Default Risk Premium Definition

The default risk premium is an additional amount of interest rates paid by a borrower to lender/ investor as compensation for the higher credit risk of the borrower assuming his failure to pay back the principal amount in the future and can be mathematically described as the difference in between the interest rates payable on bond and a risk-free rate of return.

Key Takeaways

- The default risk premium is an additional interest rate a borrower pays to lenders/investors for higher credit risk, calculated as the difference between bond interest rates and risk-free rates.

- It is a compensatory payment for investors or lenders in default on debt, typically applicable to bonds. Lenders charge higher premiums if the borrower defaults on recurring interest payments or principal amounts, incentivizing them to take more risk.

- Lenders charge higher default risk premiums for poor credit, while the government pays dividends in favorable conditions to attract investors and offer higher yields.

Explanation

Default risk premium (DRP) works as compensatory payment to investors or lenders if, in any case, the borrower defaults on their debt. DRP is commonly applicable in the case of bonds. Any lender will charge a higher premium if there are chances that the borrower will default in meeting out its debt servicing, i.e., defaults in either recurring interest payments or principal amount as per the agreed terms and conditions. It acts as an incentive for the lender to get rewarded more for the risk undertaken.

Purpose

If the lender assumes that the borrower can default in complying with its debt servicing terms and conditions, i.e., risk of non-payment, the lender may charge a higher DRP. Investors with poor credit records pay a greater interest rate to borrow money. If adequate DRP is not available, an investor will not invest in companies more prone to default. If a company depicts lower default risk, this, in turn, will lower the future cost of raising capital for the company as such companies will get funds at lower DRP. The government does not pay a default premium except in unfavorable conditions to attract investors and pay higher yields.

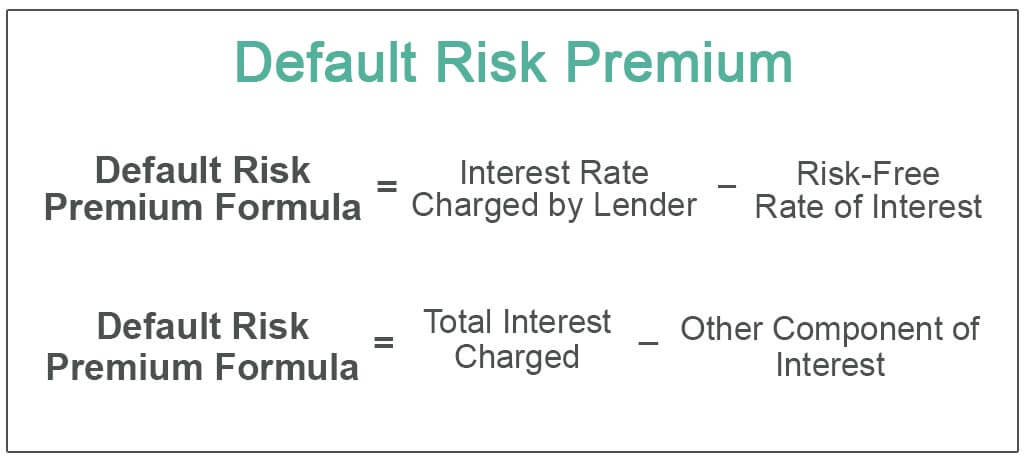

Default Risk Premium Formula

DSR formula is represented as below –

DRP = Interest Rate Charged by Lender – Risk-Free Rate of Interest

DRP = Total Interest Charged – Other Component Of Interest

DRP is the difference between the Risk-Free Rate and the Interest Rate charged by the lender. The interest rate comprises the following components – Inflation premium, maturity premium, liquidity premium, risk-free rate, and DRP. The risk-free rate is based on an asset that possesses no risk. DRP generally deals with treasury bonds, as the US government backs these bonds. The default risk premium is the amount above the rate of treasury bonds that any investor would like to earn on an investment

How to Calculate Default Risk Premium?

DRP is the estimated return on a bond reduced by a risk-free return rate on investment. To calculate the DRP of a bond, the bond’s coupon rate needs to be reduced by a risk-free return rate. It can be understood through the following steps.

- Step 1 – The rate of return for risk-free investment should be determined. The principal amount will grow with inflation while reducing deflation, and the US government backs the security. Say the rate of risk-free security is 1%.

- Step 2 – If a corporate bond that we wish to purchase offers 10% of the annual rate of return, then subtracting treasury’s rate of return from a corporate bond will be 10% – 1%, that is 9%.

- Step 3 – Now, the estimated rate of inflation will be subtracted from the above difference. If inflation is estimated to be 4%, the value will be 9% – 4%, 5%.

- Step 4 – If any other premium is included in the bond-like liquidity premiums, subtract those premiums. For example, if the bond carries a liquidity premium of 1%, subtracting 1% from 4% will arrive at 3% of the default risk premium.

Example

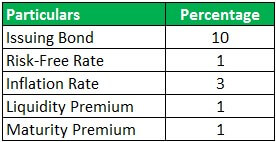

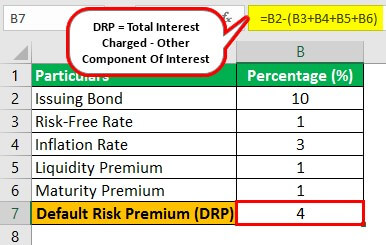

ZYDUS Ltd. is issuing bonds with a 10% annual percentage yield. Now, suppose the risk-free rate is 1%. In that case, inflation of that particular year is estimated to be around 3%, and the liquidity and maturity premiums of the bonds are both 1%, adding all of these together with the sum totals to 6%. Hence, this bond’s default risk premium equals 4% of the annual percentage yield (10%) – other interest components (6%).

Solution

Here,

- The total Interest charged is 10%

- Other components of interest = (risk-free rate + inflation rate + liquidity premium + maturity premium)

- = 10% – (1%+3% + 1% + 1% )

- = 10% – 6%

- DRP = 4%

Factors that Determine Default Risk Premium

The following are the factors that determine DRP –

- Credit History – Any entity is considered trustworthy if it has paid previous debts on time with interest payments. Such companies or individuals are presumed to have lower default risk, and therefore they get access to cheaper funds as lenders charge lower DRP from them.

- Credit Worthiness – Companies with poor credit ratings and lower-grade bonds pay more default risk premiums. The companies are rated based on their financial performance by rating agencies such as Moody’s, Fitch, and S&P. Better the financial performance is the credit rating. Higher credit rating results in a lower default risk premium, and hence the investor would not get high returns since the risk is less.

- Liquidity and Profitability – The company’s profitability helps banks know their creditworthiness before giving loans. The cash flows are examined to determine if the company has enough cash to meet its interest obligations.

Advantages

- With a high default risk premium, the market compensates investors more for undertaking greater risk by investing in such companies.

- Novel and risky business investments offer above-average returns, which the borrower can use as an earning reward for investors on investment risk.

- The riskier a particular asset is, the greater is the required return from that asset.

- DRP helps assign a relative risk rating to a particular asset for the investor.

- DRP helps determine the level of risk an investor or lender has to undergo if a borrower defaults on the loan.

Frequently Asked Questions (FAQs)

How does default risk premium affect interest rates?

The interest rate that must be provided to attract investors will increase directly to the default risk of a hazardous bond. Investment choices from an investor’s standpoint, the default risk premium influences investment choices by contrasting the default premium of similar bonds.

Can default risk premium be negative?

A risk premium, in general, is a means to reward an investor for taking on more risk. Risk premiums may be reduced for investments with lesser risk. An extremely low-risk investment’s return occasionally could have a negative risk premium.

How does the default risk premium impact investors and borrowers?

For investors, a higher default risk premium means earning higher returns for taking on greater risk. On the other hand, borrowers face higher borrowing costs if they are perceived as having a higher risk of default. This translates into higher interest rates on loans and bonds, making it more expensive for them to raise funds in the financial markets.

Why does default risk premium vary?

Higher credit ratings have lower default premiums and lower yields and are assigned to businesses that generate more money or are more secure.

Recommended Articles

Recommended Articles

Continue with these closely related articles from the same guide.