Call Risk Definition

Call risk is the risk that the bond an investor has invested in will be redeemed by the issuer before its maturity date, thereby raising the risk for the investor as he would have to reinvest the redeemed amount at a much lower rate or in an unfavorable investing market scenario.

Key Takeaways

- Call risk refers to the risk that the issuer may call or redeem a bond or other fixed-income security before its maturity date.

- Call risk can negatively impact investors who rely on the consistent income generated by the bond

- Call protection assures investors that the bond will not be called during that period, allowing them to receive the expected income until the call protection period expires.

Components of Call Risk

Call Risk, as explained earlier, exposes an investor to an unfavorable environment. It has two major components

- Time to Maturity: Call risk is often associated with callable bonds providing an option to the issuer to call the bond much before the maturity date. The probability of a bond being called decreases with time as there is less time left for the bond issuer to exercise the option to call the bond.

- Interest Rates: Interest rates are even a bigger factor in call risk as when the interest rates fall, the yield increases, and the issuer will find it profitable to call the bond and restructure the bonds as per the current interest rate cycles, thereby leading to paying lower coupons on the same amount of principal.

Example of Call Risk

The following is the example of call risk.

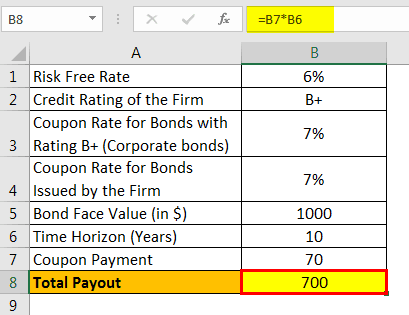

Suppose a firm reached out to the financial market participants to fund its long-term liabilities. In the process, the bonds of the firm issue as the management does not want to dilute its equity stake. Let’s suppose the bonds are issued at a coupon rate of 7%. This effectively means that the firm pays out $7 to the bondholders for each $100 invested. The coupon rate of 7% was decided as per the current prevailing rate of 6% (assuming the risk-free rate). Assume that due to changing political and economic scenarios like trade wars and periods of recessions, the interest rates cycle changes, and the yield curve inverts.

This effectively means that the risk-free rate decreases. For calculation purposes, let’s assume that it drops to 3%. In the case of vanilla bonds issued by the firm, it has to still pay 7% even if the new bonds issued are at a much lower rate as the risk-free rate has itself dropped considerably(6% to 3%). The firm is effectively borrowing at a much higher rate, which can have a considerable effect on its cash flows.

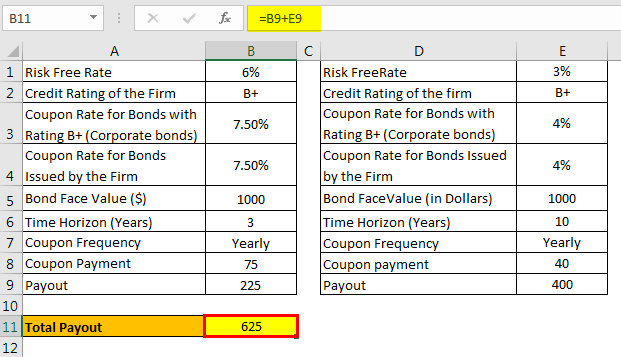

Now consider the scenario when the management had issued a callable bond. In that scenario, the firm would have to pay a higher coupon (let’s assume 7.5%) when the risk-free rate is 6%, as the investors would demand a premium even if the credit rating of the firm is high. The advantage that the firm would have by issuing this callable bond is that it can pay back the principal amount to the bondholders much before the maturity date and restructure the debt at a much lower rate (let us say 4%) as the risk-free rate has itself decreased by 50%.

In the above example, 0.5% (7.5 % – 7 %) is the call risk premium of the callable bond. The following tables summarized the cash flows in both scenarios.

Scenario 1

The firm issued a Vanilla bond

Scenario 2

The firm had issued a callable bond, and the interest rate cycle changes after 3 years.

Ignoring the change in duration and the time value of money in the interest of simple calculations, we can see the firm has saved at least $ 75 in the pay-out of $ 700 (i.e., more than 10%) across 10 years. For the investor who had invested in scenario 2 (callable bond), the cash flow would have considerably reduced. This is called call risk and is applicable to the investor of the callable bond.

Important Points

- An investor invests in a bond because he wants to get a fixed return for a particular duration of time. At the maturity date, when the time to the horizon has completed, the principal value is returned. This is a typical life cycle of a vanilla bond. However, the situation gets a twist if the bond issued is a callable bond. In such a scenario, the issuer of the bond has a right to call the bond, and return the principal to the investor much before the maturity date.

- Although the investor has got his money back, he has to reinvest the principal amount to gain the same quantum of returns. This might not be possible because the market situation might be completely different. Most often than not, the interest rates would be low. In economic terms, this is termed as reinvestment risk – the risk that the principal reinvested might not give the same returns as it was initially bound to give.

- The issuer of the callable bond has to pay a premium in addition to the coupon rate as the investors have to carry a call risk and expect to be compensated for the same.

- In terms of calculations, the pay-out of call risk is calculated similarly to the call option as the issuer may or may not call the bond.

Conclusion

Call risk as such itself is not cause of worry to the investor but is the beginning of many more unfavorable and unforeseen situations. It is nothing but reinvestment risk as It exposes the bondholder to an unfavorable investing environment, thereby leading to an unexpected decrease in cash flows and hence the portfolio risk. Although if managed properly, it can help a speculator earn good returns in a considerably short period of time.

Frequently Asked Questions (FAQs)

How can investors assess call risk?

Investors can assess call risk by reviewing the terms and conditions of the bond, including any call provisions, call protection periods, and potential call dates. Understanding the issuer’s financial situation and monitoring interest rate movements can also provide insights into the likelihood of a bond being called.

What are some strategies to manage call risk?

Investors can employ several strategies to manage call risks, such as diversifying their bond portfolio to include both callable and non-callable bonds, investing in bonds with longer maturities or higher call premiums, and conducting thorough research on the issuer’s call history and financial stability.

Is covered call risk-free?

No, covered calls are not risk-free. While covered call strategies can offer specific benefits and potential income generation, they still carry risks that investors should be aware of. Here are some critical risks associated with covered call strategies:

a. Stock price risk

b. Opportunity Risk

c. Market and volatility risk

Recommended Articles

This has been a guide to what is called risk and its definition. Here we discuss the example of a call risk along with an explanation and its important points. You can learn more from the following articles –