to their risk-weighted assets. These requirements aim to enhance financial stability and protect depositors and the broader economy. Let us understand them through the points below.

- The requirements mandate banks to maintain a minimum Common Equity Tier 1 (CET1) capital ratio of 4.5% of risk-weighted assets

- A total capital ratio of 8%.

- Countercyclical buffers, capital conservation buffers, and systemic risk buffers.

- These rules vary by jurisdiction and are enforced by banking authorities to mitigate risks and prevent bank failures.

Structure

The Fund structure states how the bank will finance its operations using the available funds. It can be equity, debt, or hybrid securities.

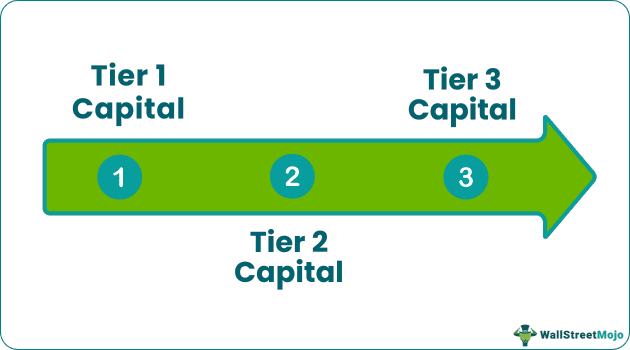

Types of Bank Capital

Banks must maintain a certain amount of liquid assets in correspondence to its risk-weighted assets. The Basel accords are banking regulations that ensure that the bank has enough capital to handle the operations and obligations.

There are three types:

#1 – Tier 1 Capital

It consists of the bank’s core capital (i.e.) Shareholders’ equity and the disclosed reserves (retained earnings) less goodwill, if any. It indicates the financial health of the bank. Also, It consists of all reserves and funds of the bank. It acts as primary support in the case of the absorption of losses. It appears in the bank’s financial statement.

Under Basel III, they need to maintain a minimum of 7% risk-weighted assets in Tier 1 capital. Plus, banks also have to hold an additional buffer of 2.5% of risky assets. Risk-weighted assets indicate the bank’s exposure to credit risk from the loans provided by the bank.

Tier 1 Capital / Risk-Weighted Assets = 7 % (Minimum Requirement)

Example

Bank X has $100 billion in Tier 1 capital. Its risk-weighted assets are $1000 Billion. (i.e) the Tier 1 capital ratio is 10 %, which is more than the Basel III requirement, which is 7%.

#2 – Tier 2 Capital

It consists of funds not disclosed in the financial statements of the bank. It includes revaluation reserve, hybrid capital instruments, subordinated term debt, general provisions, loan loss reserves, undisclosed reserves, fewer investments in unconsolidated subsidiaries, and other financial institutions.

Tier 2 capital is additional capital as it is less trustworthy than Tier 1. It is difficult to measure this capital as the assets in this bank capital ratio is not easy to liquidate. Banks will divide these assets into the upper and lower levels based on the individual assets’ liquidity.

Under Basel III, they must maintain a minimum of 8% of the total capital ratio.

Example

Bank X has $15 Billion of Tier 2 Capital. The Tier 2 capital ratio is 1.5%, which is more than the Basel III requirement.

The Total capital ratio is 11.5% (i.e) Tier 1 + Tier 2 = 10% +1.5% =11.5%. Which is more than the Basel III requirement of 10.5%? (along with the additional buffer)

#3 – Tier 3 Capital

Tier 3 Capital is tertiary capital. It is there to shield the market risk, commodity risk, and foreign currency risk. It includes more subordinated issues, undisclosed reserves, and loan loss reserves compared to tier 2 capital.

Tier 1 Capital must be more than the joined Tier 2 and Tier 3 Capital.

Ratios

Bank capital management is crucial for maintaining the stability of financial institutions and the broader economy. Several key ratios are used to ensure banks comply with these requirements:

- Common Equity Tier 1 (CET1) Capital Ratio: This ratio measures the core equity capital (common stock and retained earnings) as a percentage of risk-weighted assets. Regulators typically require a minimum CET1 ratio to ensure a strong capital foundation.

- Tier 1 Capital Ratio: Tier 1 capital includes CET1 capital and additional Tier 1 capital, such as certain hybrid instruments. It is expressed as a percentage of risk-weighted assets, providing a broader measure of a bank’s core capital strength.

- Total Capital Ratio: This ratio combines Tier 1 capital with Tier 2 capital, including subordinated debt and other qualifying instruments. It is expressed as a percentage of risk-weighted assets and ensures banks have a sufficient capital buffer.

- Leverage Ratio: The leverage ratio assesses capital adequacy without considering risk-weighted assets. It compares Tier 1 capital to average total consolidated assets, providing a simple measure of how well capital supports the bank’s total assets.

- Countercyclical Buffer: This buffer requires banks to set aside additional capital during periods of economic growth to be used during downturns. It is calculated as a percentage of risk-weighted assets and aims to mitigate pro-cyclical lending behavior.

- Capital Conservation Buffer: This buffer ensures banks maintain a minimum capital buffer above regulatory minimums to withstand economic stress. It is expressed as a percentage of CET1 capital.

- Systemic Risk Buffer: Some banks may be required to hold an additional buffer to mitigate risks associated with their systemic importance. This buffer varies by jurisdiction and depends on a bank’s systemic significance.

How Does It Increase or Decrease?

Banks raise financing from various sources to provide loans to the customers on which they charge interest, which is more than the cost they borrow. The difference is profit.

- Raising funds from shareholders – Banks, through public issues, raise capital, which is used for banking operations. The return to the shareholders will be in the form of dividends and appreciation of the share value.

- Obtaining loans from financial institutions;

- Government funding the bank

- Term deposits, savings account;

Functions

Let us understand the functions of bank capital management through the discussion below.

- Bank capital acts as a protection to the bank from unexpected risks and losses.

- It is the net worth available to the equity holders.

- It assures the depositors and the creditors that their funds are safe and indicates the bank’s ability to pay for its liabilities.

- It funds for expansion in banking operations or for procuring any assets.

Difference Between Bank Capital and Bank Liquidity

Bank Liquidity acts as a measure of the bank’s assets, which is readily available to settle the dues and to manage the working capital components and business operations. Liquid assets can be converted into cash easily. (Eg) Central bank reserves, Government bonds, etc. To manage the business operations, banks should have sufficient liquid assets (Eg) Cash withdrawals by bank account holders, Repayment of term deposits on maturity, and other financial obligations.

It is the net worth of the bank, which is the difference between the bank’s assets and liabilities. It acts as a reserve for a bank to absorb losses. The bank’s assets should be greater than the liabilities to stay solvent. Minimum levels of required bank capital need to be maintained per the Basel requirement to manage the bank’s functioning.

Recommended Articles

This has been a guide to what is Bank Capital and its meaning. Here we discuss its types, examples, requirements, functions, and structures. You can learn more about financing from the following articles –