Table Of Contents

Carrying Value Definition

Carrying value is the reported cost of assets in the company’s balance sheet, wherein its value is calculated as the original cost less than the accumulated depreciation/impairments. The intangible asset is calculated as the actual cost less the amortization expense/impairments.

In simple words, it is the value of an asset in the books of accounts/balance sheet less the amount of depreciation on the asset’s value based on its useful life. In other words, we can say it is equal to the book value of an asset because it is not the same as the market/fair value of an asset.

The carrying value of a bond is different from calculating the carrying value of bonds. It means the amount stated in the company balance sheet on its issue date. It is a combined total of its face value and the amortization premium or discount. It is also called the carrying amount or the value of the book of the bond.

Table of contents

- The carrying value of an asset refers to the amount shown in the balance sheet, which is lower than depreciation incurred on it throughout its life.

- There is a slight difference between the carrying value and the asset's fair value. The carrying value is the asset's book value, whereas one can calculate the fair value using market techniques.

- One can calculate the carrying value of an asset using a subtraction of the asset's original value by the depreciation it accrued. The carrying value is an accurate measure of the liabilities and assets of the company.

- A bond's carrying value is not the same as how bonds are estimated to carry value. It alludes to the amount shown in the corporation's balance sheet as of the date of issuance.

Carrying Value Formula and Calculation

Below are the formulas for carrying the value of an asset and bond.

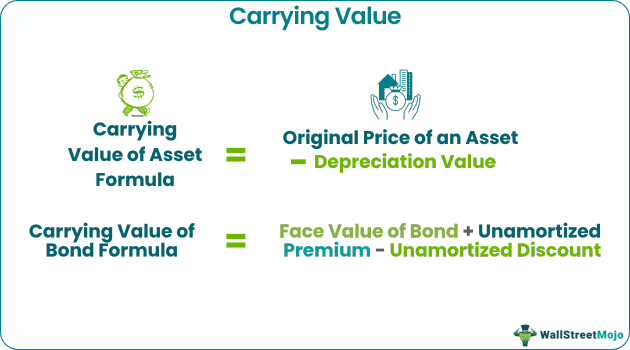

Carrying value of asset = Original price of an asset – Depreciation value

Carrying the weight of bond = Face value of bond + unamortized premium – unamortized discount

Examples

#1 - Carrying Value of Asset

Let’s assume that a company owns a plant and machinery amounting to $1,00,000 to produce certain company products. The above machinery has a depreciation value of $4000 and has a useful life of 15 years.

Please note that the cost of plant & machinery includes transportation, insurance, installation, and other testing charges necessary to get the asset ready for its use.

Further, depreciation means lowering the value of tangible assets due to wear and tear. Tangible assets represent plant & machinery, furniture, office equipment, etc.

#2 - Carrying Value of Bond

When the price of bonds is too high, investors pay a higher premium on the bond price. Conversely, if the bond’s price is low, the investors purchase the same at the discounted price. However, this depends upon the market rate of interest on the bond’s issuance date.

These premiums and discounts are amortized throughout the bond’s life so that the bond matures its book value, which is equal to its face value.

We can say that the bond carrying value means the bond’s par value plus the unamortized premium and less the unamortized discount. The same is reported in the company’s balance sheet and is also called the book value.

For example, the bond’s face value is $ 1000, the date of the bond issue is January 1, 2019, and the maturity date is December 31, 2021. Let’s assume the coupon rate is at 5%.

Now, when the bond is issued, investors will require a rate of return of 4%.

First, we need to check whether the bond is issued at a premium or discount. Preferably, we must be aware of the market rate of interest, which is 4%. The interest rate is less than the coupon rate, i.e., 5%. Therefore, the bond is issued at a premium, i.e., $ 1250. Suppose, after two years, $100 is amortized. Thus, the bond carrying value is $1,000 plus $150, i.e., $1,150; and vice versa, they can sell the bond if the market interest rate is 6%.

Difference between the Carrying Value vs. Fair Value

| Carrying Value | Fair Value |

| It is the book value or the asset value, which is the actual cost of the asset. | The fair value of assets and liabilities is calculated on mark-to-market. |

| It is based on the figures from an entity’s balance sheet; | Whereas, the fair value figures depicts the value of the assets sold in the open market. |

| It is calculated by taking the difference of the assets and liabilities on the balance sheet, also known as the Net Worth of the company; | Calculated by multiplying the market price per share with the number of shares outstanding; |

| Based on the historical cost of the asset. | Based on the current market price of the assets. |

Note: We have used the word 'amortized' several times in our article. It means the spreading of intangible assets cost over the assets' useful life, unlike depreciation. Intangible assets are not tangible assets. Examples of Intangibles assets are copyrights, patents, software, franchise agreements, trademarks, etc.

Frequently Asked Questions (FAQs)

The book value is the total value at which an asset is recorded on the company's balance sheet. On the other hand, one can define the salvage value as the total scrap value of any asset at the end of its useful life.

Goodwill is an accounting charge that companies record. It is calculated using the purchase price of the firm, then deducting the market value of assets and liabilities.

Sometimes, the carrying value obtained is negative, meaning that the asset has incurred a loss, and when losses exceed the profits, a liability gets created. Conclusively, the maintenance and life efficiency of the asset matter in preventing its transformation into a liability.

Recommended Articles

This article has been a guide to what Carrying value is & its definition. Here we discuss Carrying Value Formula and examples and its differences with Fair value. You can learn more about accounting from the following articles –